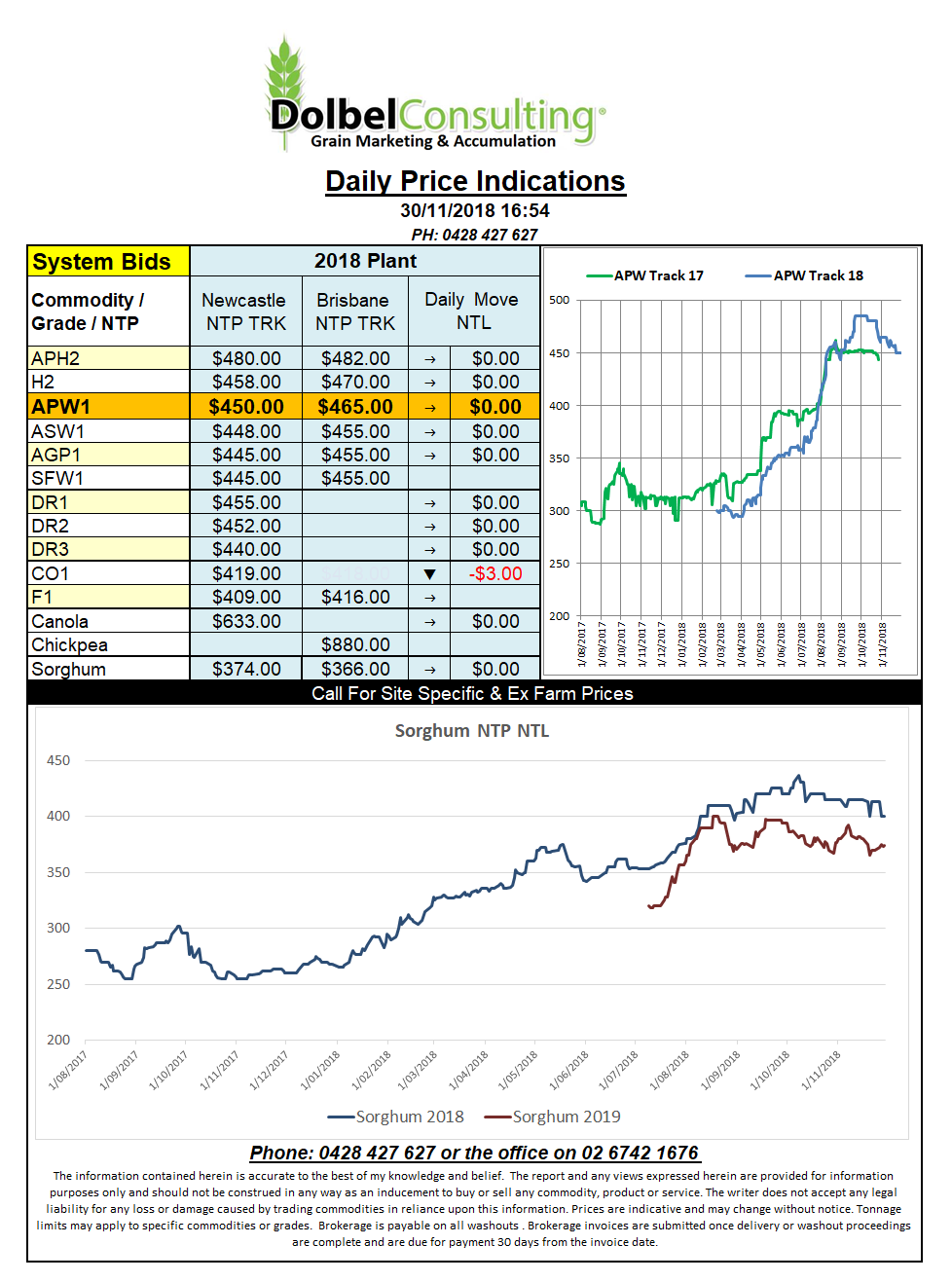

Prices 30/11/18

Further selling in the Chicago wheat pit has wheat continuing to push into the oversold side of the equation. Once December is out of the way we should see March find, if nothing more, technical support into the new year.

Generally speaking the markets appear to be hanging on possible trade talks at the G20. It is hoped the USA and China thow water not petrol on the trade fire they both appear to be happy to stoke at present.

What is it with US corn futures, weekly export sales of 1.26mt and they still succumb to technical end of month selling. Corn did fare a lot better than US wheat though. Weekly US export wheat sales totalled just 250kt. This now means that the USA will need to sell about 675kt per week throughout the balance of the marketing year to meet USDA projections, good luck with that.

In Europe recent rains and the prospect of more is starting to put a dint in a very hot dry summer. River transport was and still is becoming difficult in parts of western Europe but additional feed grains from Ukraine and Bulgaria are making there way to where they are needed.

Russia should sow about 45 million acres of wheat to harvest in 2019. The punters are predicting a crop of about 77mt off that area. This would make Russia a formidable force in the wheat export market again in 2019 / 20.