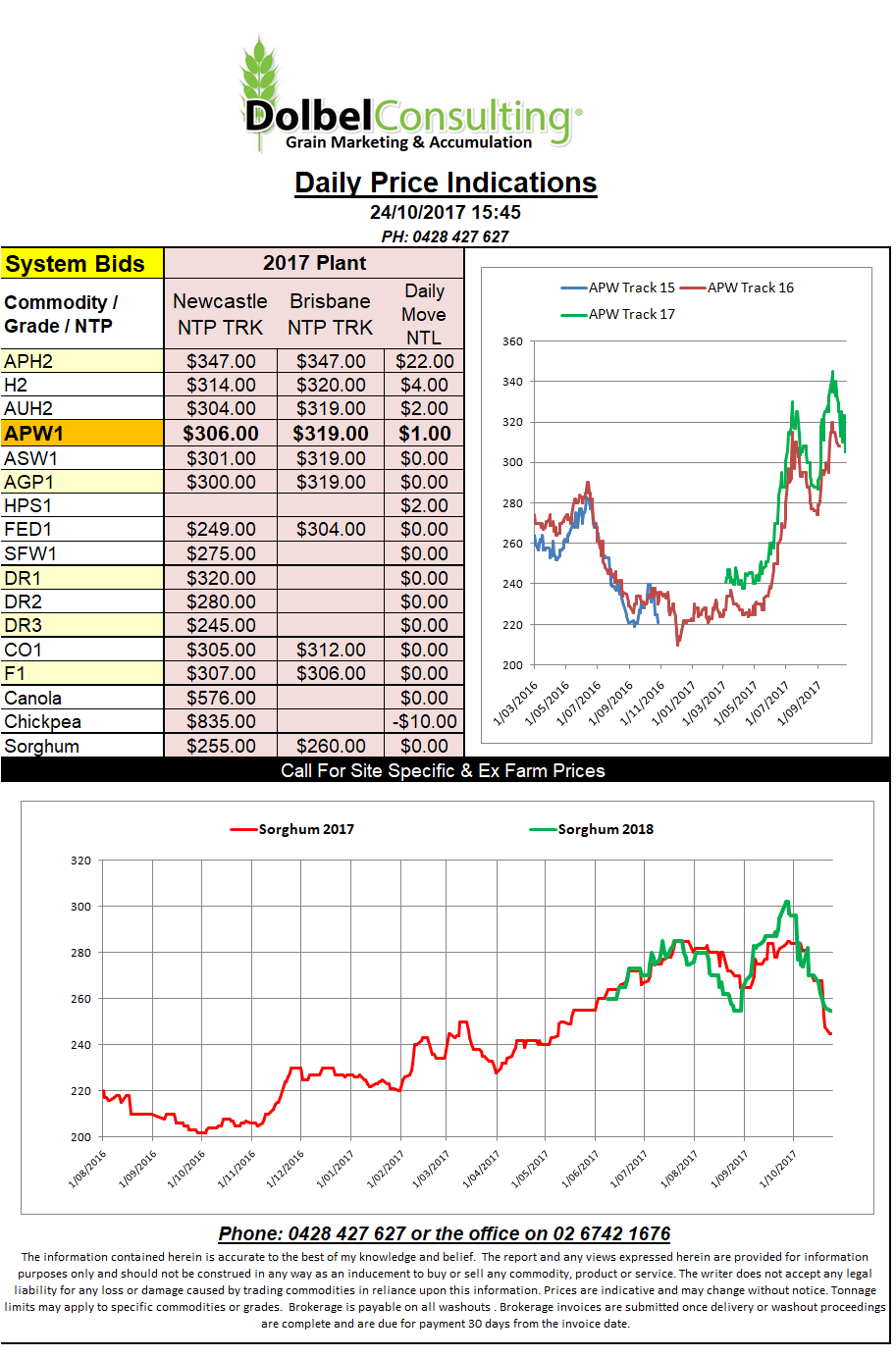

Prices 24/10/17

The funds continue to influence US futures values. Using weekend rain as the catalyst to square up some spread trade the funds cleared shorts in a number of soft commodities. Soybeans were a major benefactor of fund money with a net long being consolidated. Rainfall is expected to make for a slow start to the US row crop harvest this week but the GFS model does indicate a mostly dry week ahead apart for some clearing storms across the upper east. Hard red wheat was the best performer overnight but with ideal new crop conditions and poor weekly US sales don’t expect the rally to signal a huge turnaround.

China will offer 4.7mt of corn to their domestic market. This is corn from the 2013 – 2014 harvests so there is a degree of scepticism over quality. In recent auctions the volume on offer is generally much, much higher than the amount that is sold but it does give the market an idea of import values for both sorghum and corn.

Chickpeas for the January contract at the NCDEX were down sharply. Values equate to around AUD$810 at the Narrabri packer a fall of roughly AUD$30 / tonne. Trade was low due to adequate stocks and limited demand according to some analyst. They don’t want to risk telling anyone that the move was due to speculative liquidation now do they, last time the Indian government got wind of speculation in the chickpea futures market they shut the contract down.