6/3/23 Prices

Russia continues to rattle their sabre regarding the extension of the Grain Corridor deal. If anything, this ordeal has taught me how to spell corridor.

Russia continues to export significant volumes of grain through the Black Sea while increasing their export tax to ensure domestic prices remain stable and stocks at the domestic level remains adequate, while at the same time expressing that the sanctions are limiting exports of grain through the Black Sea. This claim is false, Russian wheat exports are set to break their export volume record this year. This isn’t a bad thing, the fewer tonnes of Russian wheat left in the silo come the end of the year the better. The last thing we need to see is big Black Sea carry in.

Ukraine have confirmed that their wheat crop will be sharply smaller than previous years, no explanation is needed to back this statement.

Joining the list of those countries expected to produce less wheat in 2023-24 is Australia. This week projection for the new crop came out at 25 – 26mt, an “average” sized crop. The current weather conditions will need to turn significantly in order to sow the area needed to realise even this estimate.

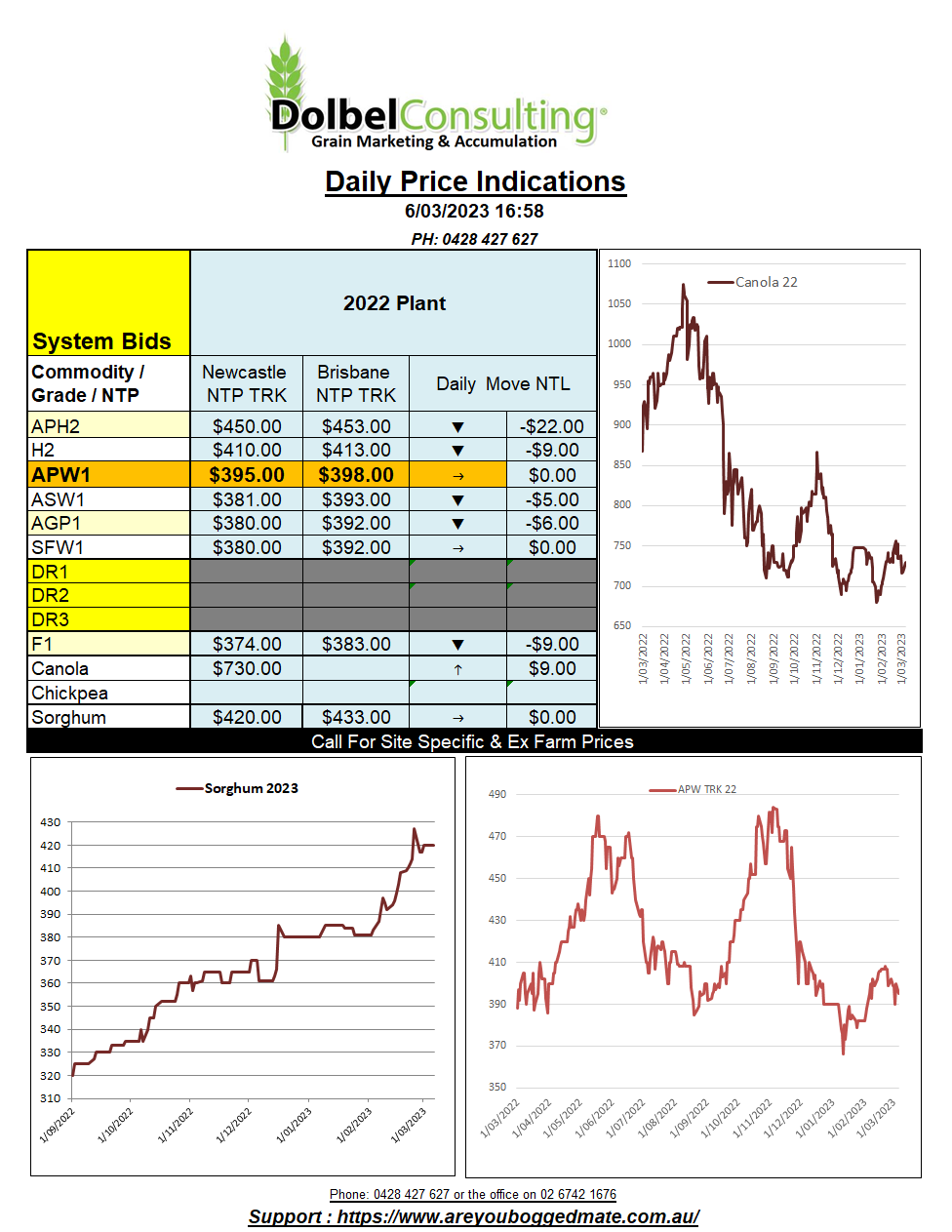

The dry weather across eastern Australia has also taken its toll on summer crop production. The national sorghum crop now estimated between 1.6 and 1.7mt, a deviation of at least 35% to the 5-year average. Those international buyers looking for Australian sorghum may find the silo’s run dry earlier in the export year than they traditionally do. Current export orders for sorghum are estimated to be running at roughly 700kt.

Northern France and Germany are expected to see some showers this week, Germany potentially receiving 25 – 50mm while France could see this towards the north, the greater area is expected to see just 10 – 20mm. The southern durum region towards the lighter end of forecast.