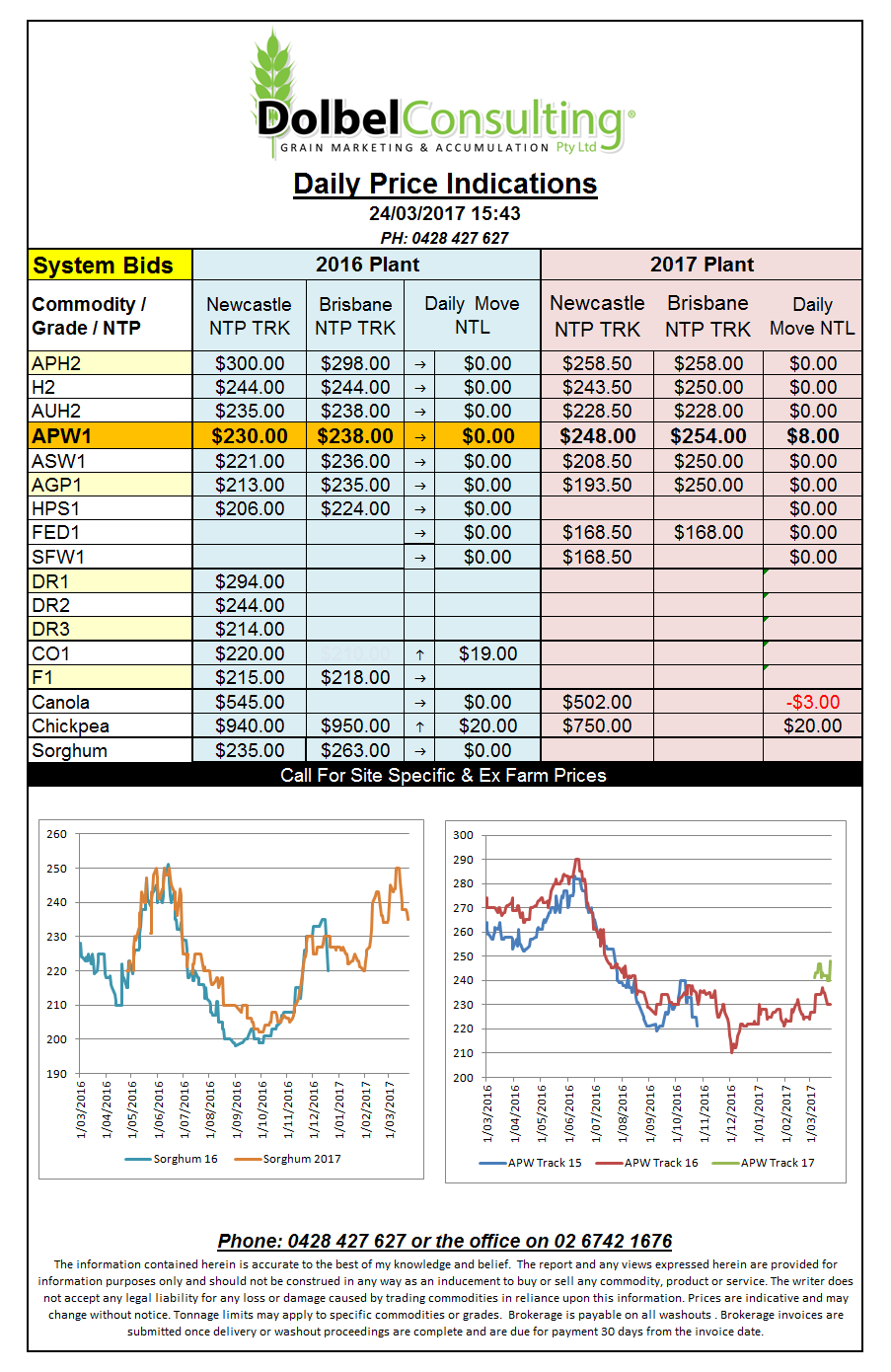

Prices 24/3/17

The weather map for the US wheat belt looks good for east of the Mississippi and north of Kansas but for a large slice of the hard red wheat belt the map isn’t as promising as some market wires might lead you to believe.

Initially wheat futures in the US were firmer but fell away as the session went on only to close the day lower at Chicago and Kansas and very little gains for Minneapolis.

The funds continue to square up leading into the March 31st US sowing report and this is the major market moving in the short term.

The key to the fund money appears to be talk that Trump won’t get the amendments to the healthcare act through. These “amendments” were the means to fund much of the stimulus in the US according to some commentators. So no amendments, no big growth, no big growth and Wall St will get bored and sell the US stock market down, the USD will fall, and yada yada.

Canadian durum values remain mostly unchanged with bids in central Saskatchewan steady at C$266 / tonne for 1CWAD. Spreads from 13% protein to 12.5% protein 1CWAD are roughly -C$1.15 / tonne while spreads to 2CWAD at 12.5% protein are around C$36.00 / tonne. So vitreous remains the major determinant to prices there.

Talk of India being unable to build any type of reserve stocks of chickpeas leading into 2017-18 is driving prices higher.