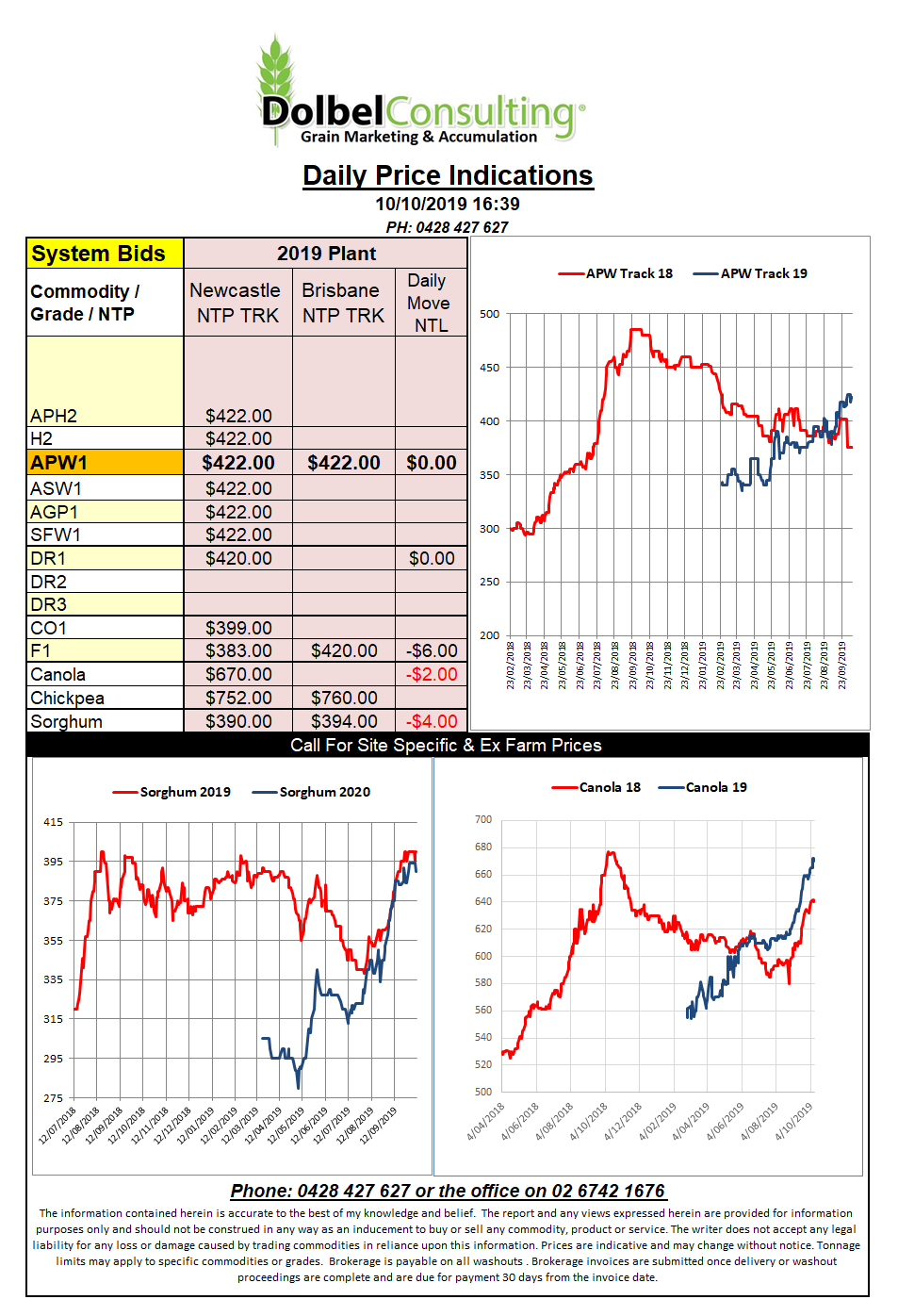

10/10/19

With a USDA report due out tonight it was never going to be a huge night of changes at Chicago. The trade wanted to rally on the back of an approaching winter storm in the USA but caution won the day and the punters generally squared up ahead of the Oct WASDE.

The China / US trade negotiations also fuelled the usual level of speculation assisting the stock market and energy futures higher.

At the cash level in the US there was a little firmer basis in some Midwest elevators trying to cover last minute corn demand before the winter storm hit.

Further north in SW Saskatchewan we see spring wheat values continue to soften while 1CWAD13 durum remains firm. Cash bids ex farm for 1CWAD13 for a December pickup are indicated at C$269.44 / tonne. A back of an envelope conversion would see this equivalent to roughly AUD$480 – $490 NTP Newcastle. This may be a rough guide for future DR1 sales values off the LPP.

Over the last couple of years China had sustained a fairly active auction system for state owned corn in an attempt to reduce stocks to a more manageable level. With the volume of stocks now down to a more modest 56mt there is even talk that China may abandon the recently introduced ethanol mandate. This could have two side effects for corn and ethanol. One would be the obvious decrease in corn demand to make ethanol domestically the other would be a lack of interest in importing ethanol form guess where………that’s right, the USA. If you throw the ASF problem into the equation it does tend to make you wonder where corn stocks will start to head.