23/8/24 Prices

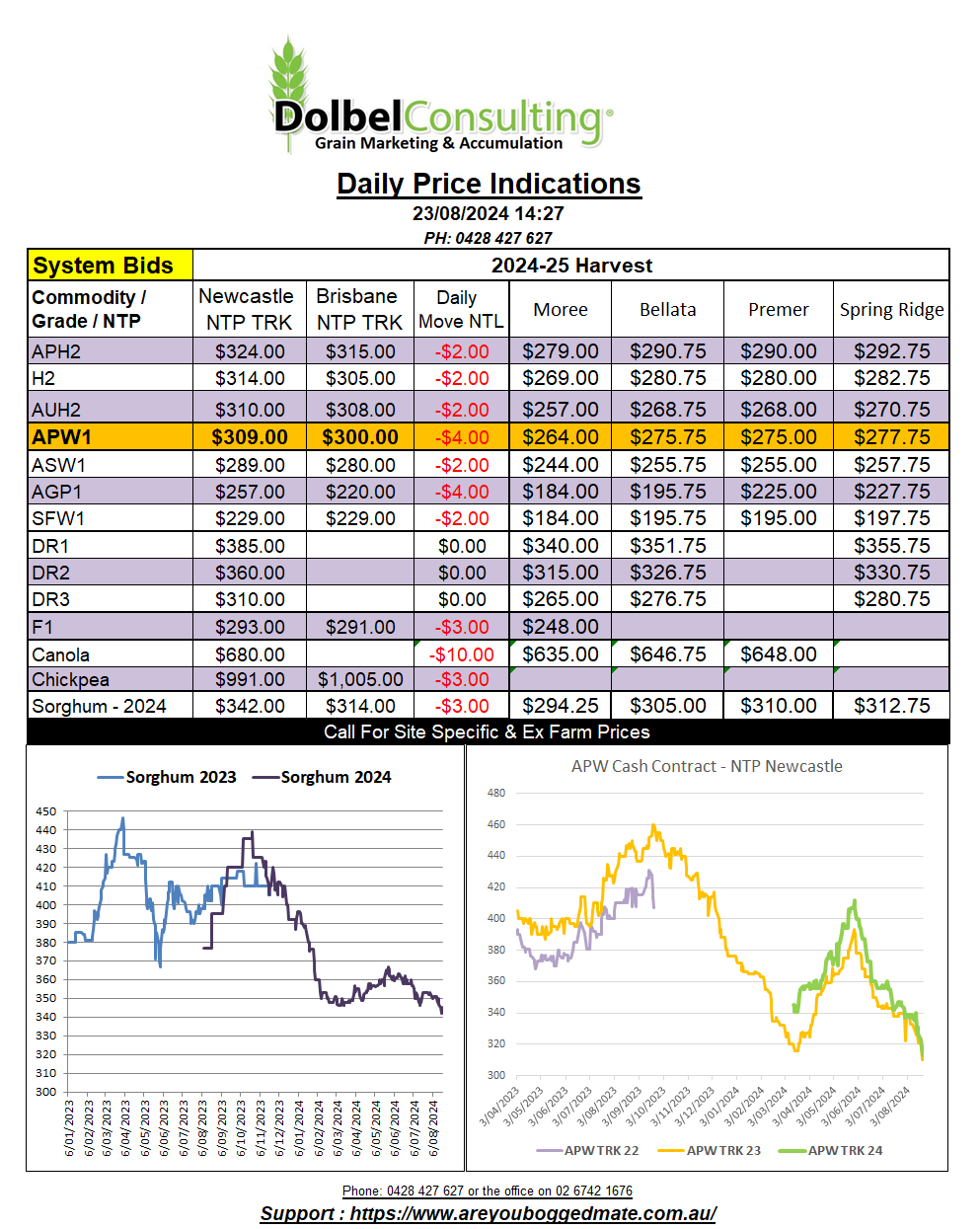

| There’s not many green markers on the board this morning. London feed wheat £3.30 lower in the Jan25 slot, Paris milling wheat €2.25 lower in the Dec24 slot. All three US traded grades of wheat futures are lower, Minneapolis spring wheat leading the way. As if that’s not depressing enough we also have Chicago soybeans back 20.25c/bu in the Jan25 slot. Both Paris rapeseed and Winnipeg canola are lower, Feb 25 Paris back €6.75 and Winnipeg canola in Jan25 slot shedding C$11.30. The AUD shed 0.53% against the US dollar, but that’s not enough to counter these moves. The slip wasn’t just restricted to futures markets, cash bids for wheat out of the US Pacific Northwest were AUD$2.00 – AUD$4.00 lower against yesterday’s conversions. French values were also lower day to day, the conversion now AUD$5.64 lower than yesterday. Interesting to see Black Sea values, day to day in AUD, were not as pressured as EU or US values though. The funds still hold a big short in Chicago wheat. This is a major anchor to any kind of price recovery at present. Mind you a recovery at present may have the potential to act like a double edged sword, potentially increasing inflation calculations thus impacting on interest rate indicators. It’s amazing to think that less than 100 fund managers could have such control over a market. The US futures market appeared to take the news of more damage to Russian export facilities and the rail strike in Canada (over before it started) as an opportunity to dump more wheat futures, testing contract lows. It appears for every buyer there’s two sellers trying to feed them a positive story. |

||||||||||||||