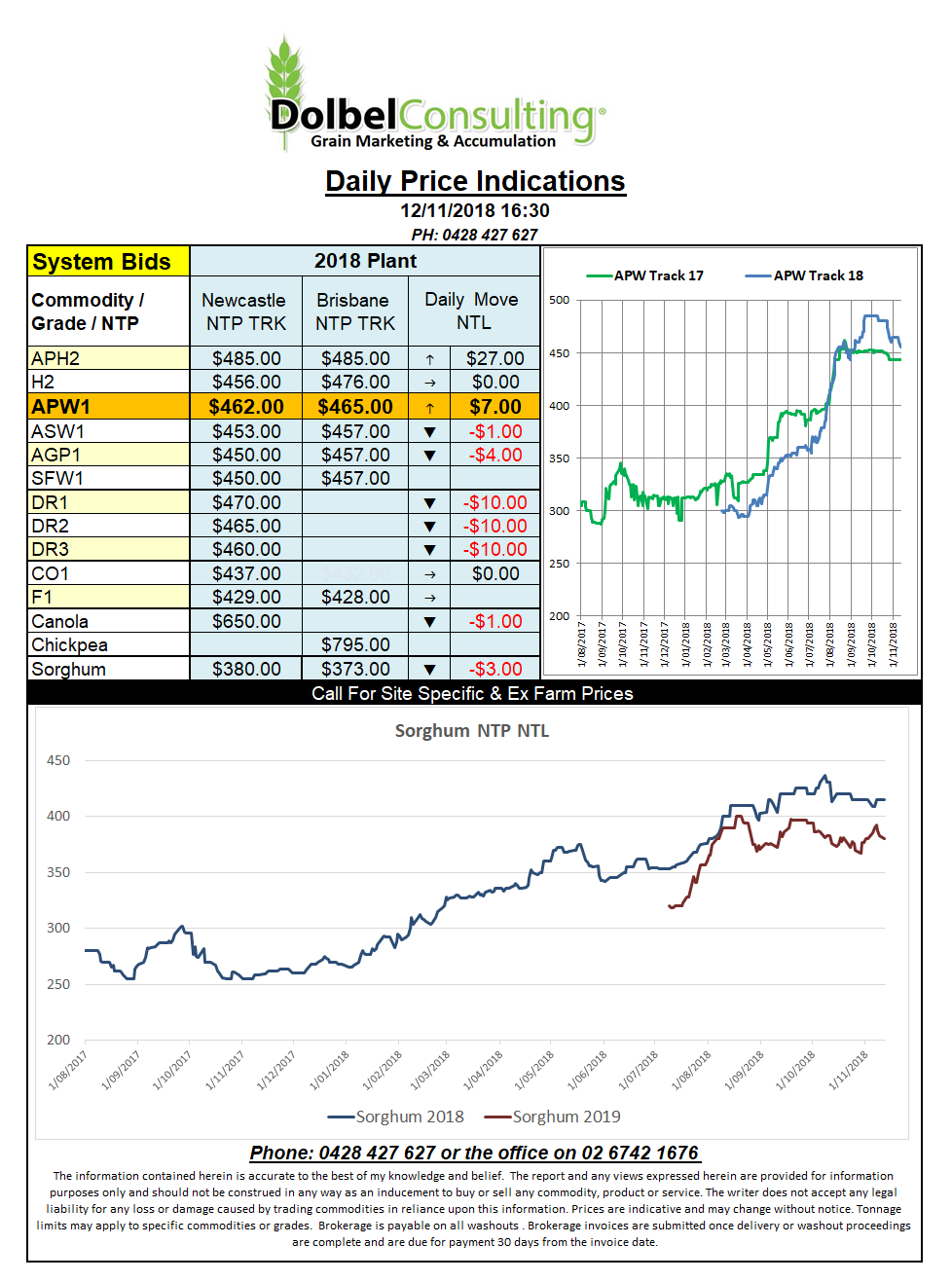

Prices 12/11/18

US wheat futures drifted lower on the back of the recent USDA report. It appears Chicago SRW is destined to drift aimlessly either side of 500c/bu for a while longer yet. We’ve see futures trade US$10 either side of US$183/t for Dec 18 SRW since Ag-Quip. This spread has even narrowed up more since the start of October with the range now about US$7.00 either side.

The market appeared happy to trade around the increase in Chinese wheat stocks. That’s a little odd considering a few months ago there was actually talk of dropping China off the balance sheet as they are generally neither an importer or an exporter thus have little impact on the general S&D for wheat unless they have a massive crop failure. Remember they carry over 50% of the current world ending stocks, this equates to over a year’s worth of Chinese production. With Chinese usage at roughly 123mt and stocks at 143.57mt and production at 132.5mt their ending stocks are expected to get bigger.

As for the rest of the world with China out of the equation this leaves ending stocks at 123.14mt, about 920kt less than last month’s USDA estimate. 123.14mt equates to only 69% of annual world exports or 252 days of buffer stocks if the world ran out of wheat production. Without China we also see a sub 20% stocks to use ratio, so things are a little tighter than the world trade may lead you to believe but without a massive failure, and we won’t really see that possible until spring 2019, than the world appears comfortable and prices appear to be destined to stay in the current range we are looking at.