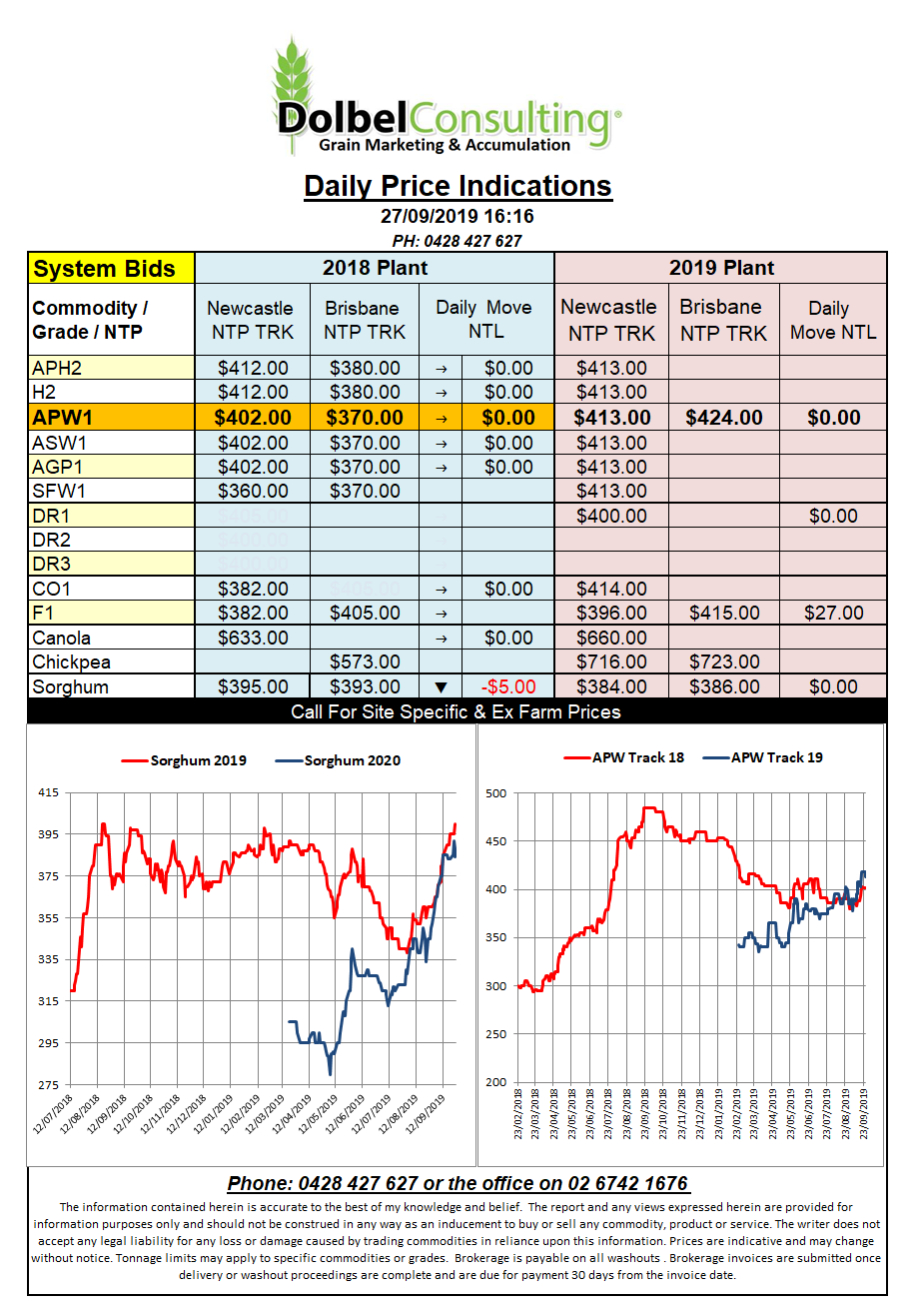

Prices 27/9/19

Wheat futures in the US saw a reversal on what has been happening all week. Last night spring wheat futures fell away while soft and hard red winter wheat futures moved higher. Spread trade & profit taking maybe, technical trade most likely.

There’s no new fuel for the fire with global wheat estimates fairly flat in the latest IGC report. Wheat production is pegged at 764.1mt a new world record and about 31mt higher than last year. Ending stocks are still set to finish the marketing year around 6mt higher than last year at 270.6mt. A stocks to use ratio of 35.6% isn’t exactly a number that will drive markets higher. We really need to see it closer to 20%.

The USA continue to remain ahead of last year’s sales pace for wheat. At 12.6mt that is roughly 16% ahead of this time last year. Mexico and Asian markets continue to be the main destinations but recently sales have also been reported into Egypt and Yemen.

African Swine Fever continued to spread through Asia this week with cases reported in Korea, Philippines, Vietnam and continued cases in China. There are significant changes to the meat market in China with imports jumping 26% year on year for pork alone. Total meat imports are said to have risen by about 42.5% year on year. The production dynamics in China are also changing with bigger farms being able to take the chance of restocking pigs more so than smaller producers. The disease is actually pushing the industry into larger scale production and efficiency improvements. The smaller farms cannot take the production risk.