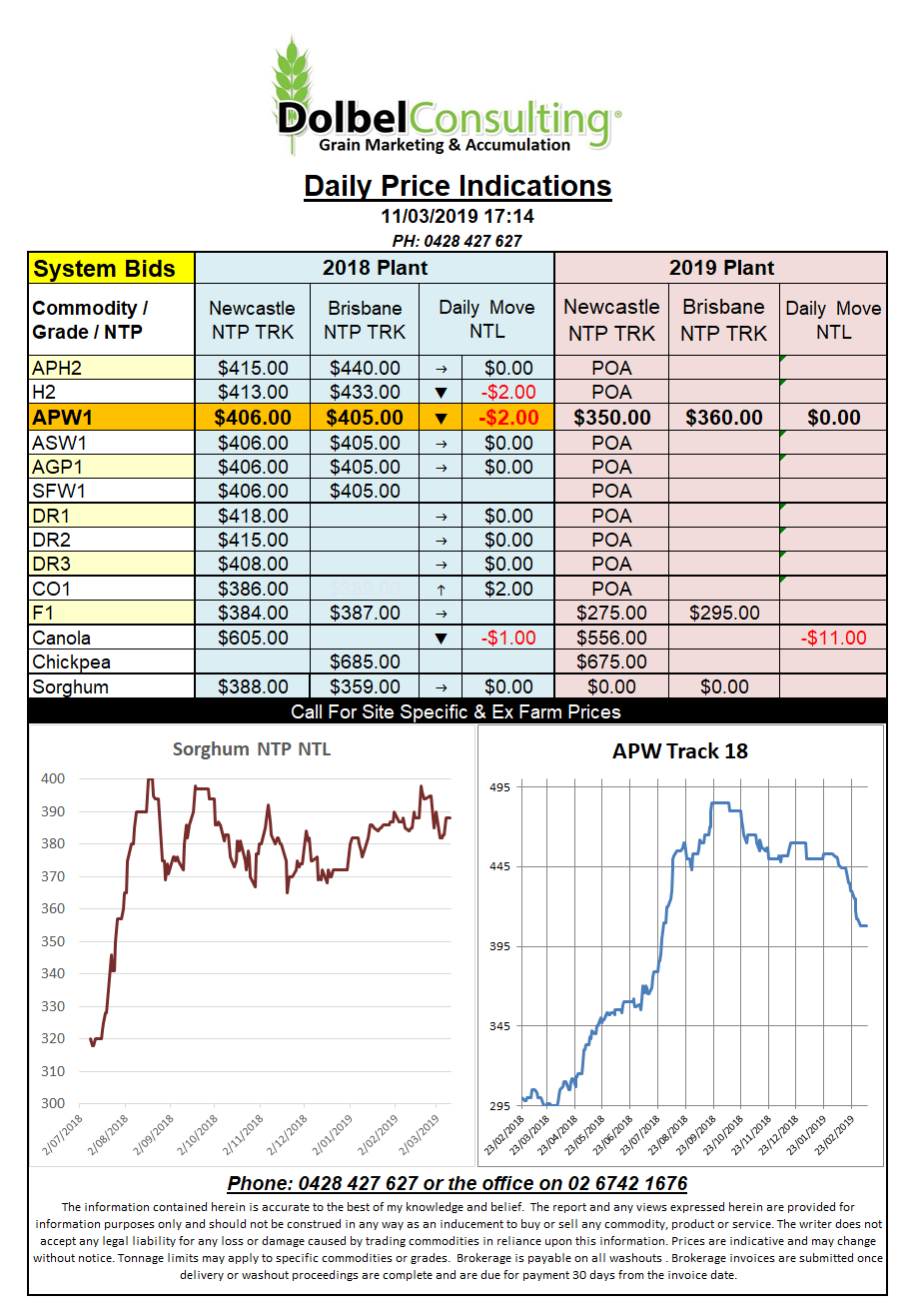

Prices 11/3/19

The USDA report was considered as bearish wheat, or even more bearish than some of the punters had anticipated.

World ending stocks were jacked up to 270.5mt an increase of 3mt. The biggest hit came from an increase in US ending stocks thanks to slow exports, an increase of 1.2mt saw US carryover increased to 28.72mt. To meet the USDA export target of 26.26mt the USA export sales will need to come in at roughly 368kt tonnes per week as current export sales are listed at 22.58mt. Why the punters think this will be difficult is a little beyond me at the moment. US wheat is cheap into Asia, has no competition from Australia and in some cases is even working well into the Middle East. The more I look at this the more I can see a spring rally in US wheat futures but I’m not a punting man.

So with all the bearish talk in the wires we actually saw SRW futures at the Chicago CME rally a little, not a very committed rally but a close in the black it was. Soybeans were softer but both ICE canola and Paris rapeseed ran their own race both managing a close in the black. It should be mentioned that there was 16kt of nearby wheat traded in the Aussie FOB Platts contract at the CME and another 16kt done in the June contract. Does this have something to do with the large off screen trades at the ASX yesterday ?. The Platts number came in as a settlement value of US$265.75, so roughly AUD$377 FOB, or an equivalent price of AUD$352 FIS (comparable to ASX). Was this a simple buy Platts sell ASX spread trade.