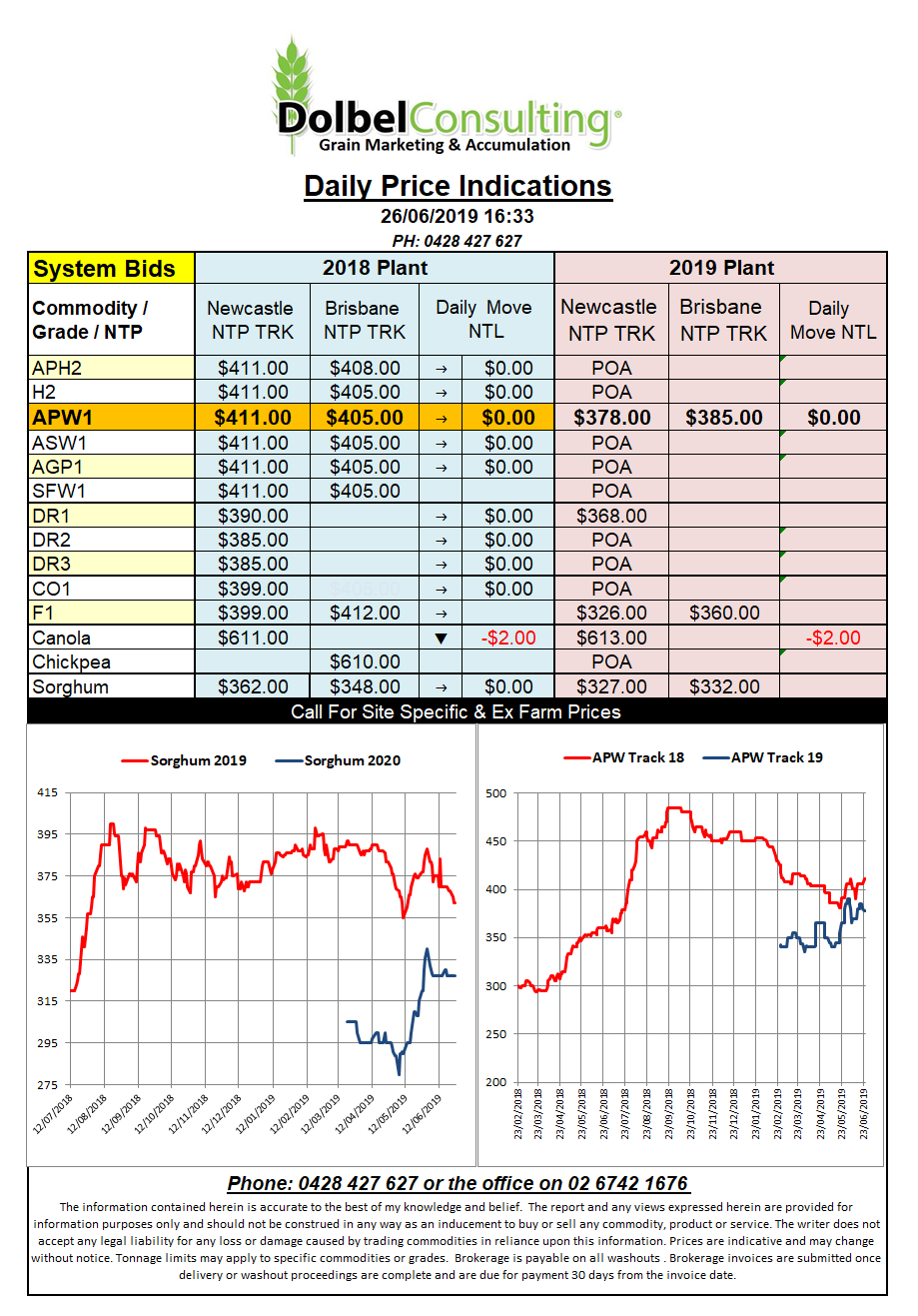

Prices 26/6/19

Canola futures at the ICE were crushed in overnight trade. The November contract was off C$9.00 / tonne by the close, January was back C$8.70. This recent fall puts the downside in canola futures at C$21.70 or 4.54% over the last 3 months. The November contract is still C$10.20 higher than the low set back on the 6th of May but keep an eye on this week’s StatsCan report.

The downside in futures was attributed to recent rain and the prospect of further rain across much of the canola sowing districts of Alberta and Saskatchewan. According to some reports the rain was patchy though and drought condition persist in some pockets. In other parts like SW Saskatchewan up to 60mm has fallen at a time many believe will save the crop.

The region also produces the bulk of Canada’s durum wheat. Cash prices for 1CWAD13 across SW Sask have flattened out or actually slipped away a little in some locations. At C$235.00 per tonne durum is priced about the same as 13.5% milling wheat.

Wheat futures in the US were lower on the back of drier weather expected across the bulk of the HRW belt over the next 7 days. The same cannot be said for Iowa and Wisconsin where the 7 days model predicts 2.5″to 4″ may fall. The S&D sheet for the US is going to take some sorting out with lower corn and soybean production a key feature while wheat volume and quality will also play a major role. The soft season for much of the hard red wheat and soft red wheat area and the threat of scab will make working out the feed grain S&D difficult. Will wheat fill the gap in the corn demand or will the feed grain wheat be full of head scab ?