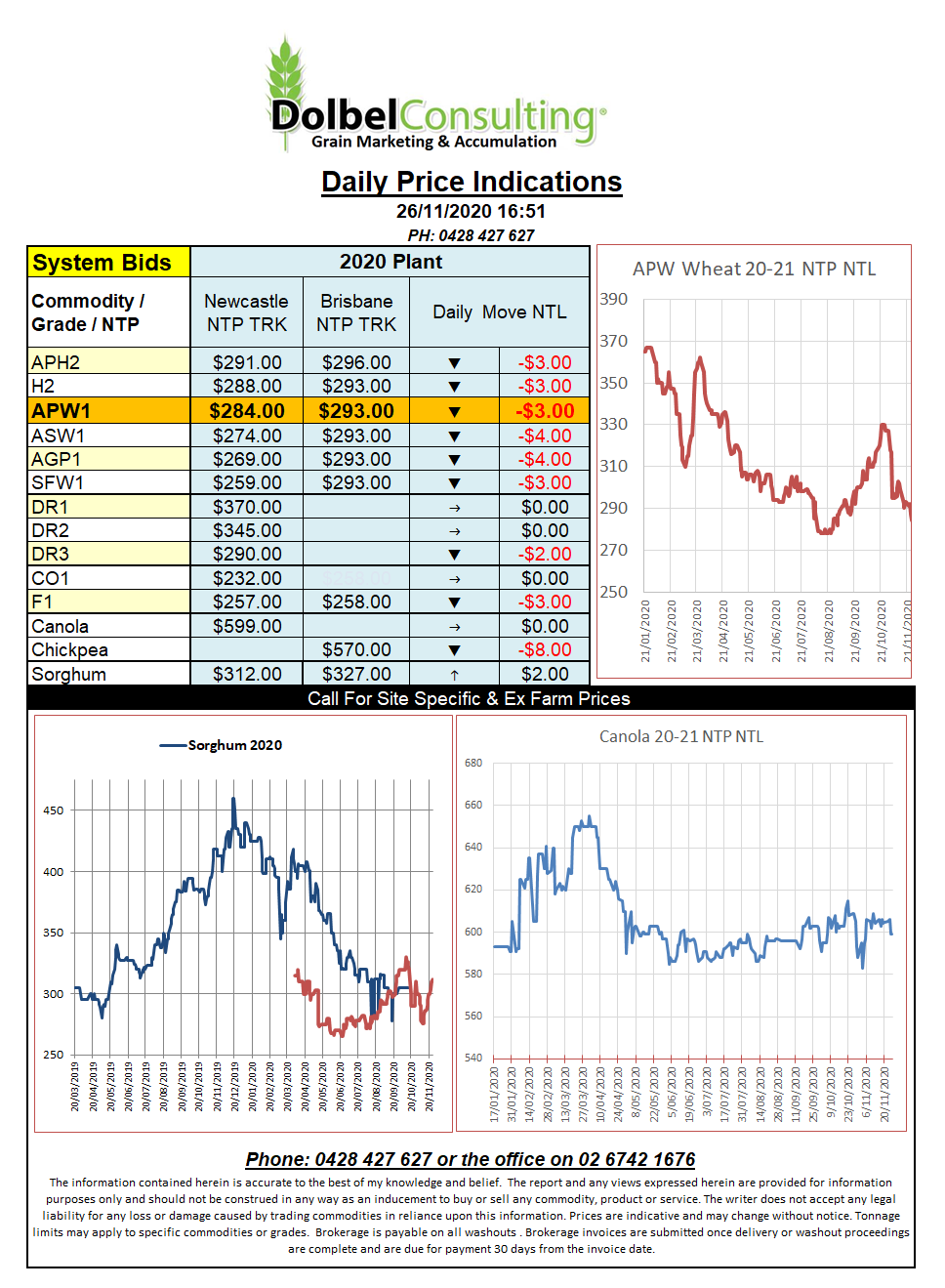

26/11/20 Prices

The prospect of higher ethanol stocks in the USA and the thought that further COVID restrictions will limit demand for ethanol as the US moves through winter kept a check on corn prices. Over the last week demand for both ethanol and petrol in the US have eased significantly. Wheat was mixed at the opening of the Chicago session, initially finding support from the weaker US dollar and falling US crop condition ratings. By the close the wheat market had copped a thrashing though. Punters happy to take some profit and square up prior to the long weekend. The combination of the Thanksgiving break, a looming first notice day in the Dec contract and even talk of increased Russian wheat exports had the punters heading for the door.

SovEcon upped the projected Russian wheat export number for 2020-21 1mt to 40.8mt. This is only 100kt below the previous annual record. In the same report Russian exports of barley and corn were reduced. The increase will obviously hinge on the government and whether or not they support the increase. Export quotas and export taxes have been used in the past to limit export demand depending on crop size. At the moment Russian consumers are canvassing the government for an export tax to help keep domestic wheat prices down. The stronger Ruble may also see export values out of the Black Sea slip a little.

Tunisia tendered for 75kt of optional origin durum for delivery between Dec 20th and Jan 25th. The tender also included 92kt of soft wheat and 75kt of feed barley. Soft wheat was bought at US$276CnF +/- a bit, no number on the durum yet, this will be important to know.