27/8/21 Prices

Technical buying pushed Chicago soft red winter wheat futures higher in overnight trade. The move higher appeared to have little new fundamental support apart from a slight reduction in EU wheat production number by the European Commission.

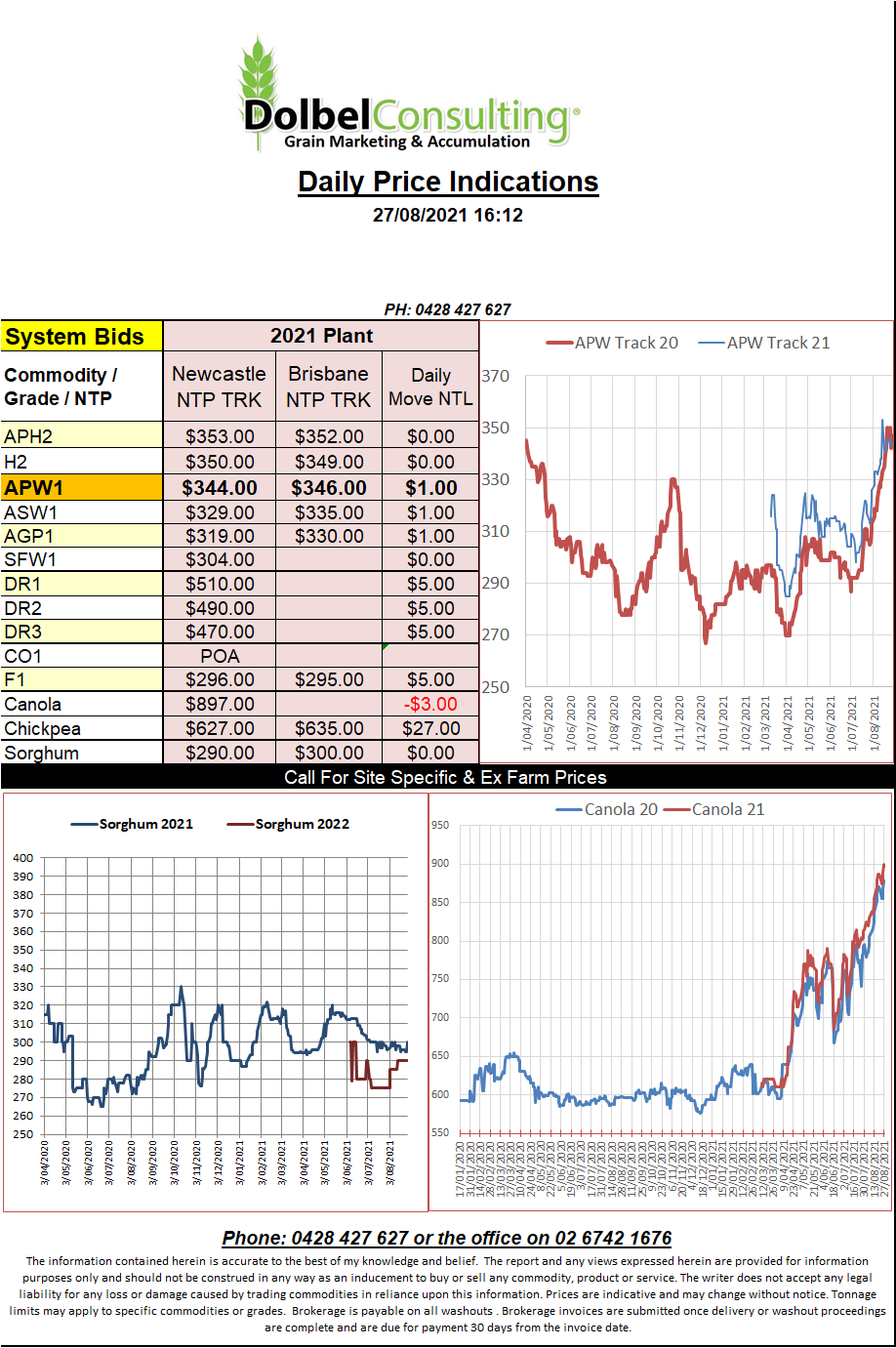

The results of the tender to buy wheat and barley by the Tunisia State Grain Agency are showing about 50kt of both were purchased on Thursday. The wheat parcel appears to be made up of two 25kt lots, one valued at US$349.89C&F and the other US$352.77 C&F. Using US$350 as a price point this would equate to an Aussie port number something close to AUD$355 equivalent. This does tend to indicate both APW and ASW could compete in this market at current new crop values if needed to.

The barley portion of the tender saw two parcels booked, one at US$319.50 C&F and the other at US$322.98. For the sake of the exercise let’s call this an average price of about US$321. This would compare to an Aussie port price of something like AUD$315. Currently we see bids into the port in WA at AUD$300 – $310 so in theory would also work. Both wheat and barley will most likely be supplied from the Black Sea or western Europe.

Russian spring wheat yields are slipping in the Volga Valley with some producers reporting yields down under a tonne to the hectare. The trend is set to continue across the entire Russian and Kazakhstan spring wheat region. Many saw seeing less than 20% of their average rainfall over the last 30 days. 90 days totals across Kazakhstan spring wheat regions are as low as 25 – 75mm.