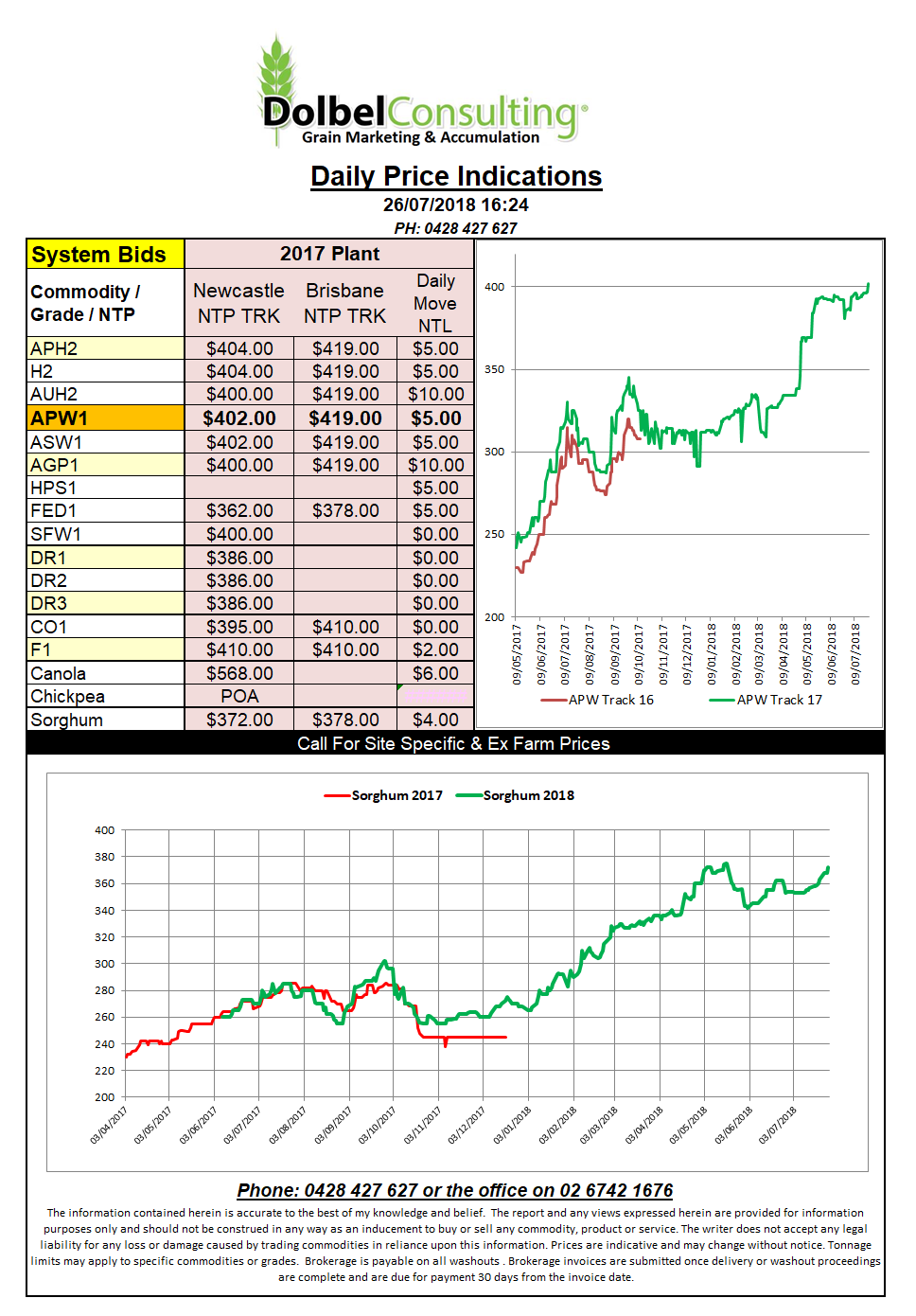

Prices 26/7/18

US SRW and HR wheat futures touched limit up in overnight trade. The driver was a combination of a poorer outlook in Europe but primarily some less than expected yield estimates from the current US spring wheat crop tour. If you believe the US wires.

Last year the producer moaned as the tour results showed there to be much more yield potential than most has thought. This year the reverse appears to be happening. Yields appear to be lower than what the trade were expecting to see.

The real smoke in the distance may not be US spring wheat yields, or even drought conditions in Germany. There are a few rumours starting to emerge that the weather damage to Russian and Ukraine wheat may well be enough to trigger an export ban at some stage. This is almost backed up by recent tender values. Egypt appeared happy to pay US$15 more and now we see some offer values for the latest Bangladesh business coming in US$15 to US$30 higher than previous tender results there.

StrategieGrains reduced total EU wheat production for the second time in 2 weeks. Potentially taking it to a six year low. Soft wheat production is expected to come in around 130mt. Durum estimates are also up in the air but are expected to be less than 10mt now.

As world values rise, so will offer values for new crop grain out of Western Australia. With the east coast at an obvious supply deficit every dollar higher in the west is likely to be reflected in the east. It might pay to watch this from a distance for a few weeks.