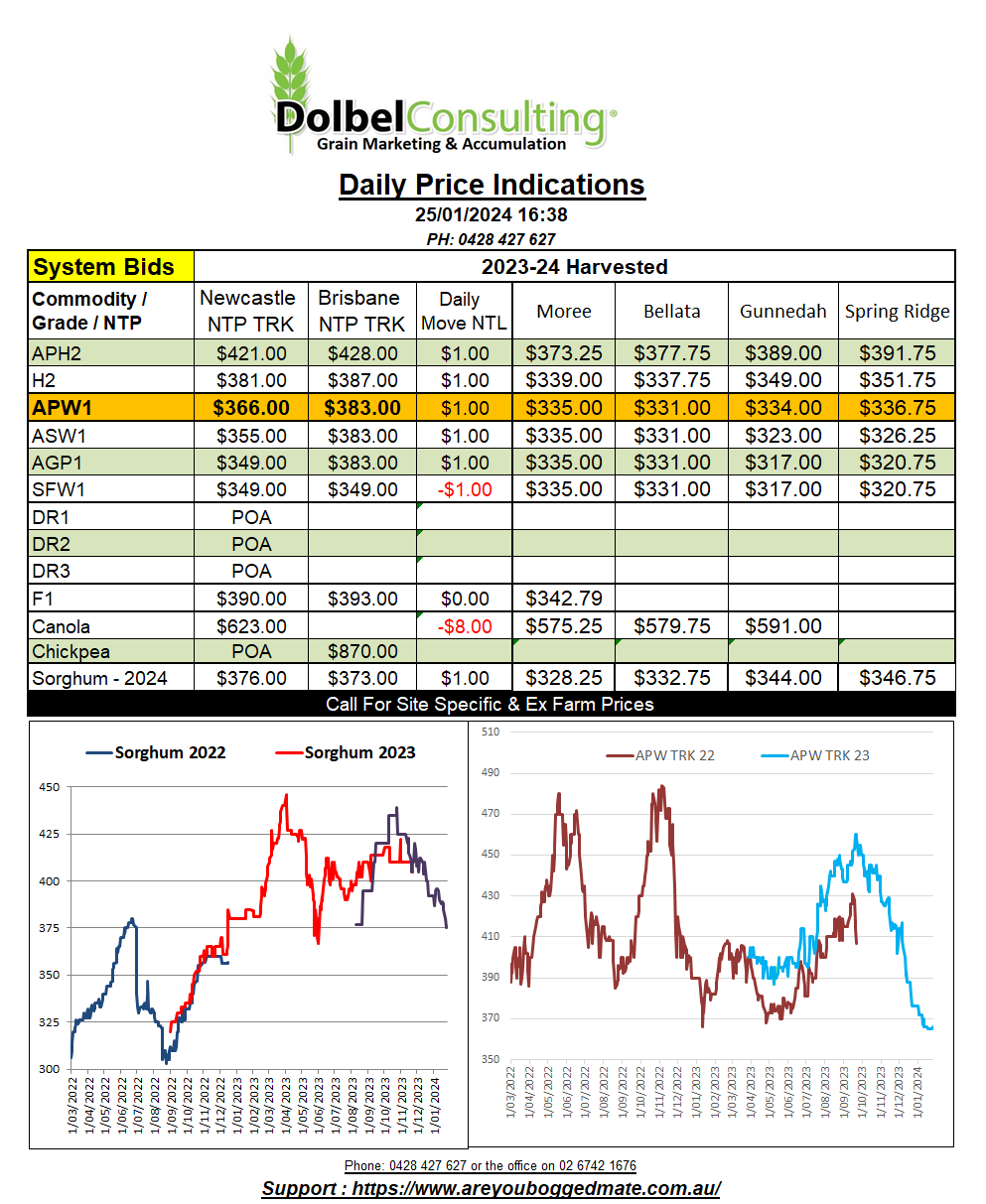

25/1/24 Prices

US wheat futures grabbed a few more cents per bushel from the open. Warmer temperatures across the US plains will be welcome after the last week or two where many locations experienced blizzards. The possibility of unseasonably warm weather across parts of the US Midwest may also see a significant amount of snow cover lost in places.

Technically we now see nearby SRWW futures at Chicago back to trading above the 100 day moving average. Some analyst suggest further upside, potentially, as high as the mid 600c/bu range prior to the March contract expiring. It’s hard to back up that assumption without seeing a significant uptick in global demand.

The reversal of recent gains in canola and rapeseed futures wasn’t as good to watch as the higher close in wheat. Paris shed E2.75 on the nearby rapeseed contract while ICE canola futures were C$4.80 lower on the nearby. Chicago soybeans were mixed, closing either side of unchanged.

The crush pace of canola in Canada for December was reported at 943.3kt, that’s up on the previous month and also higher than during December 2022. Better still it is above the volume needed to achieve the Agri-Food Canada projections of 10.5mtpa. This data may prevent further sharp losses in ICE canola, but gains may also be capped by the large soybean crop in S.America. This market is starting to look very range bound.

Durum values across Italy have failed to sustain the rally. Week on week bids out of the major mills were unchanged. This tends to support what we are seeing for cash values out of both Canada and France, both countries values remaining flat this week with variations on price more a function of currency than end user values. In Canada we see nearby values priced higher than April by C$6.50/t, new crop (Sept24) priced C$58.26 lower than nearby.