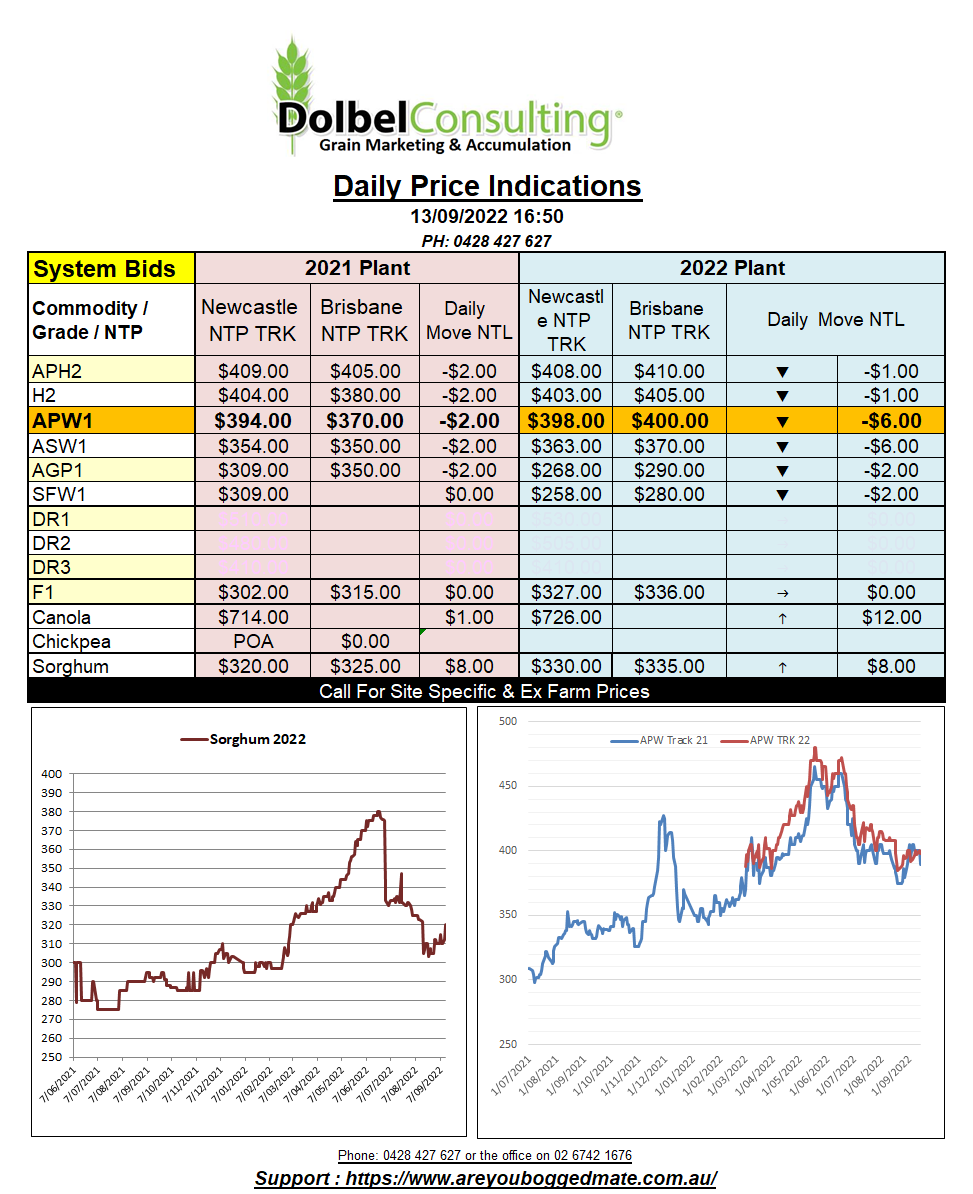

13/9/22 Prices

Another month, another USDA World Ag Supply and Demand report. Firstly, the boring stuff, the wheat market, generally the report appears a little bearish wheat if anything. Global production is a smidge higher, up 4.32mt to 783.92mt. Beginning stocks were reduced a little and consumptions was increased a little, the net result being a 1.23mt increase in world ending stocks. So not overly bearish, just not really a report to stoke a fire under wheat prices, which now appear to be priced fairly into the world market.

Argentine, Canadian, and Australian production numbers were all left unchanged, Aussie carry in increased a smidge, rolling straight through to a higher carry out of 3.15mt, a number still well below where it is an issue. EU carry in and consumptions were adjusted, a lower carry out the net result. A realistic production number is now against the Russian wheat crop, 91mt. Russian carry in was lowered 1mt, consumption and exports increased but still the net result was an increase of 1mt to Russian carry out, now estimated at 15.39mt. Chinese numbers were left unchanged as were Indian wheat numbers. India, China, and Russia will carry out between them 171.28mt of the 268.57mt of wheat expected to be carried over. That’s 63.77% of world ending stocks in the silo of a major exporter, a net importer and India who just banned wheat exports. Not exactly bearish wheat either is it.

Corn and soybeans were the big winners last night. World corn production back 7.03mt and world carry out back 2.13mt. US corn yields were reduced from last month’s report by 0.182t/ha, that may not sound like a lot, but the net result is a reduction in US production of 10.54mt. The downside is the higher prices are expected to reduce domestic demand in the US for food, feed, and some industrial uses. US corn exports were also expected to decline by 2.54mt. Still the net result is a fall of 4.29mt in US ending stocks. Leaving a US stocks to use ratio of just 8.5%.