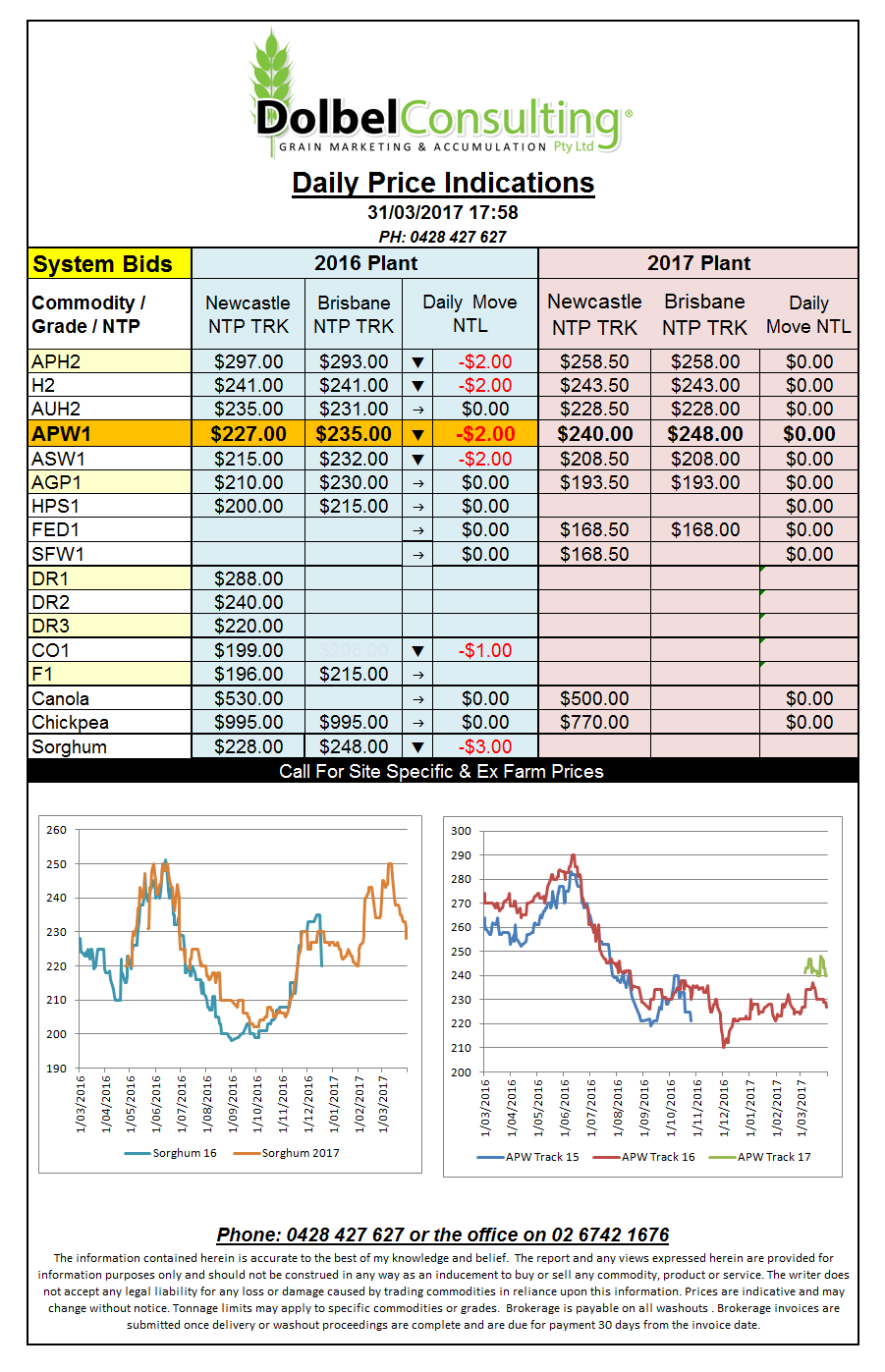

Prices 31/3/17

US grain futures were generally lower across the board with weakness leaking into the ICE and Paris canola contracts as well as London and Paris wheat. Futures at Chicago are generally oversold and should start to see some technical support as we move into April / May. This will depend a lot of the spring conditions for wheat and the pace of summer crop sowing in the US and Europe.

From a global perspective we should see lower wheat acres, some countries that are currently enjoying a weaker exchange rate may look at increasing production but generally speaking lower production in the US and Australia is likely to counter these increases.

The 200kt Algerian durum business done mid week was said to be priced around US$253 / tonne CAF. Punters are yet to get the supplier confirmed but expect it to be mostly Canadian and possibly US durum. Let’s have a look at wheat US$253 may equate to if Aussie durum was to be used to supply. Freight to Algeria from Australia is roughly US$34 / tonne. So that would equate to about US$221 FOB Australia or AUD$290, less around $30 to put it on a boat would make it about $260 NTP equivalent. So priced somewhere between our current DR1 and DR2 values, I’d love to know what quality they actually ship. With central Saskatchewan values still around C$255+ / tonne for 1CWAD you would have to assume quiet a low grade, maybe even a No3.