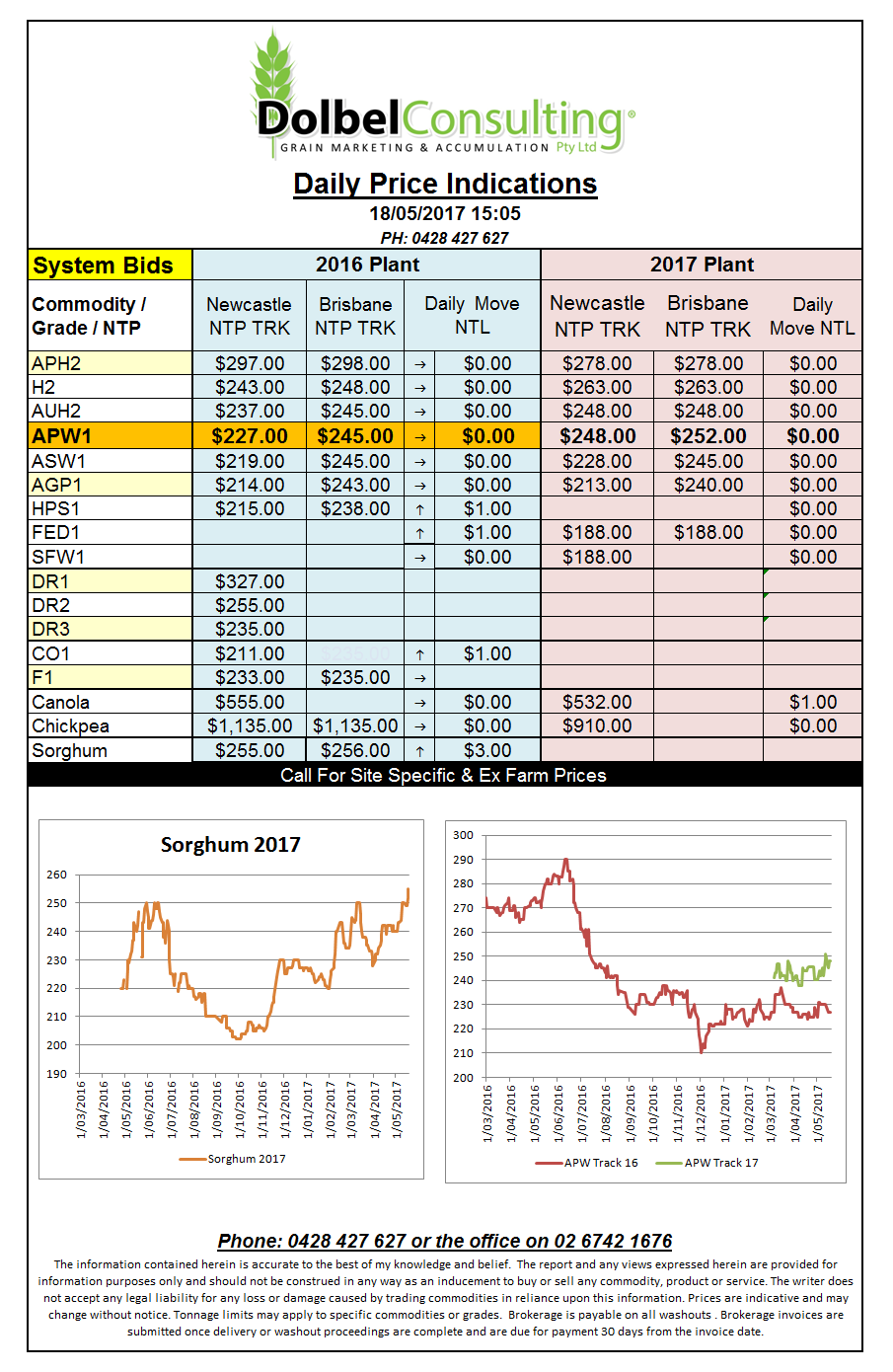

Prices 18/5/17

Durum values in central Saskatchewan are still firm for 1CWAD with ex farm average pricing from pdq coming in at C$260.85 / tonne for 13% protein around a C$22 premium over their spring wheat bid at 13.5% protein. That compares well to the $33 premium we are currently seeing for DR1 above APH2. Local demand has picked up a little for DR1 and DR2 of late with accumulation activity centred around a loading out of Newcastle in June. Direct deliveries are required to be at port by the 5th of June so I’m not sure how long the better system bids will hang around after that. There is also talk / rumour of another boat later in July but I’ve nothing firm on that shipment as yet.

US futures for grains were generally flat or a little firmer overnight, more a function of a weaker US dollar than anything fundamental though. Not much has changed in regards to global production data since the USDA report last week. Most crops around the world are in reasonable shape and those that are not are not great located in the major importers and most major exporters are still dealing with massive carryover stocks from the last couple of year. We may see some further damage to the Kansas crop tomorrow as severe storms cross the Midwest US but if an April blizzard can’t bull this wheat market nothing shy of a major drought will.