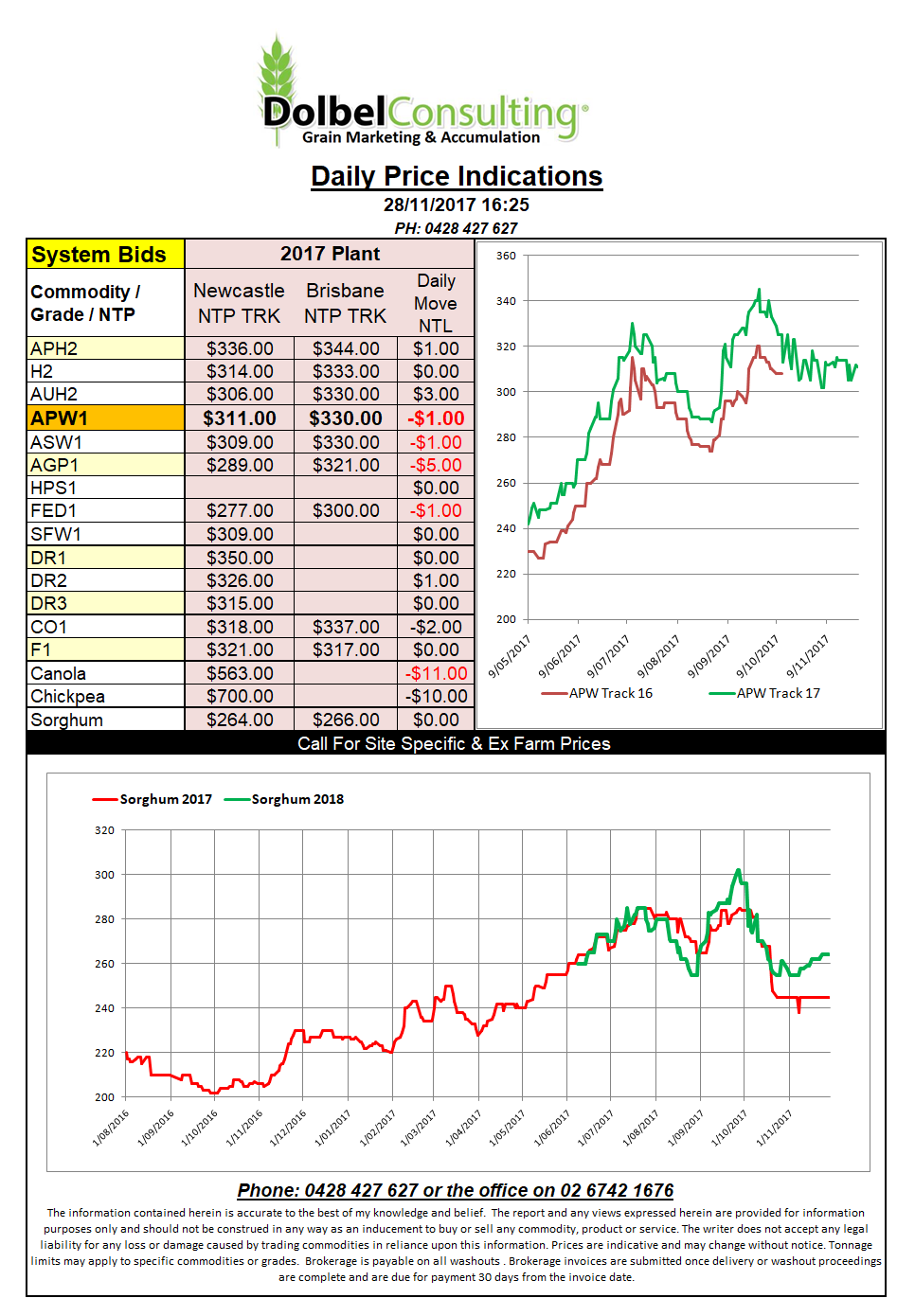

Prices 28/11/17

In 2016 the world said “grow more high quality wheat” at the time the world was awash with low grade durum and bread wheat thanks to a terrible season in the US but mainly in Canada.

Turning the page forward to 2017 and the world responded, be the size of the crop in the US and Canadian a smaller than normal crop the quality is very good.

As a result we continued to see the premium for quality shrink as we moved into the Australia harvest where the dynamics of a drought in SQLD and NNSW continued to support grain values regardless of grade. What is currently unfolding may appear a little perplexing at first but watching the international spreads for quality wheat shrink and the demand for wheat domestically increase is resulting in a rapidly closing of wheat grade spreads here in NNSW.

Yesterday APH1 was bid at $310 ex farm LPP while SFW1 wheat was trading at $285, a spread of just $25/tonne, a spread that was closer to $35 back in mid September. Local basis has not collapsed, the premium we are seeing in NNSW is still very, very good, take a look at the two charts attached. But to sustain the current values we do need to see global values stabilise at least or improve and at the moment the lack of wheat business the US is placing on the world stage is not encouraging and will continue to build world ending stocks in the midterm. The EU is finding itself in a similar position. It does tend to lead one to think is this basis we are seeing right now giving us the best opportunity or will we see better prices on the back of higher global values as we move into next M/A/M.