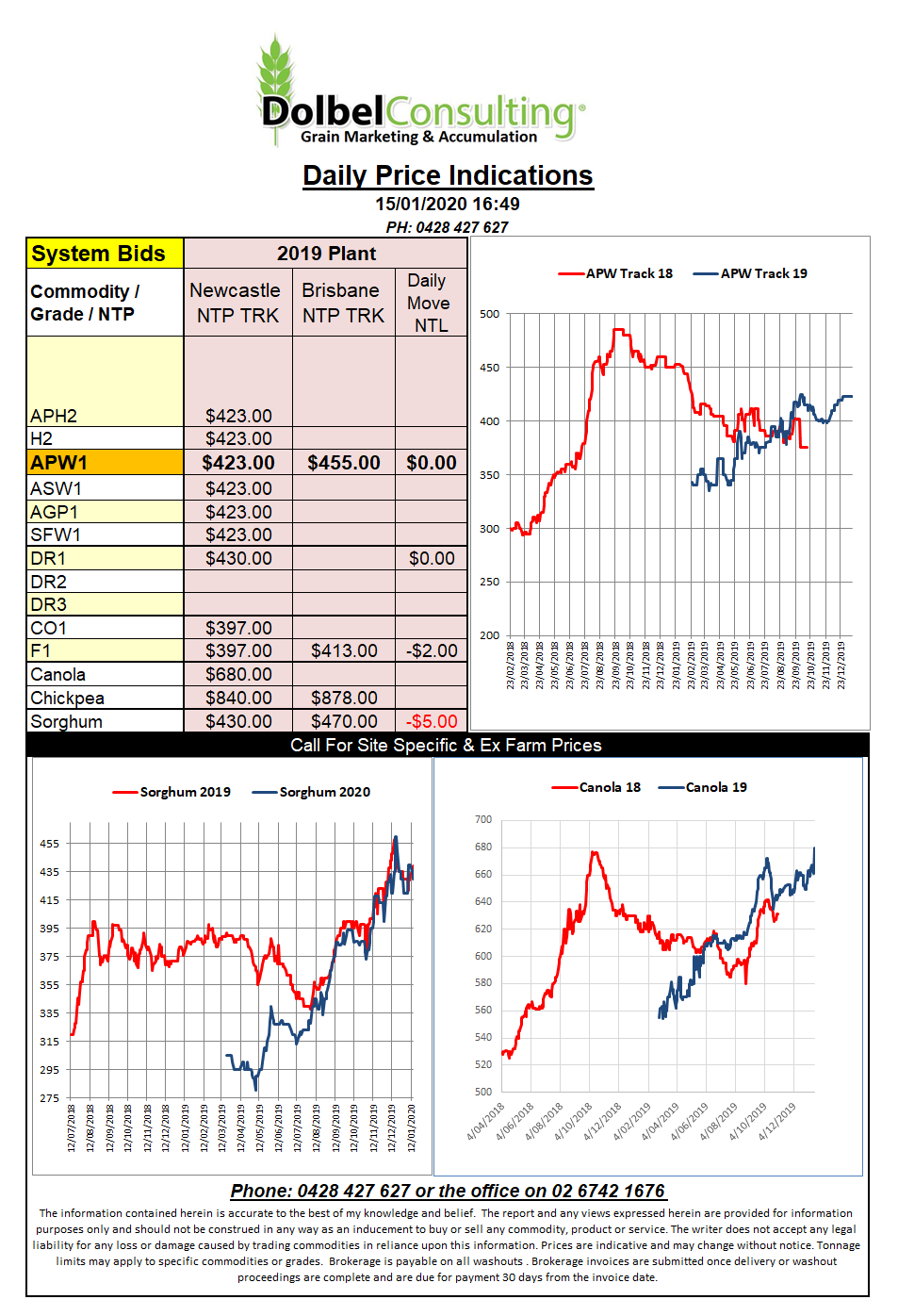

Prices 15/1/20

Hard and soft wheat contracts at Chicago continue to move higher. This has a few analyst wondering what’s going on. The Minneapolis spring wheat contract is probably wondering why it didn’t get an invite to the party too.

You would expect demand for hard wheat out of the USA to be good, it has been priced at a discount to soft wheat since October 2018. It slipped under SRWW values a couple of times prior to October but prior to 2018 this discount was almost an unseen event (and they wonder why US winter wheat acres are at a 100 year low). The reason was simple, a bumper US crop (low grade), a bumper Russian crop, a lot of feed grain in the USA and Canada and HRW had to buy demand both internationally and domestically.

The problem now is when will this discount for hard wheat over soft wheat reverse back to a traditional spread. The futures market for December 2020 has SRWW at 584.75c/bu and HRW at 532c/bu, so the punters are either getting ready to make a motsa on spread trade or they genuinely think that HRW stocks will remain burdensome in the USA for a while yet. One thing you can be sure of though is that this spread and the lower wheat area will make for some interesting reading during the March – May period this year.

Overnight Egypt picked up another 240kt of Black Sea wheat at roughly US$249 C&F. Turkey picked up 550kt of optional origin milling wheat, most assume Black Sea with some French product, time will tell. Russia needed to put some more sales on to get its export program back on track. There is also some talk of Russia restricting exports in the short to midterm, nothing confirmed as yet.