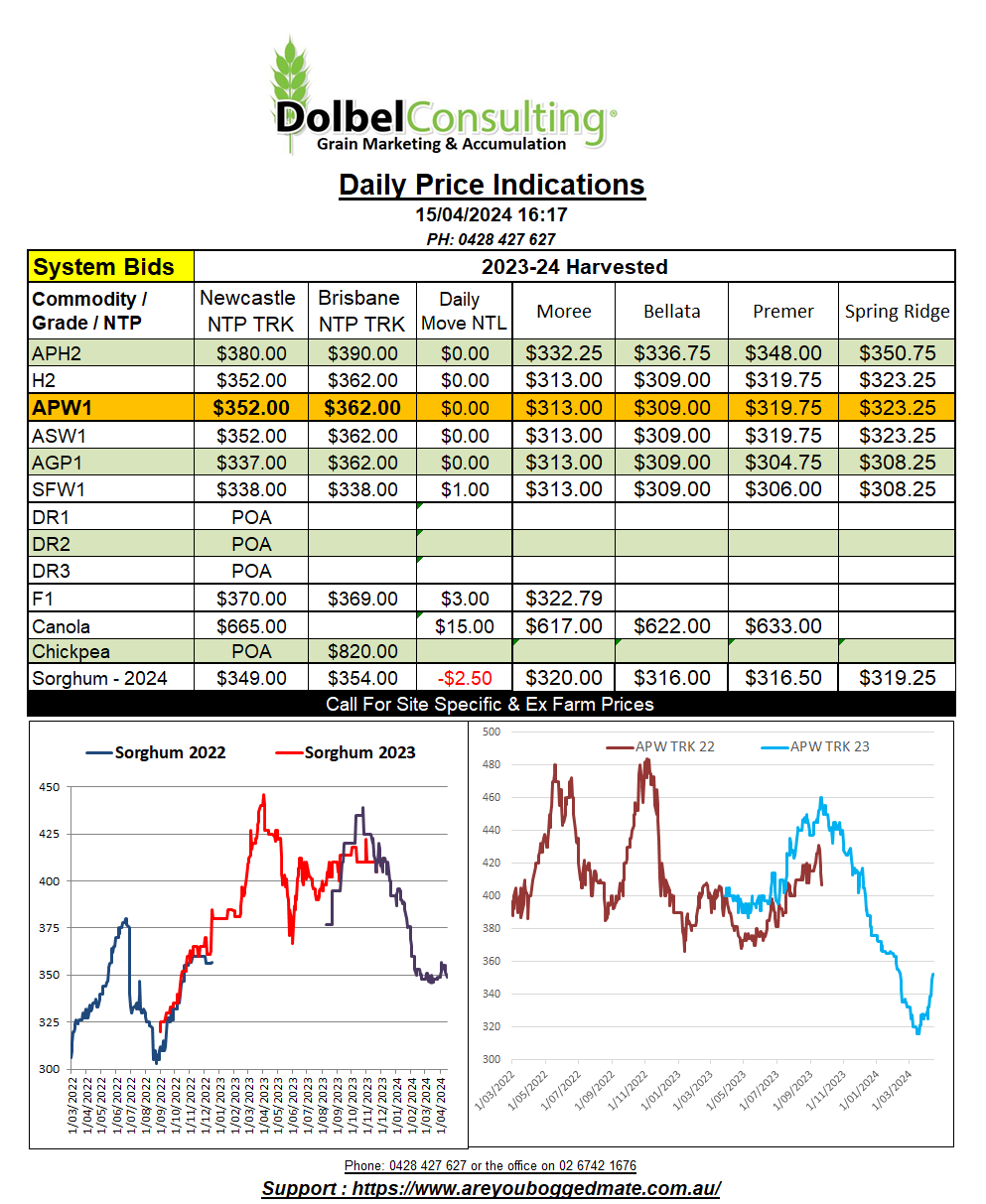

15/4/24 Prices

It was a tug of war in corn and soybean futures this week. CONAB and the USDA providing the muscles to move the Chicago futures markets, adding some volatility and thankfully some upside to the market fueling a recovery on Friday.

Lower corn and soybean production in S.America was the key to the recovery. The USDA cut Argie corn 1mt on Thursday, now pegged at 55mt. This is still well above the Rosario Exchanges estimate of 50.5mt. The big discrepancies between the two lie in the Brazilian estimates though. USDA corn there at 124mt versus CONAB at 110.96mt. The difference between USDA and CONAB estimates for S.American corn now lie at 18.5mt, that’s a lot when you consider it’s equivalent to 35% of projected US corn exports.

The soybean numbers for S.America from both CONAB and the USDA also vary greatly. Brazilian soybean production, although sharply lower than early season estimates, is not as low as it could have been. At 146.5mt (CONAB) it is below the USDA estimate of 155mt, but it could have been much worse after dry weather punned production in Brazil’s top bean state Mato Grosso. A better season in the south saw Rio Grande do Sul increase production by over 70% to stop Brazilian losses from being much more.

The lower soybean estimates from CONAB seemed to carry some weight in the markets, even though hitting the screens just a day after the monthly USDA WASDE report, the market definitely took notice of the reduction in estimates.

The spillover was a kick in values for Chicago soybean futures, that strength spilling over to both Winnipeg canola and Paris rapeseed futures.

Both canola and rapeseed are also seeing some fundamental strength from local weather conditions in France and Canada. Canada is probably a little dry, but that is expected to change next week.

France, and much of Europe, is still a little wet, not as wet as it was. I’m not convinced this won’t help Europe though, condition ratings were flat week on week.