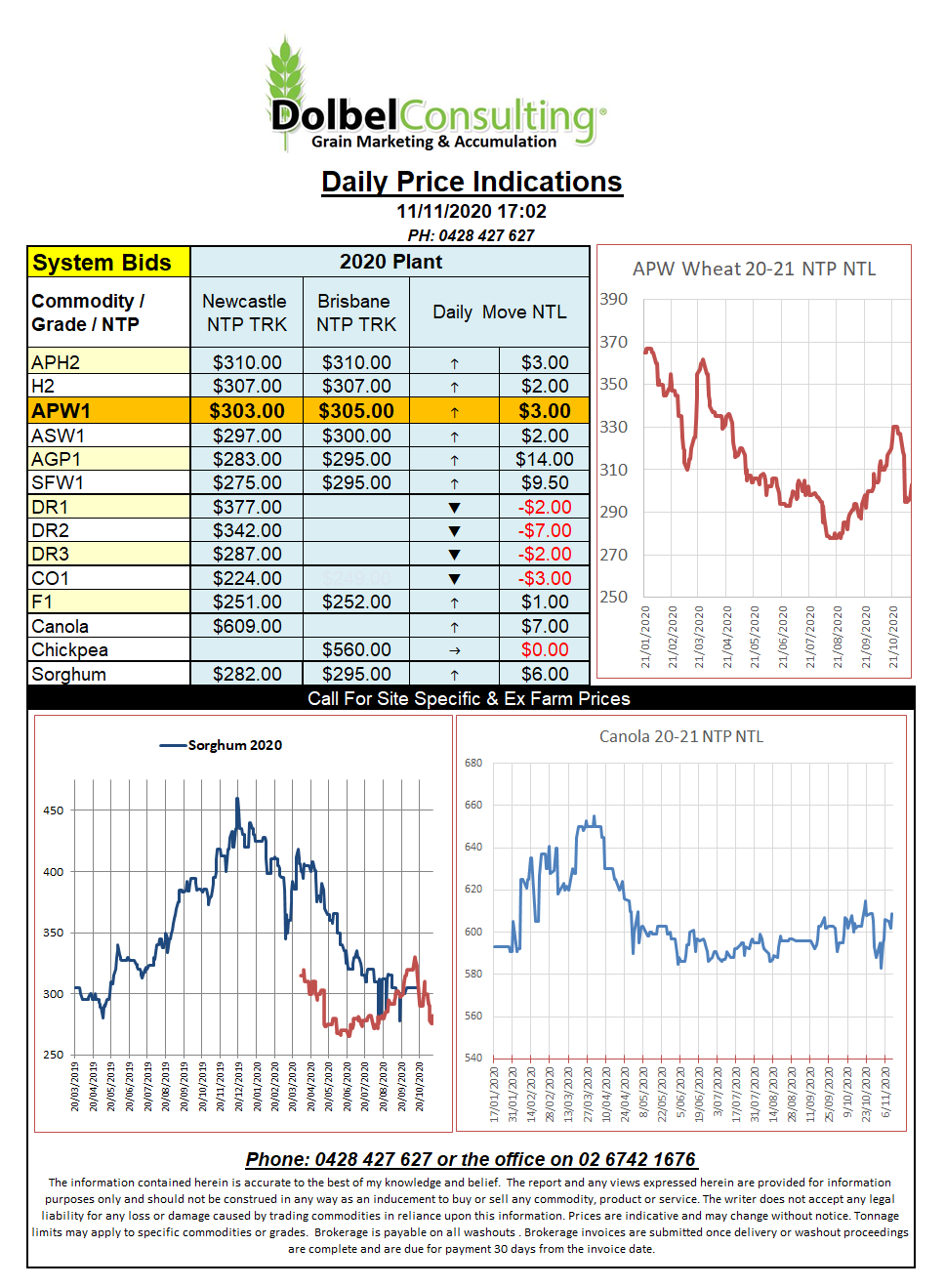

11/11/20 Prices

The November USDA WASDE report was out last night and if anything it could be viewed as positive for wheat. World production was marginally higher at 772.38mt, yes that’s big but it’s smaller than many had expected to see. The carry-over stocks were reduced 1mt to 320.45mt. Looking through the numbers we see the Aussie production estimate was left unchanged at 28.5mt, that’s a bit of a surprise but Argentina was only reduced 1mt too, that could have been more. The EU was back a smidge but Russia was increased 500kt. Other than those minor moves there wasn’t really much more on wheat that is worthy of a mention.

The big moves were in corn and soybeans. Corn futures at Chicago are up 15.5c/bu this morning. That’s the biggest daily move since October last year. A reduction in average US yields saw production there fall from 373.95mt to 368.49mt. Combine this with reductions in Ukraine, the EU and Russian and it easily counters the rise in production for S.Africa. World ending stocks were reduced 9.02mt to 291.43mt.

Soybean production was back 5.83mt globally and ending stocks were back 2.18mt. Reductions in the USA & Argentina were the key. The strength in soybeans spilt over to both the ICE canola and Paris rapeseed futures contracts. This, in theory, should lend support to local cash prices for canola here today unless the trade smash basis for six again. One might extrapolate from this that those importing countries that have been sitting on the fence regarding wheat, corn and soybeans may actually come to the market now.

Export sorghum may yet be the big winner here once the trade take their eye off wheat and barley.