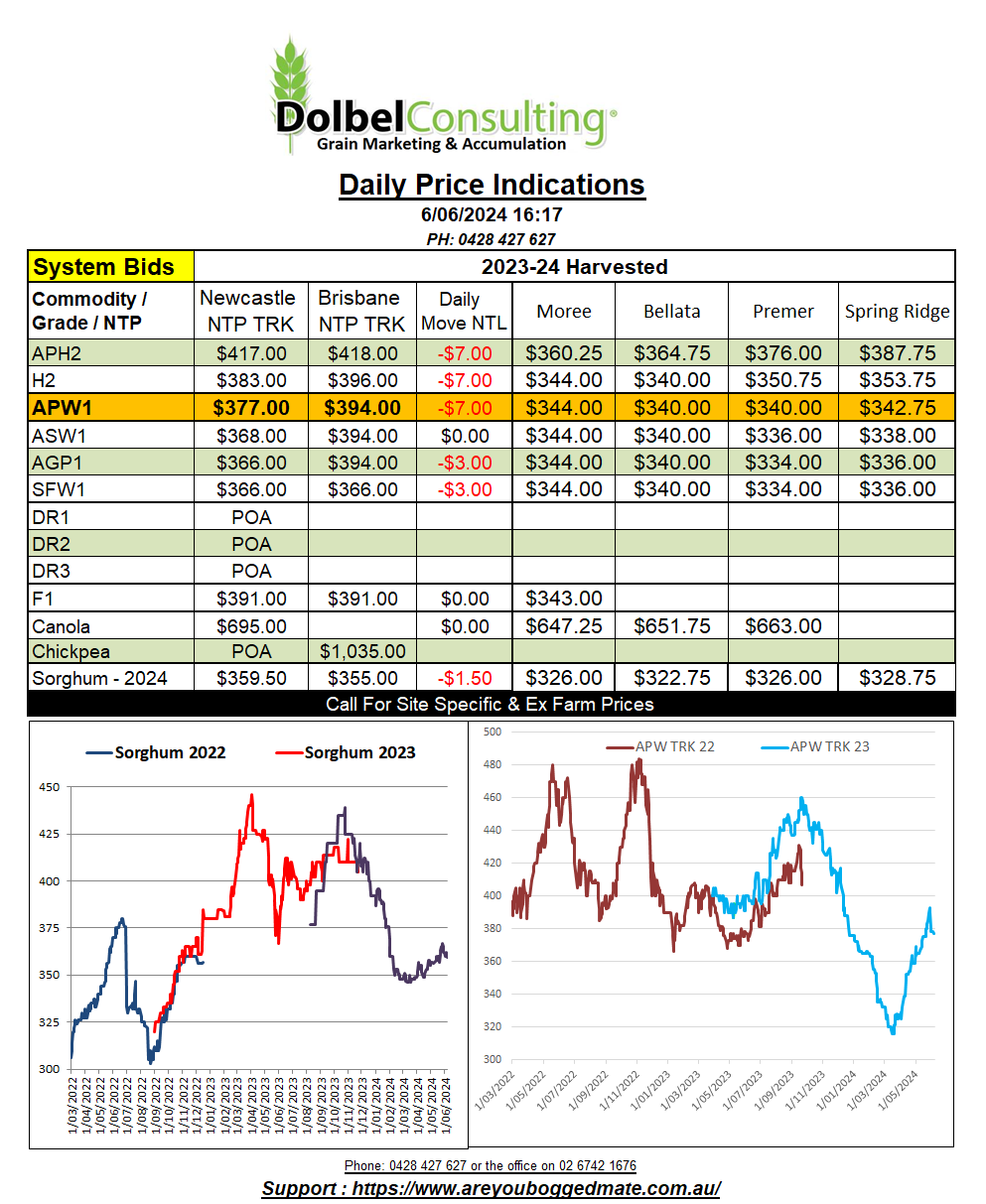

6/6/24 Prices

Algeria was said to have picked up 840kt of mostly EU milling wheat for August. Values are speculated, as is tonnage, as Algeria do not make public their purchase details. Current trade guesstimates on value appear to be around US$279. This price does seem to be pretty low, well below any values the Aussie market could have shown at a CiF level that’s for sure. In comparison to current French values it also looks cheap, to the tune of US$25 under. It is roughly comparable to recent Russian business though. US HRWW won’t work, it’s US$30 more than French wheat CiF basis Algeria. If this is EU wheat making it’s way there it may well be signalling a softer market for EU wheat than we are currently seeing.

US wheat futures continued to push lower, realigning US values with world values after weeks of US increases. The recent sharp decline in US wheat values has brought US wheat back into competition into the Asian market. HRWW now again competitive with Aussie wheat on a grade to grade basis with no additional premium apparent for Australian white wheat v red wheat. Russian, Ukraine, US HRWW and Aussie H2 all appear to be converging to around a similar number landed Asian buyer at present.

Old crop durum values in Italy fell away by five euros on Tuesday. New crop harvest is slow to start, but still earlier than usual due to a dry finish to the season and now showers delay progress. Values FOB France were also a little lower, not a lot, roughly equivalent to about AUD$1.34 softer.

Along with Turkey, Russia is also increasing durum area. Recent media from Russia confirms their intention to continue to increase sown area of hard wheat by 30% more than this year, which could be as high as 1mha in 2024. The EU has put huge import tariffs on Russian wheat, including durum, which may stifle export flow somewhat in the mid term.