2/8/21 Prices

In the US we see a little profit taking as July comes to an end. Benign weather for the bulk of the US corn and soybean crop and a slightly stronger US dollar sealed the deal and corn and soybean futures were sharply lower by the close.

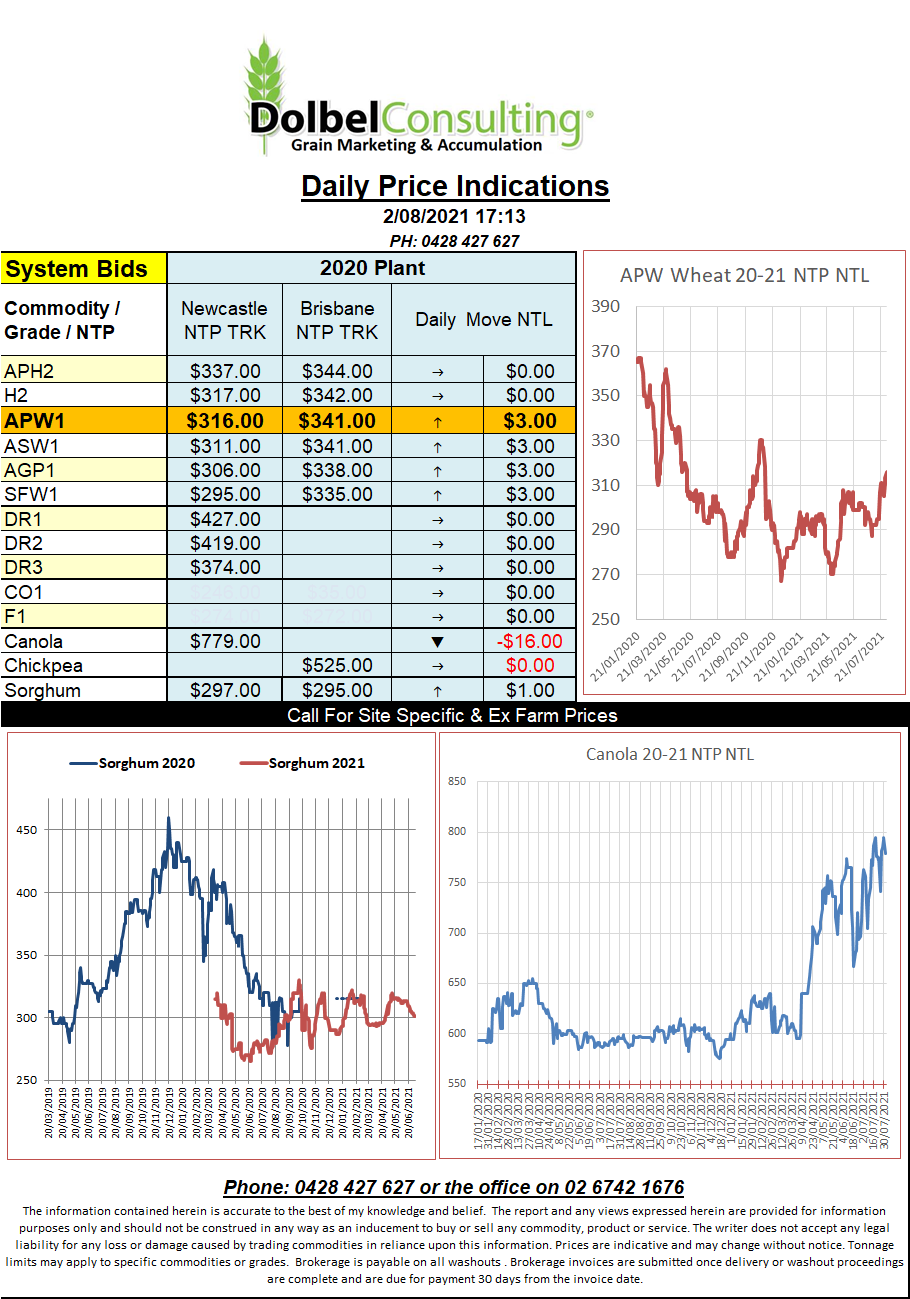

The weaker AUD should take care of any spill-over selling that pushed wheat futures in the US a little lower.

The softer close in soybeans rolled through to sharply lower canola futures at Winnipeg. Taking the lower AUD into account the move in ICE futures still equates to a plausible reduction of almost AUD$30/tonne. Looking at the PDQ cash bid summary across SE Saskatchewan we also see that the weaker canola futures were reflected in cash bids. No one is too keen to be on the wrong side of this monster at present. The average cash bid for a Dec21 lift out of SE Sask was C$816.75, down C$24.35 on the day, nearby bids were C$38 lower.

Still in Canada we see the 1CWAD13 durum price was firmer, bucking the trend in spring wheat. The average bid for a Dec21 lift now noted at C$464.58/t, up C$13.40 on the day. On the back of an envelope using basis to FOB of C$100 it would equate to a Newcastle DR1 price in the vicinity of AUD$570. Bids for French durum into Italy are not this strong. I’ll try and do a Canadian S&D sheet over the weekend to determine plausible export volume from Canada given the virtual failure of the N.American durum crops.

It would be interesting to know the demand requirements of durum for the US, Canada and Mexico and what volume this leaves for export. Bushel weight and grain size is likely to be a guestimate prior to harvest getting underway but lighter grain is also presenting analysts with a few issues when it comes to guessing yields. With lockdowns we did see a big increase in pasta consumption.