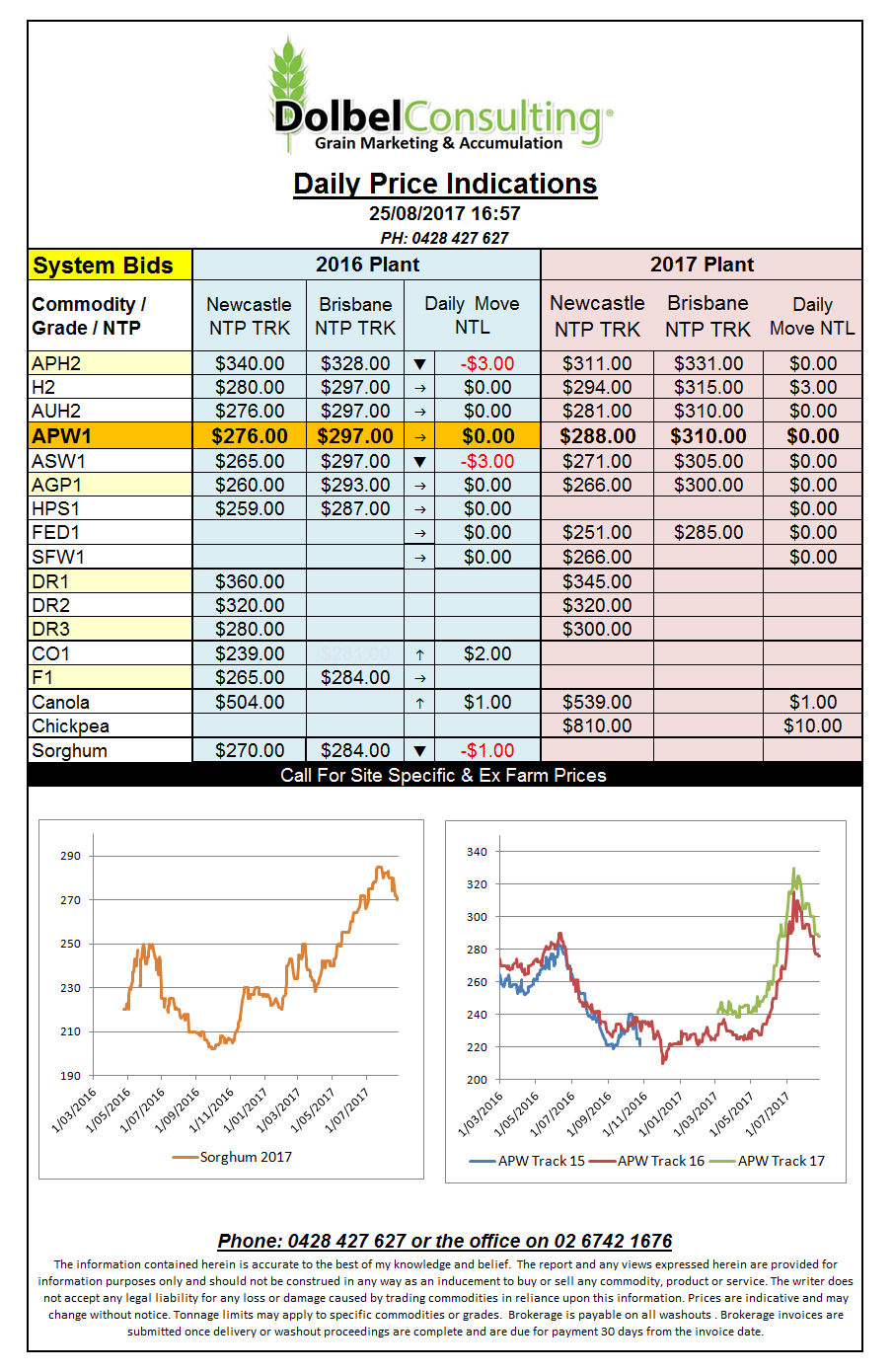

Prices

There are a couple of influencing factors in the US late this week. The Farm Journal crop tour looking at potential row crops yields, export numbers out of the US and the position of the market, which at present shows wheat as generally oversold.

The crop tour reports are telling the market corn yields in some areas are better than last year and the five year average. While other locations, some of those in the key producing states of Iowa and Illinois are disappointing. Dry weather in the “I” states has pruned yields with some crops estimated as low as 9.54t/ha in NW Iowa. Generally the yields are a little below average but not likely to bring much of an impact to the market.

For soybeans it is much the same story but reports of many pods remaining unfilled is starting to raise some eyebrows. 20% lower pod counts in some fields. Good weekly US exports of 2mt helped beans along too. Surprisingly ICE canola futures dipped a little but with the basis our local traders have pulled out of the market this week and the slightly weaker AUD prices should remain relatively stable here.

Wheat continues to be pressured by the large Russian crop but reports of lower yield potential in the US, Canada and Australia as well as reduced area in Argentina is now countering the Russian influence somewhat. With offers of Russian wheat FOB Black Sea still slipping though it is hardly likely we will see a fundamental move higher in values in the short term, technical move …… maybe.