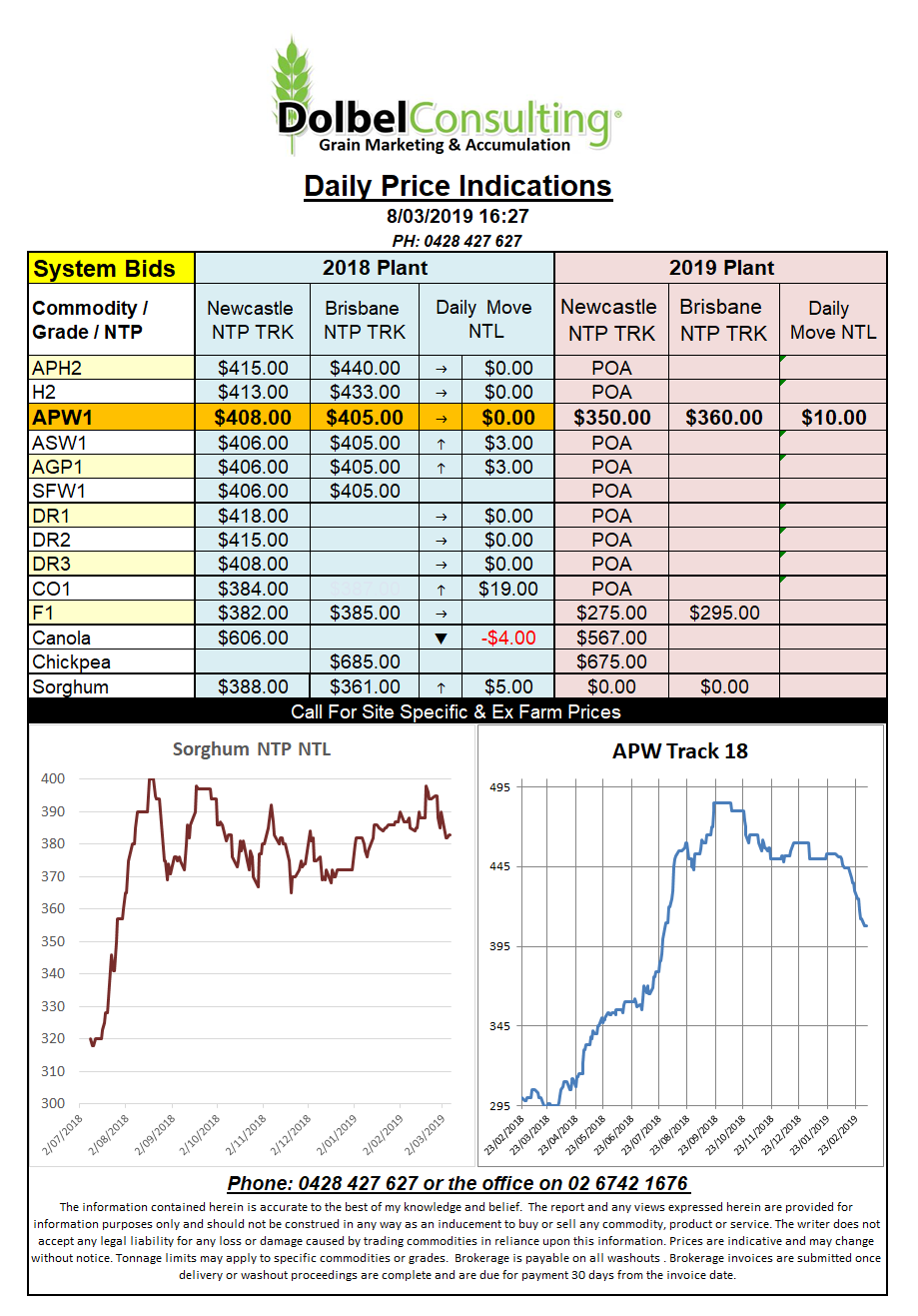

Prices 8/3/19

US soft and hard red winter wheat futures at the CME were hit hard again in overnight trade. The SRWW move when reflecting the USD / AUD exchange rate will come in close to $5.00 lower if reflected in new crop wheat values here.

The recent sharp decline has not been reflected in new crop Newcastle track wheat bids in recent days. At Chicago Dec 2019 futures have fallen roughly AUD$16 / tonne since February 26th while new crop cash bids here have slipped just AUD$3.00 / tonne.

The May SRW contract at the CME is oversold and has been oversold for a couple of weeks now with the funds happy to sell down hard on any attempt to correct. This does expose the funds to technical short covering if there are any fundamental issues through the thaw period in the USA, let the silly season begin.

The funds were having none of the positive news in the market ruin a good sell down. US weekly export sales came in at 621,700 tonnes. Even though the punters were expecting 200kt to 500kt to be announced the 20% of additional sales made no impact on sentiment. Weekly US export loadings of wheat were also good at just over 621kt.

Last night’s half decent export sales number takes US actual sales to 22.6mt versus the USDA forecast of 27.2mt, so another 4.6mt to go. It’s almost looking achievable with 13 weeks to go, that’s about 353kt / week required. Wouldn’t it be surprising if the funds all of a sudden started buying on the back of decreased US ending stocks in wheat. Not to mention the smallest US winter wheat area in 100 years and a very cold start to spring……