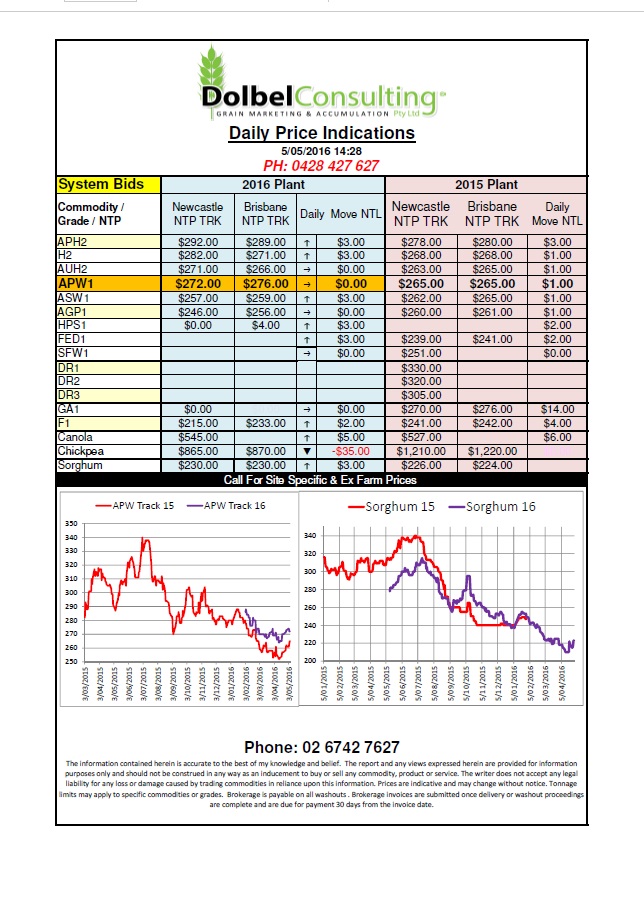

Prices 05/05/16

The European soft wheat crop just keeps getting bigger, it’s not quite as big as last year’s crop of 151.3 million tonnes but at 148.2 million tonnes it is not that far behind it. Ending stocks are expected to increase by 600kt to 189.1mt….too high.

Saudi Arabia picked up 620kt in their wheat tender last week with prices varying between US$210 and US $220 C&F for Aug / Sept delivery. Black Sea exports remained brisk last week with the Ukraine shipping 237kt of wheat, 106.7kt of barley.

In the US, crop tour scouts participating in the HRW crop tour across Kansas continue to report better than average crops. There were some reports of disease but generally the SW of Kansas is looking good after rain a couple of weeks ago.

The Indian government continues to try and reign in pulse prices with the release of state owned stocks onto their domestic market. Some say what the government is doing is not enough and that only filling a quarter of what is needed is not reducing prices significantly. 2015 / 16 chickpea imports are up 152%. Around 650kt of Australian peas have arrived in India according to official Indian data, we all know it’s more. 2016 production is pegged at 8.09mt, up only 10%, some say this is overestimated by 25%.