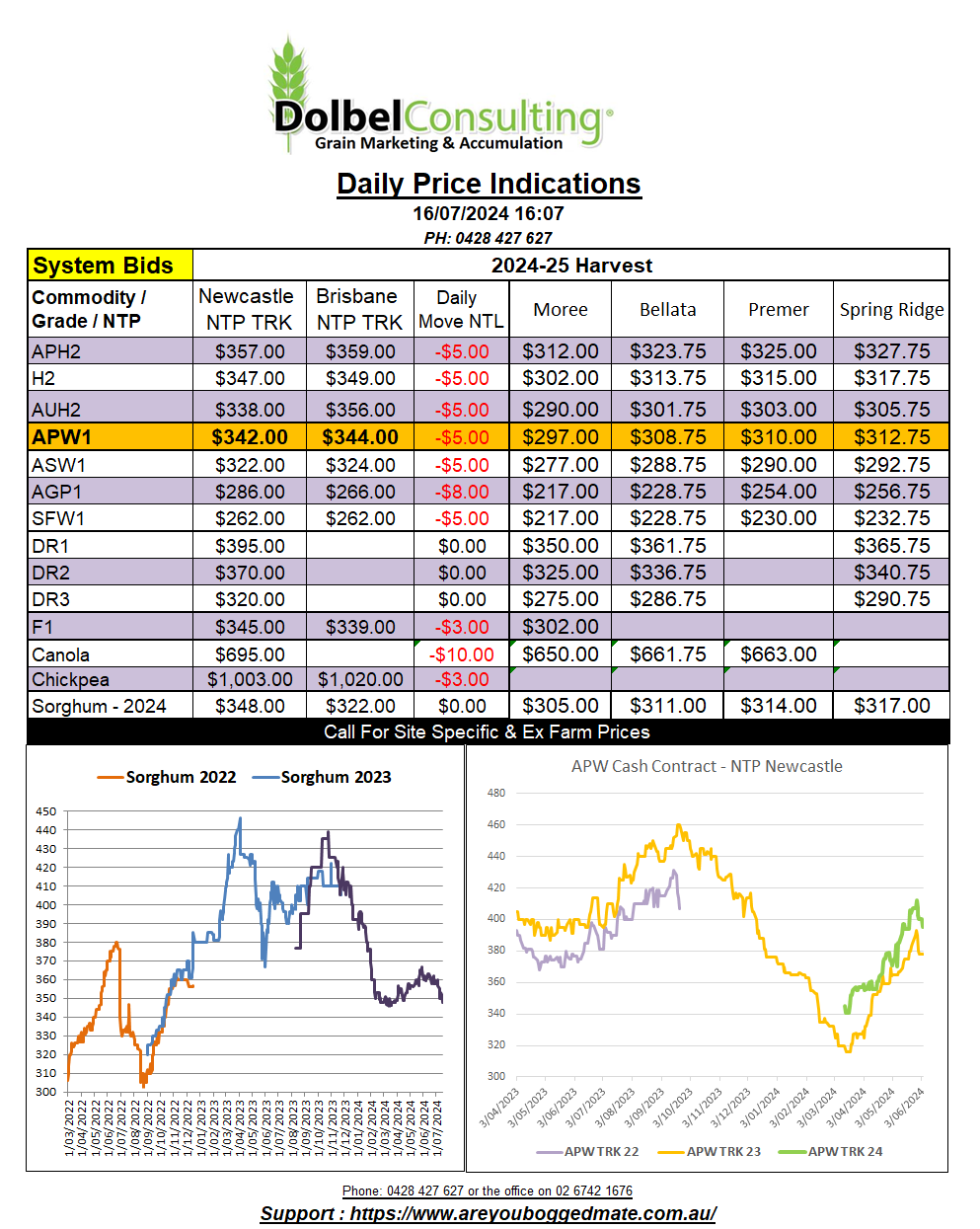

16/7/24 Prices

It was a sea of red out there in the futures markets last night. One can only assume the funds were happy to extend their now record short position in many commodities.

The weakness wasn’t restricted to just the synthetic market, cash prices out of the US Pacific Northwest also pushed lower. Making US wheat values even more competitive into the Asian markets.

White wheat out of the PNW fell AUD$9.69 compared to the last value seen there Friday. This is comparable to an XF LPP price of something close to AUD$270. This may make current new crop bids here look a lot better than they do on a new crop gross margin spreadsheet. The weakness wasn’t restricted to WW, both US and Canadian spring wheat values were also sharply lower. Canadian 13.5% spring wheat out of the PNW shed AUD$8.09 in value while US DNS was back around AUD$7.95 compared to the previous days values.

Paris milling wheat futures were not immune to the selling, the Dec24 slot there closing at €221.75, down €6.50 per tonne.

The bad news doesn’t stop at wheat though, continue on if you don’t mind watching a skid bin fire, mmm warm. Canola and rapeseed futures were also pushed lower. Paris leading the way, the Feb25 slot closing at €475.75, a fall of €8.00 per tonne. If you take day to day variations in the AUD/Euro into account the decline in AUD terms is closer to AUD$10.89 per tonne. Winnipeg canola futures were a little more subdued but did close roughly AUD$4.11 lower.

Barley you ask, FOB French values were roughly down AUD$8.00 per tonne compared to late last week.

And chickpeas, we’re all in trouble when we think chickpeas will save the day. Delhi market values were back 64Rs/Q, in AUD per tonne, taking the move in the AUD/Rs into account, that is roughly AUD$8.40 per tonne lower. Not a great start to the week. What will put the brakes on this fund fueled madness you ask, will the bottom feeders come out in force, will the possibility of lower supply from the major exporters be noticed, not according to Friday’s WASDE & CFTC.