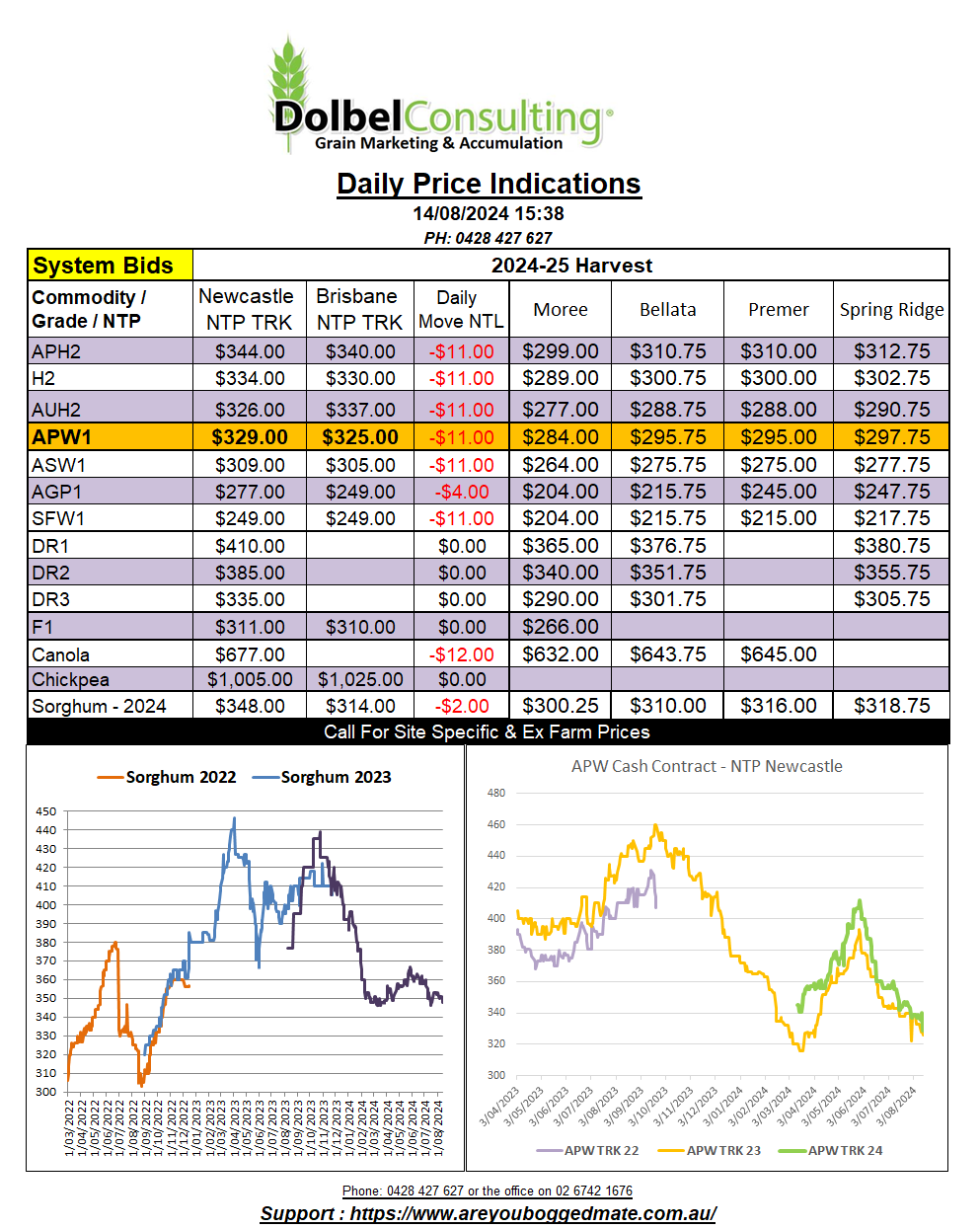

14/8/24 Prices

It’s a sea of red out there this morning. International futures markets are generally lower. London feed wheat is lower, Paris milling wheat lower, Chicago SRWW and HRWW futures are both lower, corn and soybean futures at Chicago also lower, beans sharply so and dragging canola and rapeseed with it.

Paris rapeseed was back €6.25 in the Feb25 slot, Winnipeg canola was back C$17.90 in the Jan 25 slot.

Cash bids for ex farm canola out of SE Saskatchewan were also sharply lower. The Dec pickup window followed futures lower by C$17.90. Cash spring wheat and cash durum ex farm SE Sask were generally flat though. 1CWAD13.5 durum wheat was bid on average C$245.64 / tonne for an Oct lift. The spread between CWAD1 13% durum and CWAD1 11.5% durum XF SE Sask is narrow at just -C$3.31, even 2CWAD 11.5% is just -C$8.45 under.

Conditions in the Russian and Kazak spring wheat region is wet and should remain wet in the short term. This isn’t great news for the growers there as harvest is just around the corner and the wet weather is expected to reduce the quality of their wheat. It had generally been very soft season in that area. This region produces durum and hard wheat for milling usually, but this year analyst are expecting to see more feed wheat. This could take any further downward pressure of durum values into N.Africa in the short to mid term. Still no news on the Algerian durum tender, should see some info tonight or tomorrow morning.

The 3.8mt Egyptian tender appears to have been a bit of fizzer. Reports show just 280kt being booked from Ukraine and Bulgaria. Values were around US$266.21 CFR. On the back of an envelope that’s roughly equivalent to AUD$290 XF LPP. Current new crop bids for H2 delivered Graincorp Gunnedah are AUD$313. That’s basically says our wheat competitive with Black Sea wheat into N.Africa, Aussie wheat hasn’t been that cheap for a long time.