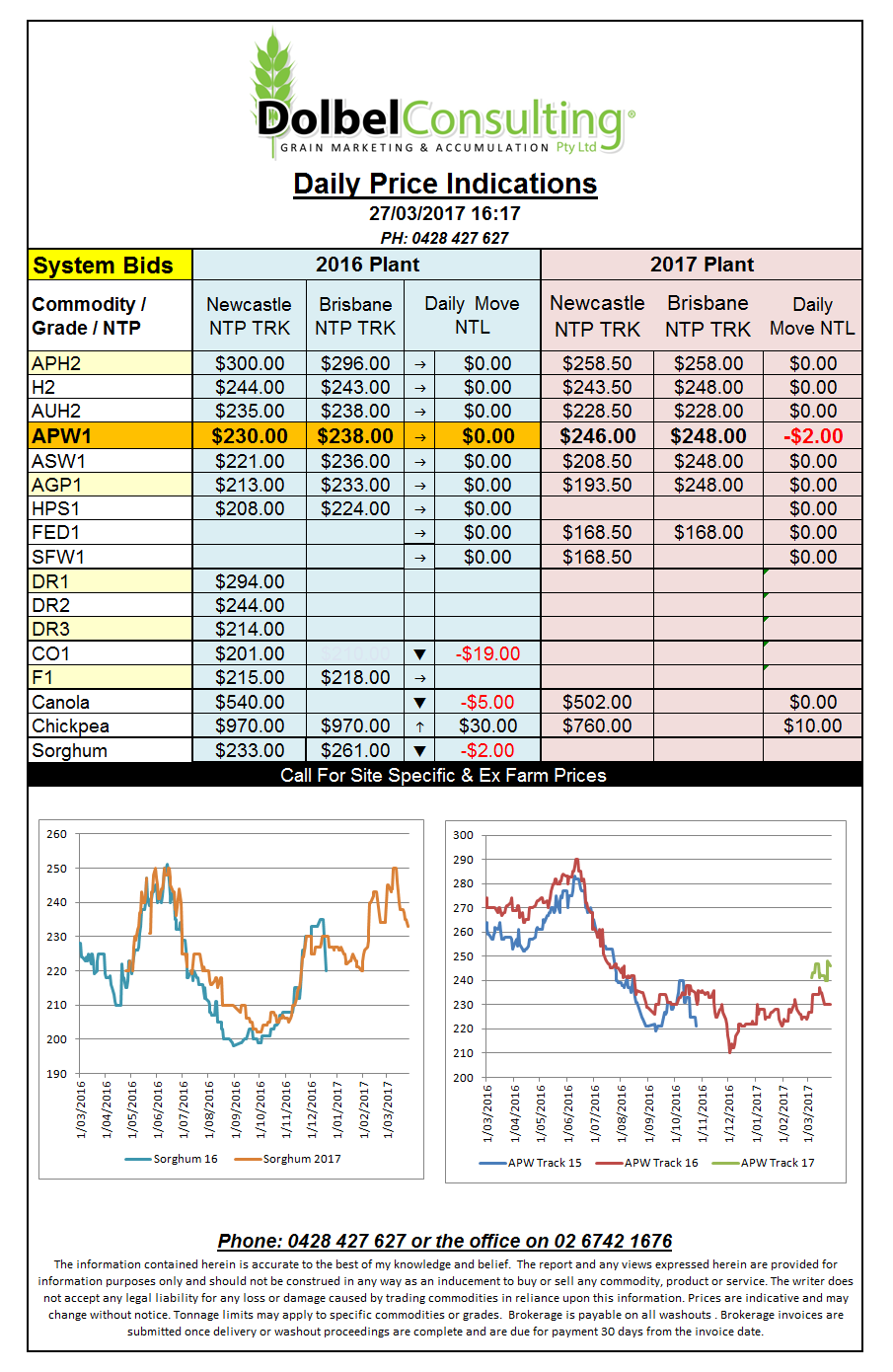

Prices 27/3/17

Better production prospects and improved logistics and weather in South America continued to influence fund liquidation in the soybean pit. Thoughts that beans will also win out in the battle for area in the USA had a negative impact.

Once technical resistance barriers were breached it didn’t matter what the weekly US sales data was, sales orders were triggered and the sell off continued. The pressure spilled over into both ICE canola and Paris rapeseed futures by the close with both contracts shedding plenty.

There is a lot of searching for direction at present, most punters are expecting it will come from the March 31st planting intentions report from the USDA. Private analyst have already suggested the US may sow as much as 89 million acres of beans, a new record. It is hard to see how new crop canola values will not be influenced by such a number and we may continue to see further weakness in new crop canola values here at least until we get a handle on what Canada has actually sown. This may not come about until May or June though, well after we should have sown our own crop.

Profit taking in the SRW pit at Chicago saw futures values there actually close a little higher but Kansas and MGEX could not muster the same support and closed flat to lower.

Canadian durum values were close to unchanged day to day with bids in central Saskatchewan averaging around C$266 / tonne.