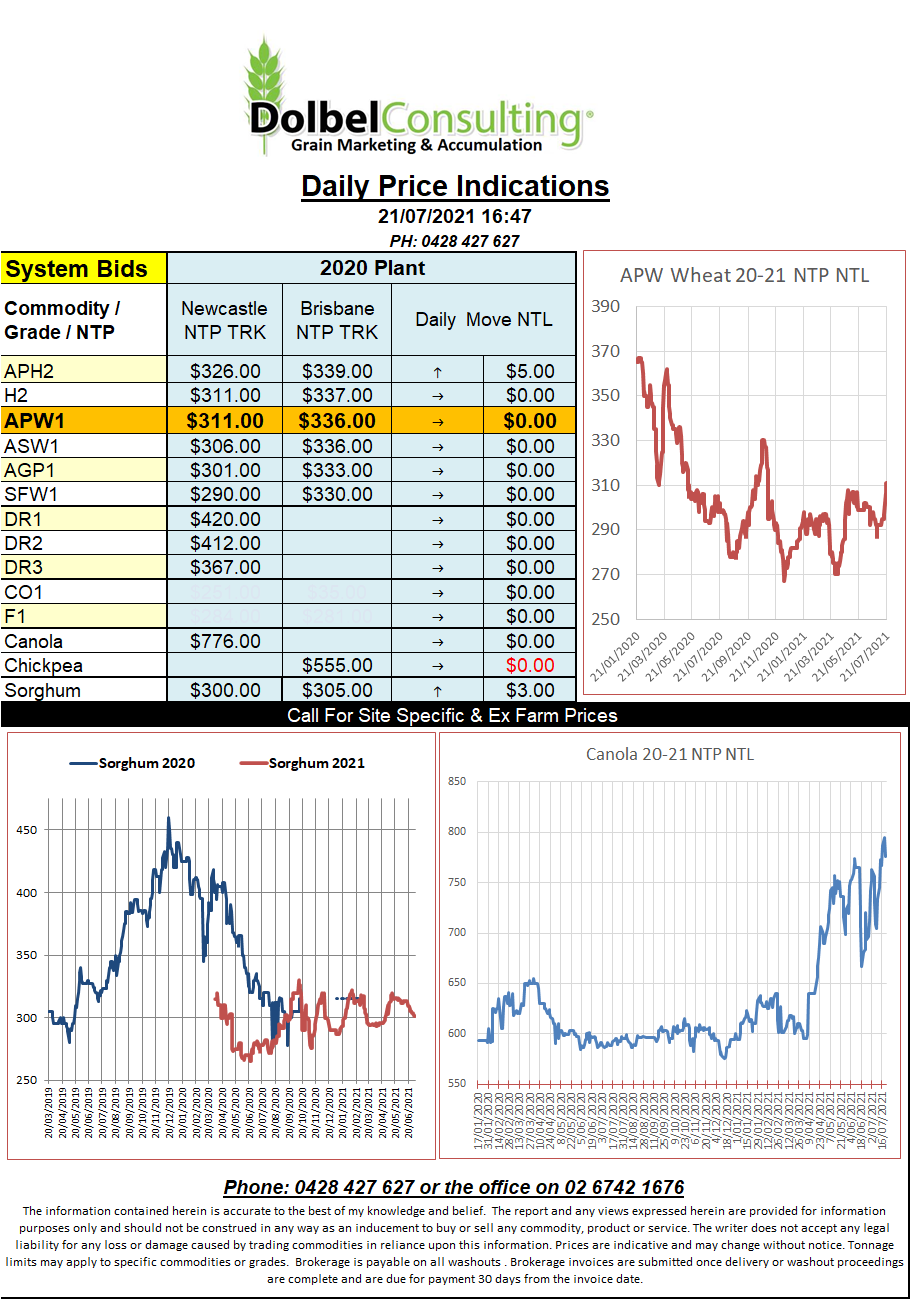

21/7/21 Prices

A quick glance at the December charts for corn and wheat at Chicago shows both contracts are relatively neutral at present. Wheat initially found some selling pressure early in the session which saw the bargain hunters in and support pushed the market back above the open before late session profit taking forced values lower again triggering more buying and a levelling out prior to the close.

Surprisingly spring wheat futures slipped lower. I say surprisingly because the G/E rating for US spring wheat fell much further in this week’s USDA crop progress report than what the punters were expecting. This may be indicating that the rally in spring wheat, for the time being, has ran its race and speculative money is now looking for something with a little more volatility as spring wheat values could flatten after pricing in the current problems.

One way to look at this is to determine what the US could buy in APH2 wheat for. At current values here, roughly $297 ex farm LPP, this could land in the PNW of the US for something close to US$360 – $370 +/- FOB depending on ocean rates and margins. Currently dark northern spring wheat out of the PNW is bid at about US$380 FOB for 13%. So this is indicating that in reality cash bids there are now very close to import parity and this could start to restrict the flow of export grain out of that region.

In SE Saskatchewan we see cash bids for 1CWAD13 durum ex farm rally sharply again to C$392.65 for a Dec21 lift, that’s a jump of C$16.28 per tonne. This is against the trend in 1CWRS13.5 milling wheat that actually shed C$4.53/tonne. 1CWAD13 to 1CWRS13.5 now +C$24.80.