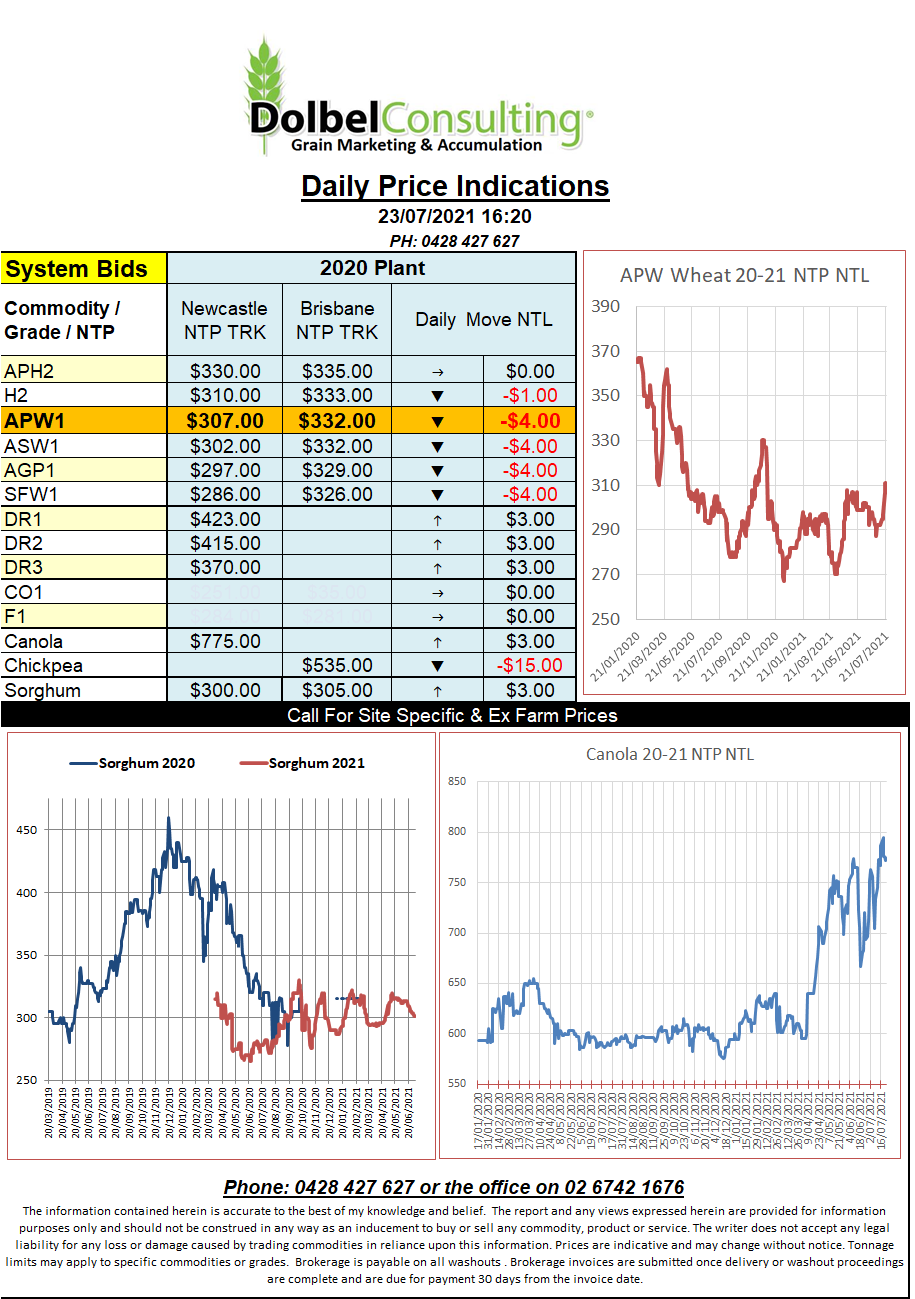

23/7/21 Prices

Chicago soft and hard red winter wheat futures were lower in overnight trade. Global fundamentals are unchanged with issues in spring wheat crops in the USA, Canada, Russia and harvest delays in the EU offering support. After closing higher for the previous six sessions a round of profit taking was in order and those sellers dominated the overnight trade.

Spring wheat futures at MGEX did manage to close higher, as did both cash and durum bids in SE Saskatchewan. 1CWRS13.5 Canadian spring wheat was up C$4.72 for a Dec21 lift with the average bid coming in at C$361.89 / tonne.

I’m not sure if the durum numbers on PDQ are correct as a C$47.24/t rally in Dec21 durum is huge. PDQ is a pricing website which accumulates and averages prices per region across the Canadian Prairies. It’s run by the Alberta Wheat Commission. Just say this durum price is right, which it may well could be given the issues in the Canadian durum belt. A price of C$450.29 ex farm SE Sask for 1CWAD13 would roughly equate to an equivalent Aussie port number of AUD$530 for DR1. Granted durum was probably overdue for some solid drought premium in Canada and the USA so it may take a little while to see this number reflected in global values, if at all or to 100%.

PDQ quotes a flat canola market overnight with the average Dec21 price XF SE Sask sitting at C$843.

With high temperatures hanging around the US spring wheat belt and the Canadian durum belt for another 14 days and little to no rain in the forecast the fat lady has stepped up to the microphone and is about to test the speakers. The next part of this equation will be reality, when headers start, we may still be 4 – 6 weeks away from that point.