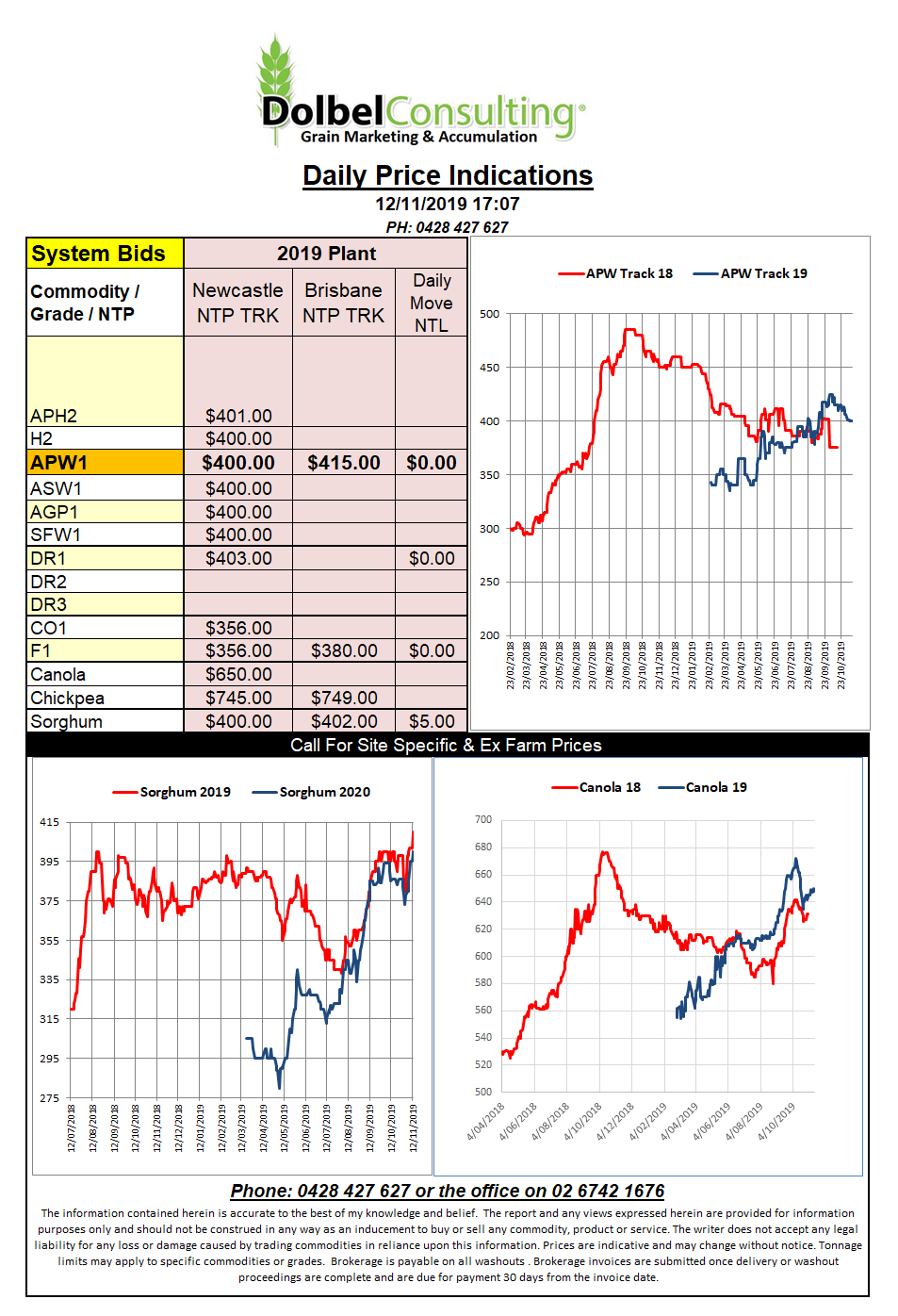

Prices 12/11/19

With the US markets closed for Veterans Day we turn our eye to the European markets for data. Milling wheat at Paris was a little lower closing the session for the December slot at E177.25 / tonne.

Offers at the FOB level in France were closer to US$202. This would indicate that futures are around US$6.50 under physical there at present. The futures contract, like most is a FIS contract, in this case free instore at Rouen or Dunkirk.

So we have French wheat at US$202 + freight of say US$18.00 to Egypt, so US$220 C&F. Black Sea wheat at US$208 + US$16, so US$224 to Egypt. Ukraine wheat is about US$5.00 lower than Russian with similar freight. Romanian wheat is somewhere between Russian and Ukraine. So Egypt is steady at around US$220 delivered. The USA though is there at US$212 + freight of around US$30, so US$242 C&F Egypt, some US$20 out of the money. That’s about 54c/bu. Now HRW futures are already trading at 430c/bu. Back in 1999 wheat drifted as low as 201c/bu. If you applied a 2.5% CPI to this number you come up with something close to 365c/bu after 20 years. I know CPI has little to do with reality let alone farming but run with this. The question we need to ask is, can HRW fall to a price of US$367c/bu and I guess the answer is, if we are heading to the worse international price the US has seen in 20 years, than the answer is yes. Just to drive this home a little deeper we need to look at global stocks to use ratios for then and now and unfortunately 1999 actually had a lower stocks to use ratio than 2019 by quite a lot. We really need the USA to reduce ending stocks of wheat by about 50%.