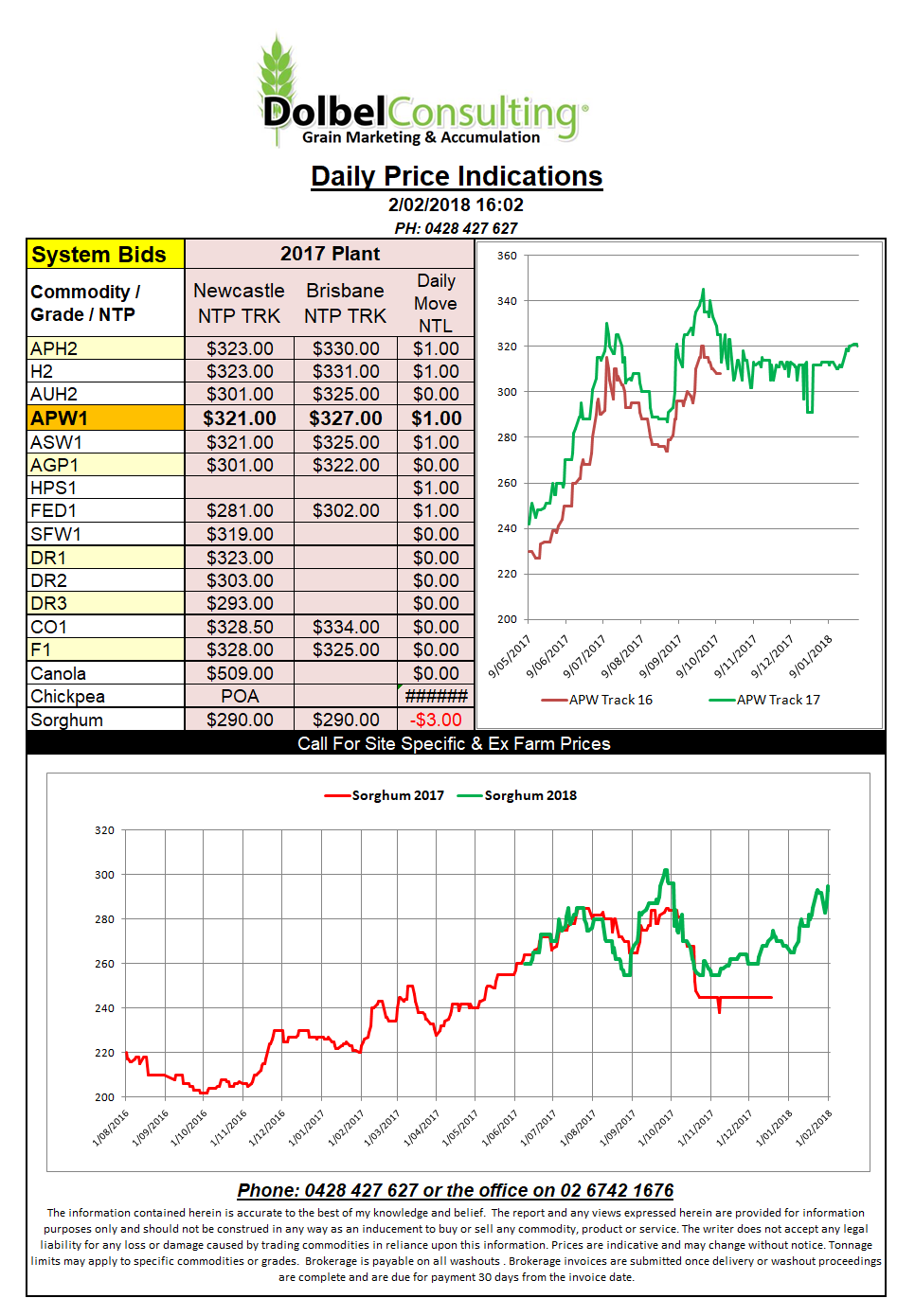

Prices 2/2/18

We have a few reports out next week that may breathe some life into US futures markets. On the 8th we have the USDA supply and demand report and on the 5th we see the StatsCan stocks report for the end of December. Neither are expected to hold any big surprises apart from potentially increasing wheat stocks in both nations.

Canada are still up in arms over the country of origin labelling laws being introduced in Italy. It’s not so much that they don’t want the consumer to know it’s Canadian wheat, it is more of a case of who is going to bear the cost of segregation if product lines cannot be blended.

At Chicago soybean futures were lower early on poor weekly export data. Values never really recovered and apart from some midsession correction the contract was set for a lower close, and that it did. The weaker soybean market spilled over into ICE canola which also slipped lower. Paris rapeseed wasn’t about to help anything either. Talk of bigger canola acres in eastern and western Europe this summer thanks to low wheat prices is continuing to thwart any attempt in international canola values to push higher.

A late session rally in Chicago wheat pushed the market back to where it started. The dry weather in the US HRW belt continues to counter concern over growing wheat stocks and poor weekly exports.

Chickpea futures are mixed, firmer yesterday and softer today. Converted to a Narrabri price futures would come in around $580. The import duty into India continues to muddy price discovery but if you use that figure as an indicator for Pakistan business it’s close.