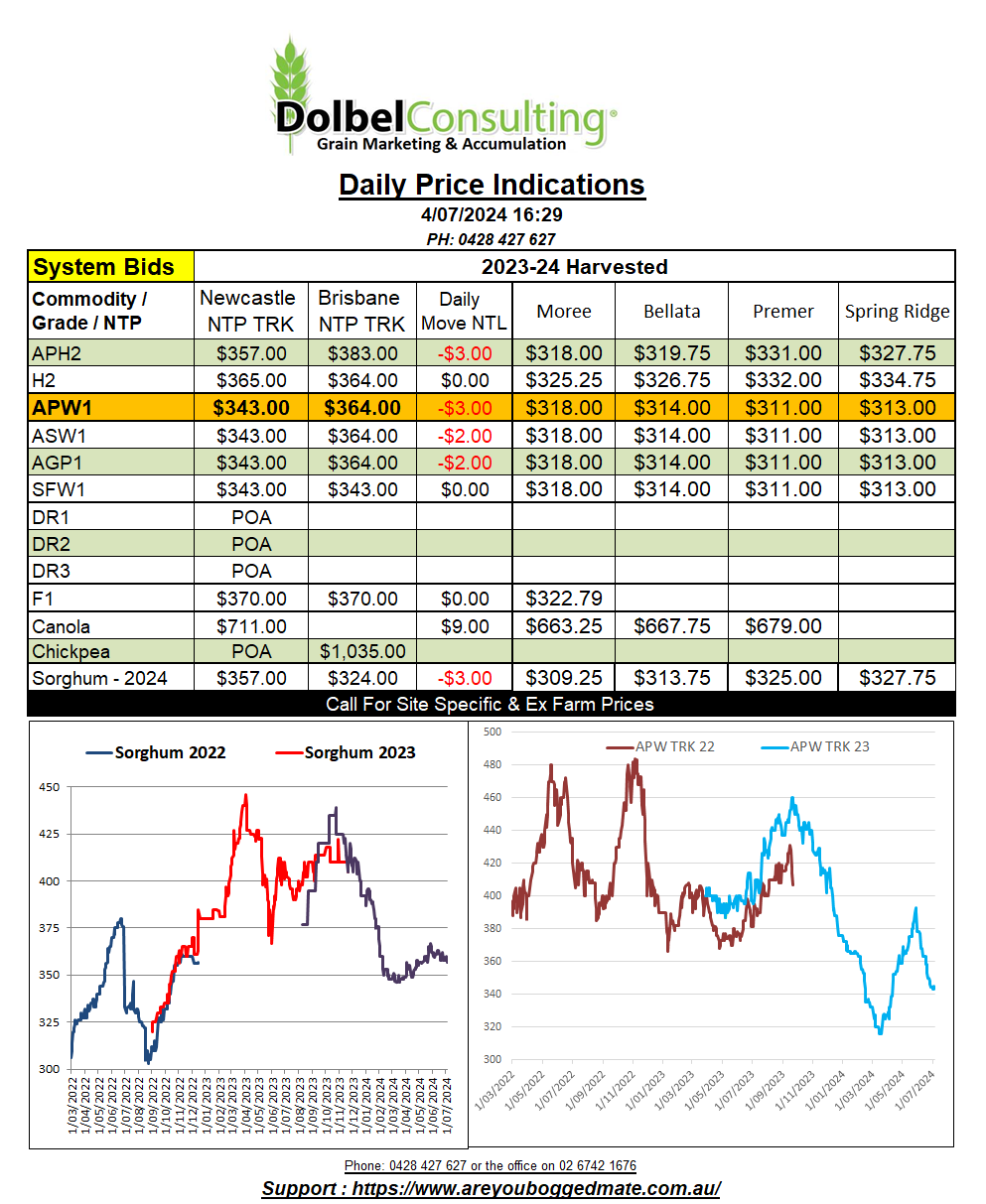

4/7/24 Prices

Paris rapeseed futures were again the clear winner in overnight sessions. The Feb 2025 slot closed €7.25 higher at €510.75 / tonne. Chicago beans were a little higher by the close, up 9c/bu (AUD$4.93/t). Strength in both US soybeans and Paris rapeseed pulled the Winnipeg canola contract higher, the Jan25 slot there gaining C$4.10 (AUD$4.48) by the close.

Paris milling wheat futures closed lower, the Dec24 slot back €4.25 /tonne. Chicago SRWW and HRWW contracts and the Minneapolis spring wheat market also closed lower. Values for US red wheat out of the Pacific Northwest were lower, hard red winter wheat shedding the equivalent of AUD$7.08 per tonne day to day when taking the stronger AUD into account. The day to day difference in spring wheat values was less, roughly -AUD$6.75 / tonne, white wheat values were stable.

On the back of an envelope US wheat values out of the PNW into the Asian market remain very competitive against Aussie wheat. US club white wheat is considerably less that current bids for APW1 off the east coast of Australia. Currently this is putting little pressure on local east coast Australia consumer bids though, as old crop stocks across E Aust are relatively tight. Wheat out of WA into the Chinese market remains very competitive with all the major Asian suppliers and is up to AUD$20 lower than most ports of origin.

Chickpea values at the Delhi market saw some significant downside last night. In AUD/tonne the move was equivalent to roughly AUD$20.96 when taking the move in Rs/Q and the stronger AUD into account. This takes week on week losses at the Delhi market to roughly AUD$32.75 / tonne.

With the Aussie economy basically falling apart the talk of higher interest rates appears to be getting hosed down. Talking to reps that pass through the shop they have told me that clients in larger stores in the city have noted retail sales back between 40% and 60% year on year, that’s fire sale territory for many.