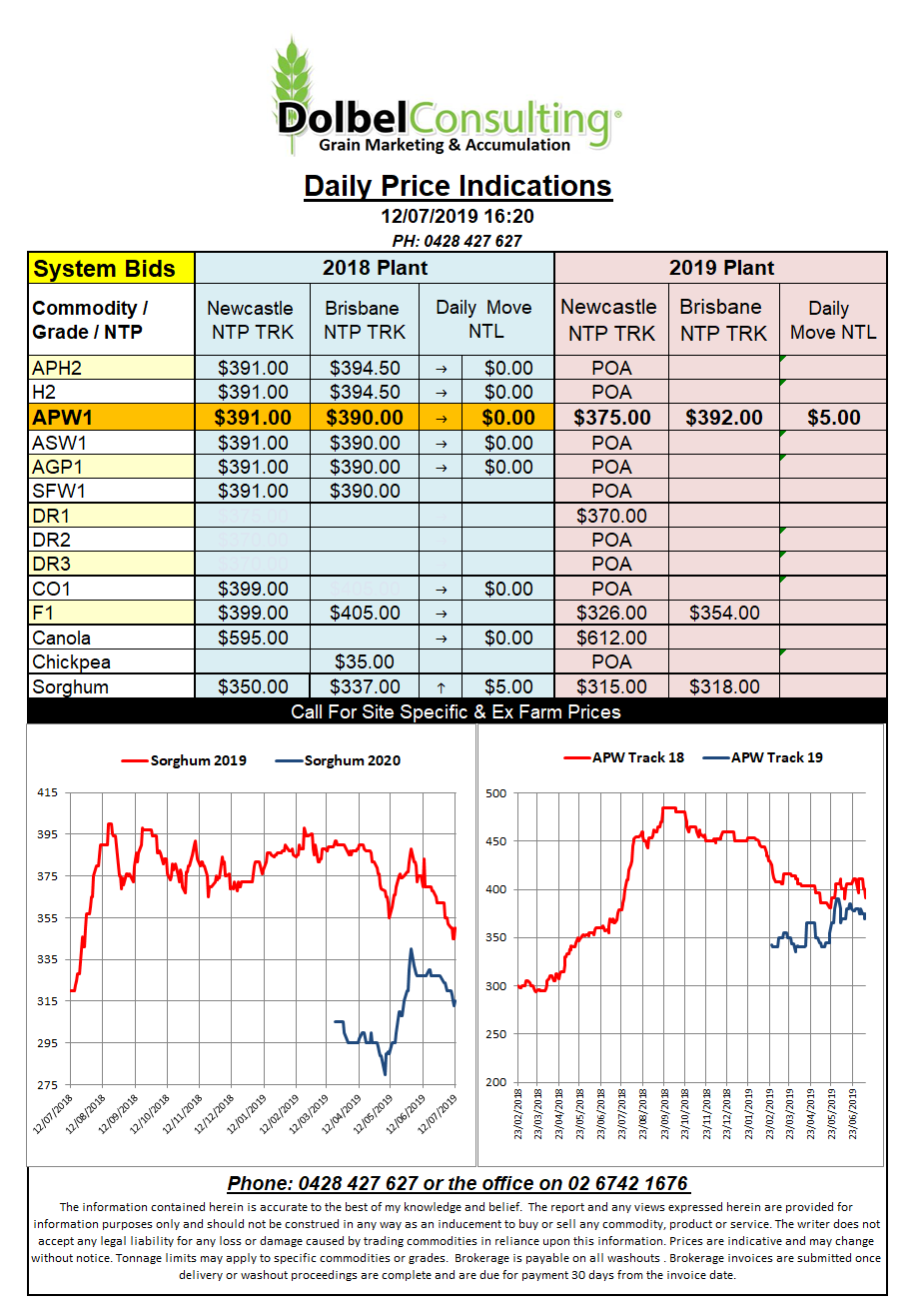

Prices 12/7/19

Well the big news is the wheat numbers are in the WASDE report, let’s have a quick look.

Global wheat production was cut by 9.37mt to 771.46mt, not a small crop by any means but a cut larger than any trade estimate. The S&D sheet also shows cuts to consumption but the USDA still came up with a 7.88mt reduction in carry over stocks, now just 286.46mt. Once again not exactly a small stock level and still represents a stocks to use ratio of over 37%. This really needs to be under 30% to get some mild panic in the market.

The USDA also came out with their estimate for “the world less China”, this ratio comes in at about 22%, which should be supportive as we know Chinese wheat will not move onto the International market and the only real reason the world takes any interest in Chinese wheat S&D is in the rare instance they become a net importer.

So the big changes for wheat are Australia from 22.5mt to 21mt, most private estimates I’ve seen for Australia are now under 20mt. Canada was 34.5mt now pegged at 33.3mt, Russia went from 78mt to 74.2mt, Ukraine slipped 1mt to 20mt. One number I find surprising is a rise in Kazakhstan from 13.8mt to 14mt. The EU slipped from 153.8mt to 151.3mt. Carry over stocks in the major exporters are expected to shrink to 32.34mt while the major imports will see a carry over of about 189.23mt, that’s the bad number in all of this.

The other number we were hanging out to see was the US and Chinese corn estimate. The US had a June estimate of 347.49mt July is surprisingly 352.44mt while China stayed unchanged at 252mt. So there’s still plenty of scope for movement in the August report.