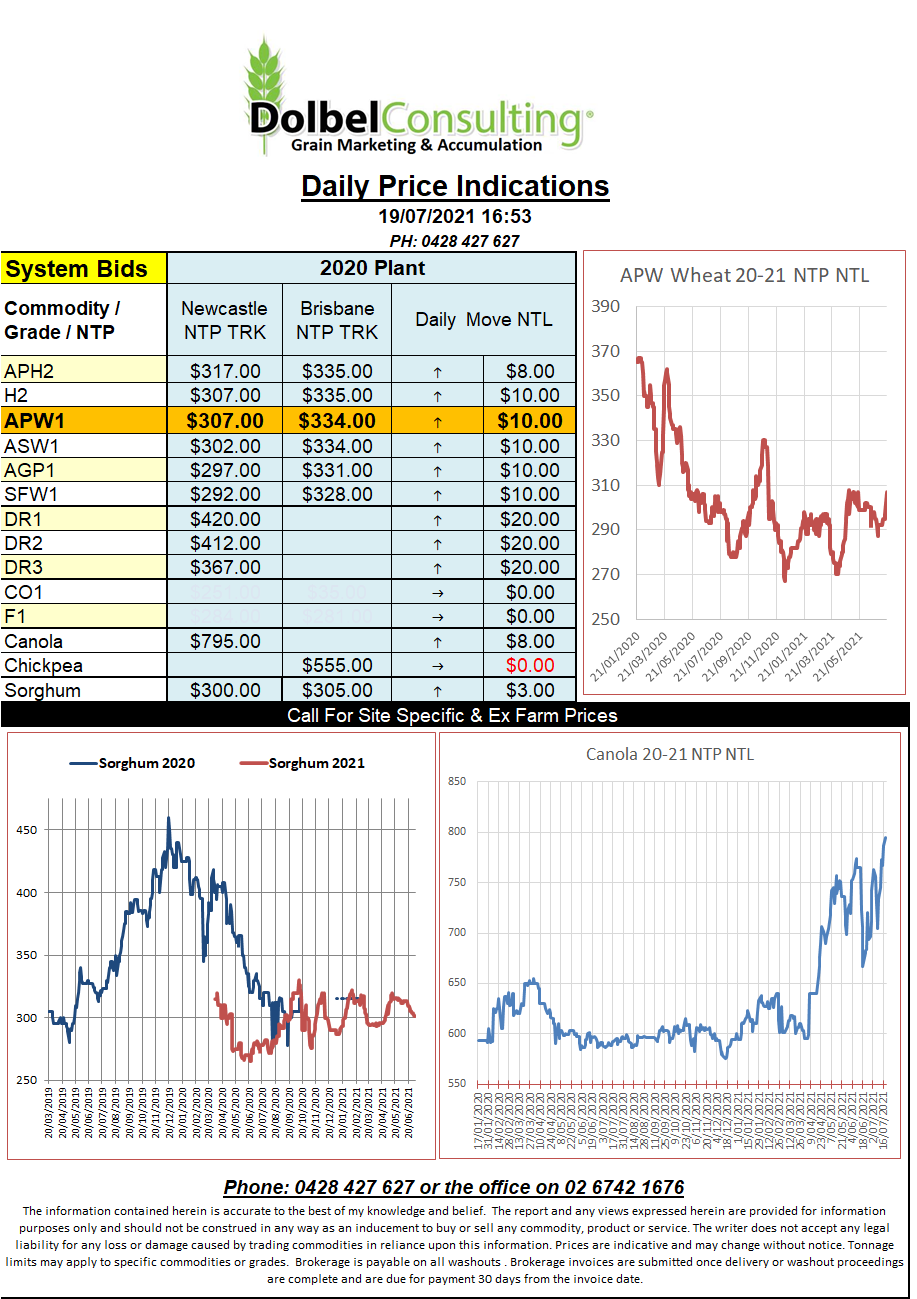

19/7/21 Prices

US wheat futures continue to rally as the punters are starting to realise that a 4 week dry spell in the spring wheat belt of the USA and the Canadian Prairies combined with some serious heat is about all they can handle.

The punters are starting to call the Canadian canola crop sub 16mt compared to last year’s crop of 18.7mt. Although not comparable to what we may call a drought here in Australia the N.American system is also not designed to be able to tolerate the variability we have here either. Thus a deviation from the average is often a major issue, as we saw in European wheat production a couple of years ago when yields slipped dramatically from over 6t/ha to as low as 4.5t/ha. So as bad as it sounds now there will be some spring wheat and there will be some canola come harvest time, so be aware of corrections during their harvest period.

Another important point is the ability to capitalise on any short fall in production, or export capacity, the N.American market may present.

It has become plainly obvious that in the east Aust states that this is more difficult to do than it sounds lately. Thank you China for stuffing the boat and container market and thankyou local unions for making that problem twice as bad as it should have been. This brings me back to basis. The cash prices we are seeing for canola in particular are good, very good, even with a ridiculously low basis. The question we need to ask is will the trade lift basis if execution becomes easier, and if it does, how much canola can the east coast export.

Canadian values followed spring wheat futures higher. 1CWRS13.5 was up C$10.76/t to C$365.79/t for a Dec21 lift. Durum was dragged higher as well with cash bids out of SE Sask at C$361.99/t for a Dec21 lift. Dec21 cash canola was steady to higher, bid C$877 XF SE Sask