5/11/20 Prices

Indian chickpea values, although softening, are still paying a premium for N/D/J delivery versus March +. The NCDEX futures contract actually shows a discount of about AUD$75 – $80 per tonne for nearby versus March. This does tend to indicated that a marketing program more focused on the short term than the long term maybe the best option given current conditions.

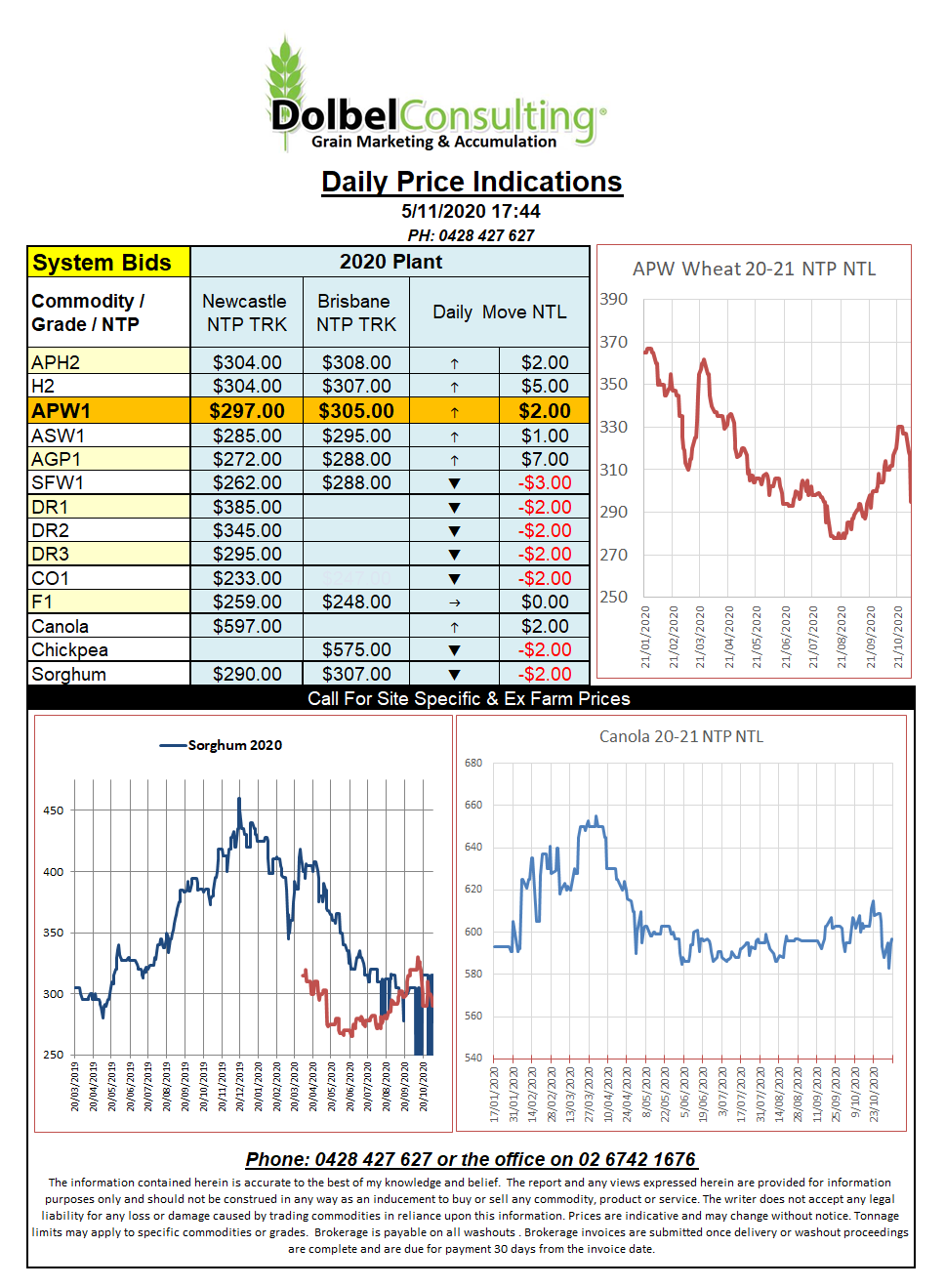

Canola futures at the ICE and Paris rapeseed futures both saw some good upside on the back of higher US soybean futures at Chicago overnight. The firmer AUD isn’t helping us a lot but the move in ICE canola futures, when taking the AUD move into account, represents a potential gain in values about AUD$3.50 today. We did see local basis back up over AUD$20 yesterday which was a promising change from days of basis reductions. With China expected to increase purchases of US soybeans and Brazilian stocks depleted we should start to see fundamental support for canola in the short to mid-term. Last night’s soybean rally at Chicago was also helped along by a jump in palm oil prices early in the session, another side effect of the dry weather in Brazil.

Cash prices for canola in SW Saskatchewan were firmer, rallying C$5.42 for a December lift. Still in SW Sask we see durum values were a touch lower, shedding C$1.65 per tonne to be bid on average at C$293.61 for a December lift. On the back of an envelope this would convert to about AUD$412 at the port using today’s exchange rates and summer basis for the Prairies.

Look for continued support in oilseeds while cereals are likely to stagnate in the short term.