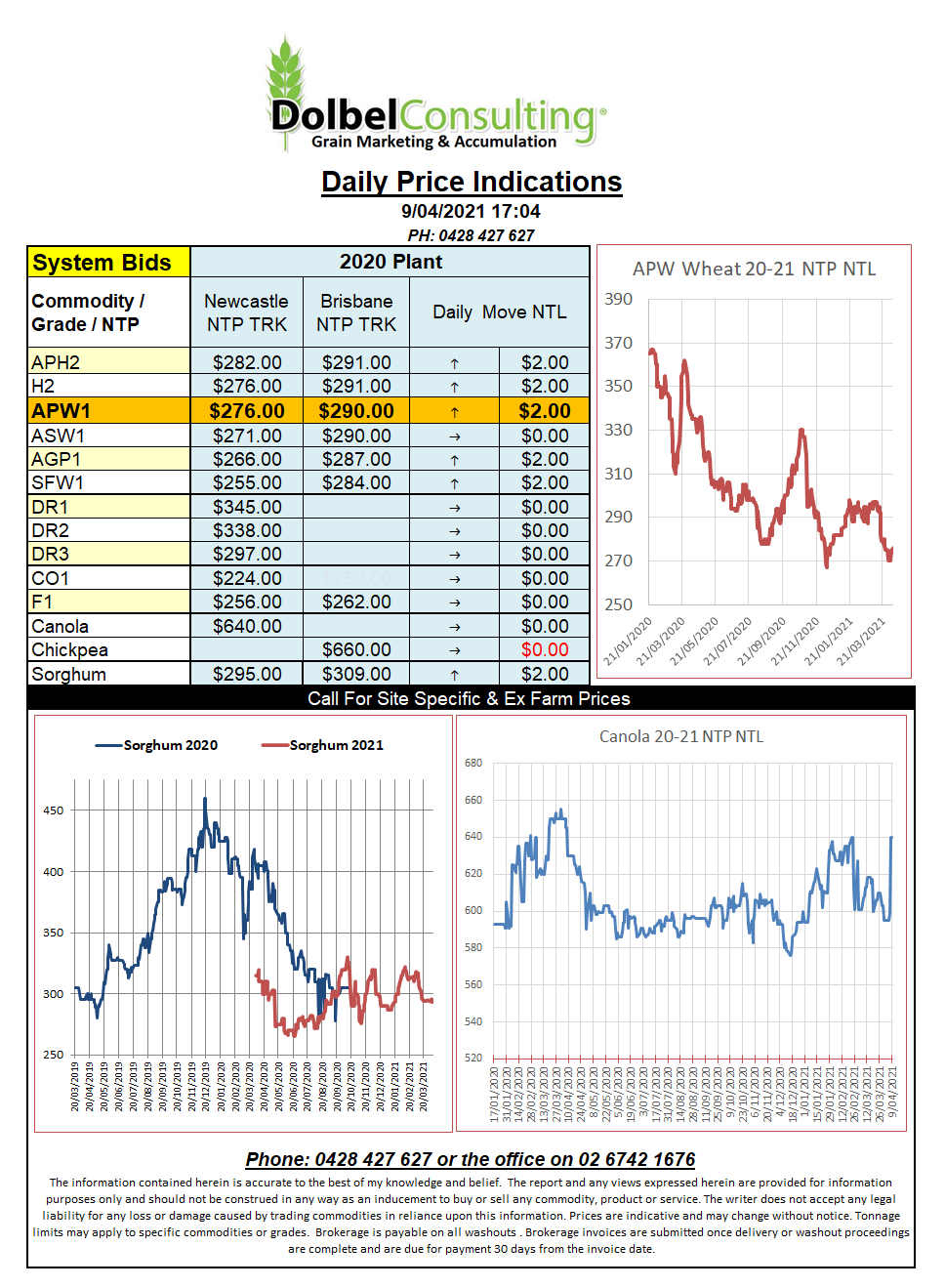

9/4/21 Prices

Looking through the raft of international business that has been reported this week one can’t help but think that many major consumers have taken advantage of the recent decline in wheat values.

Algeria started the week booking 30k of milling wheat at US$280 CFR. The product was purchased on an optional origin basis but most punters expect to see French wheat fill the contract. This purchase was around US$40 less than a previous purchase made in early March.

Thailand picked up about 58kt of option origin feed wheat on Thursday for June shipment at US$275 C&F. This would roughly equate to an ex farm LPP number of something close to AUD$255 – AUD$260. Yesterday SFW1 into the local market worked back to a price ex farm of roughly AUD$255 so bang on export parity.

Taiwan picked up 97kt of US milling wheat for May / June. Tunisia booked 75kt of milling wheat at US$260.71. Japan was also in for 91kt of Canadian and US wheat for a June slot, 66kt of US wheat and 25kt from Canada.

In the US futures markets wheat found support from good new crop sales volume, 529.9kt, with China leading the way with 260kt. Weekly export loadings were also on the high side at 634.2kt. Weekly corn sales were pegged at 757kt, down a little from both the 4 week average and last week’s volume. It does need to be noted that the prior week’s volumes were pretty big though. The punters were actively buying corn futures with expectations of lower stocks in tonight’s USDA WASDE report. Dry conditions in the US spring wheat belt helped wheat higher.