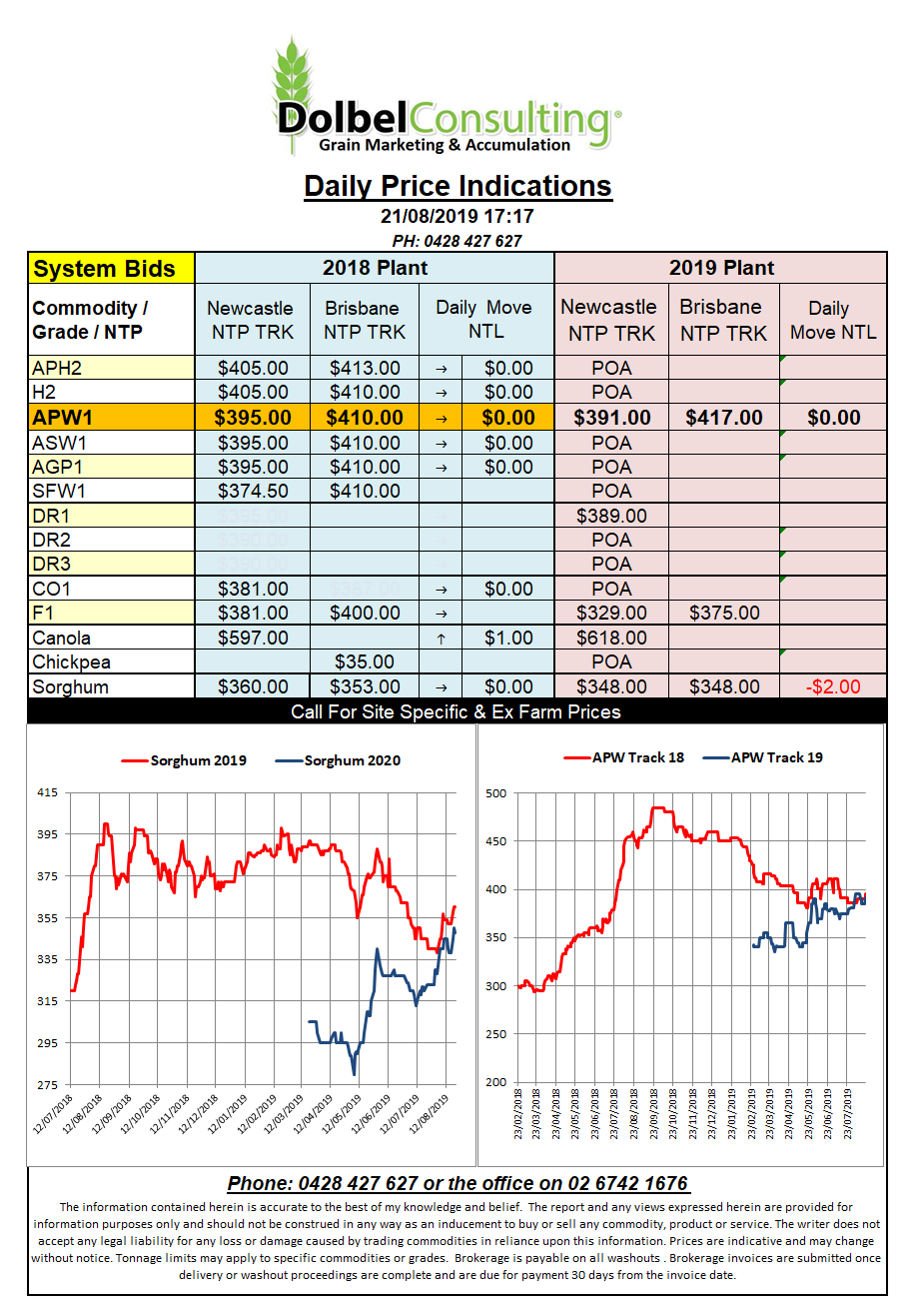

Prices 21/8/19

Hard red wheat futures in the USA continue to reflect the plight of the trade finding it hard to market a low protein crop. The normal consumer for HRW is looking for a product about 12.5% protein but the soft finish this year has seen protein’s average in the mid to low 11% range. This has meant that HRW is basically competing into the feed market and is priced accordingly.

Hard red spring wheat values are reflecting the premium expected of a high protein wheat but we are also seeing better high grade wheat out of the Black Sea and Europe this year, so most punters are expecting a tough road for wheat values at a global level for the next 6 months.

Having a better quality wheat crop in Russia isn’t all beer and skittles for them though. In theory it gives them a more expensive crop to market. Some are saying this is the reason Russian exports have slowed in recent weeks. Currently Russian wheat exports are 11% behind this time last year at just 5.1mt. In order to stimulate throughput some terminals at Novorossiysk on the Black Sea are offering a discount of US$7.00 / tonne (20% – 30%) in handling costs for those that meet their allocated export quota.

Japan picked up a parcel of US white wheat in their latest tender. White wheat out of the Pacific North West is offered at US$225 for 10% protein. APW1 wheat out of the west coast of Australia is offered at US$230. There’s about a US$8.00 freight advantage to Australia so price wise Australia simply missed the business. Potentially better margins are offered on the Aussie east coast.