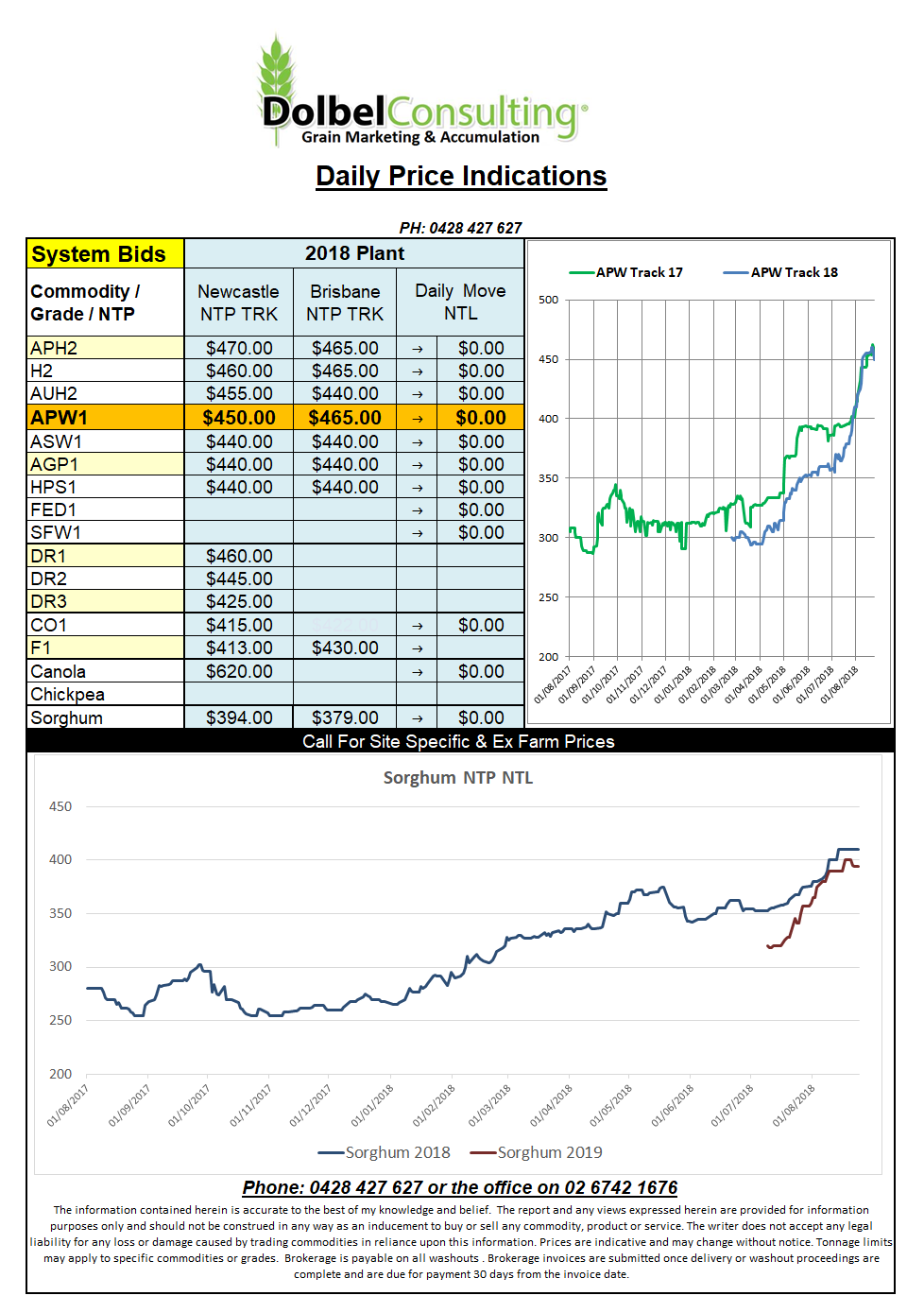

Prices 24/8/18

Soybean slipping further and a stronger US dollar all contributed to a poor performance in wheat futures at Chicago. US weekly export sales were not very impressive either with just 240kt of wheat sales made. The punters had pencilled in orders for about 650kt so the 240kt number really took the wind out of their sales.

Weakness in the soybean market spilled over into both ICE canola and Paris rapeseed futures.

Corn futures in the US continue to struggle as the season as thrown up very few significant challenges and the crop is likely to yield to its full potential this year.

The IGC put out their monthly estimates last night. Wheat production is now pegged at 721mt (758mtLY). Ending stocks are expected to fall from 265.4mt last year to 247.2mt. Consumptions was raised 3.2mt to 739.2mt.

This still represents a stocks to use ratio of over 33%. We really need to see this ratio down into the 20%s to put a fire under this market.

Taking China out of the equation on both sides of the ledger does tend to shed a new light on just how tight things are getting but the trade don’t like to focus on that, at least while talking to producers. The IGC has come up with a world wheat ending stocks number much lower than the one the USDA found in the August WASDE report, IGC 247.2mt vs the USDA @ 258.96mt.