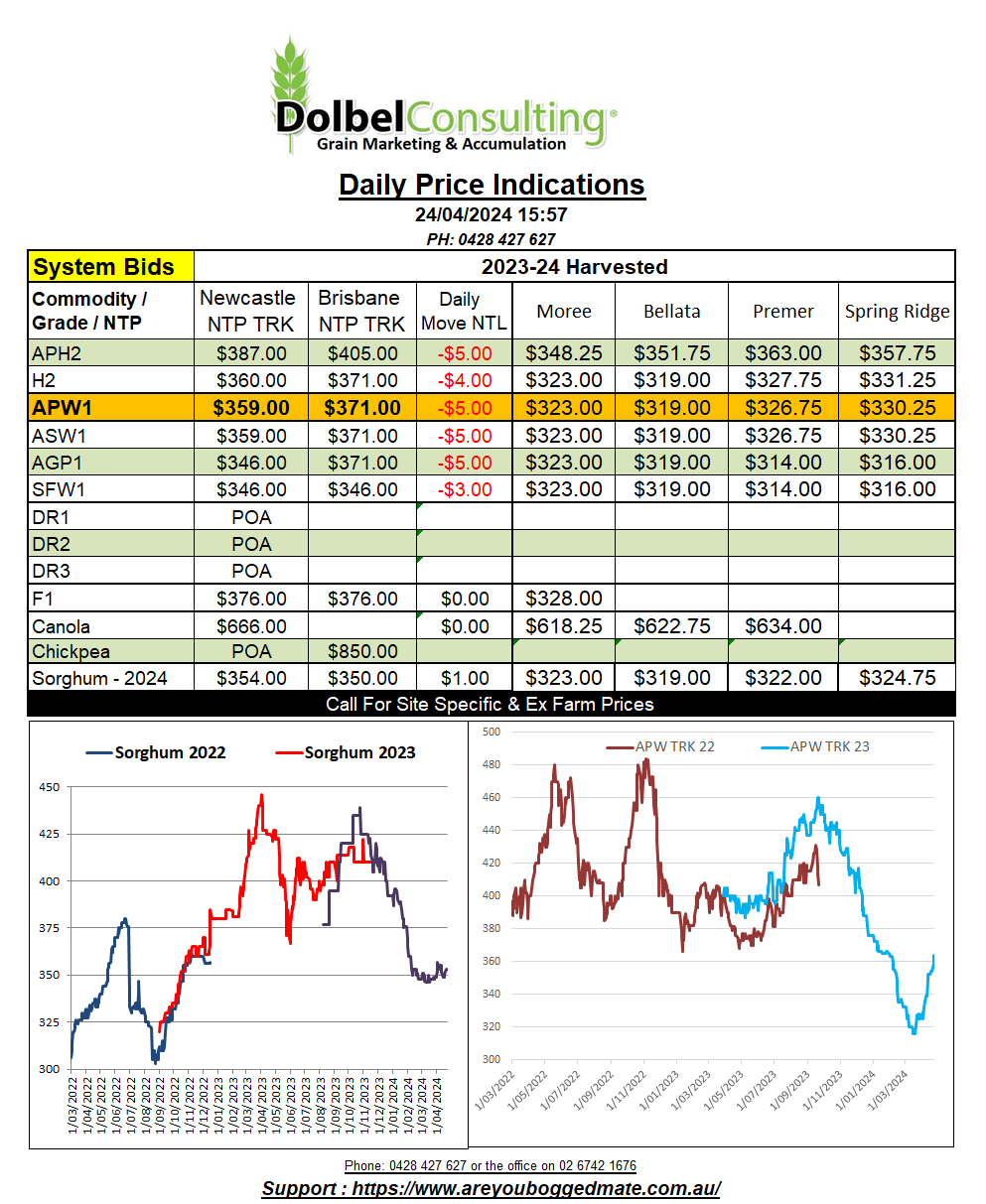

24/4/24 Prices

US sorghum export sales saw a net reduction of 1,800 tonnes for the week ending April 11th. A significant reduction week on week and also compared to the 4 week average. The US sold 8kt to Mexico, but China had cancellations of 9.8kt for the week. Net US sorghum exports were down 47% week on week at 76.2kt, the entire export program was destined for China.

Around 17% of the new season US sorghum crop has been sown, this is comparable to the average for this time of year of 18%. The majority of the sowing activity has taken place in Texas where roughly 60% of the sorghum crop is now in the ground. Kansas has sown just 1%, not unusual for this time of year while Oklahoma is yet to strike a blow.

US wheat saw another round of technical buying, short covering, supporting Chicago and MGEX wheat futures. There were also significant improvement in white wheat cash values out of the Pacific Northwest. Even when taking the stronger AUD into account, club white wheat managed gains of over AUD$14.00/t.

Managed money are said to have reduced their net short in wheat futures significantly this week. Keep an eye on Friday night’s CFTC report for confirmation. Keep in mind funds went into this week with almost a record combined net short position in US grain futures.

Paris milling wheat futures were having none of it, nearby May futures closing E6.00 lower. The outer months were not as beat up, Dec24 shedding just E0.25 by the close, other months were generally flat to +/- E0.25.

In AUD terms, Black Sea wheat values were sharply higher, even considering the AUD strength. Concerns about weather across Russian winter wheat districts was somewhat countered by better conditions and good sowing progress in spring wheat districts.

Declining crop condition ratings in the US, and potentially Russia, should continue to put pressure on the funds to reduce their net short in wheat.