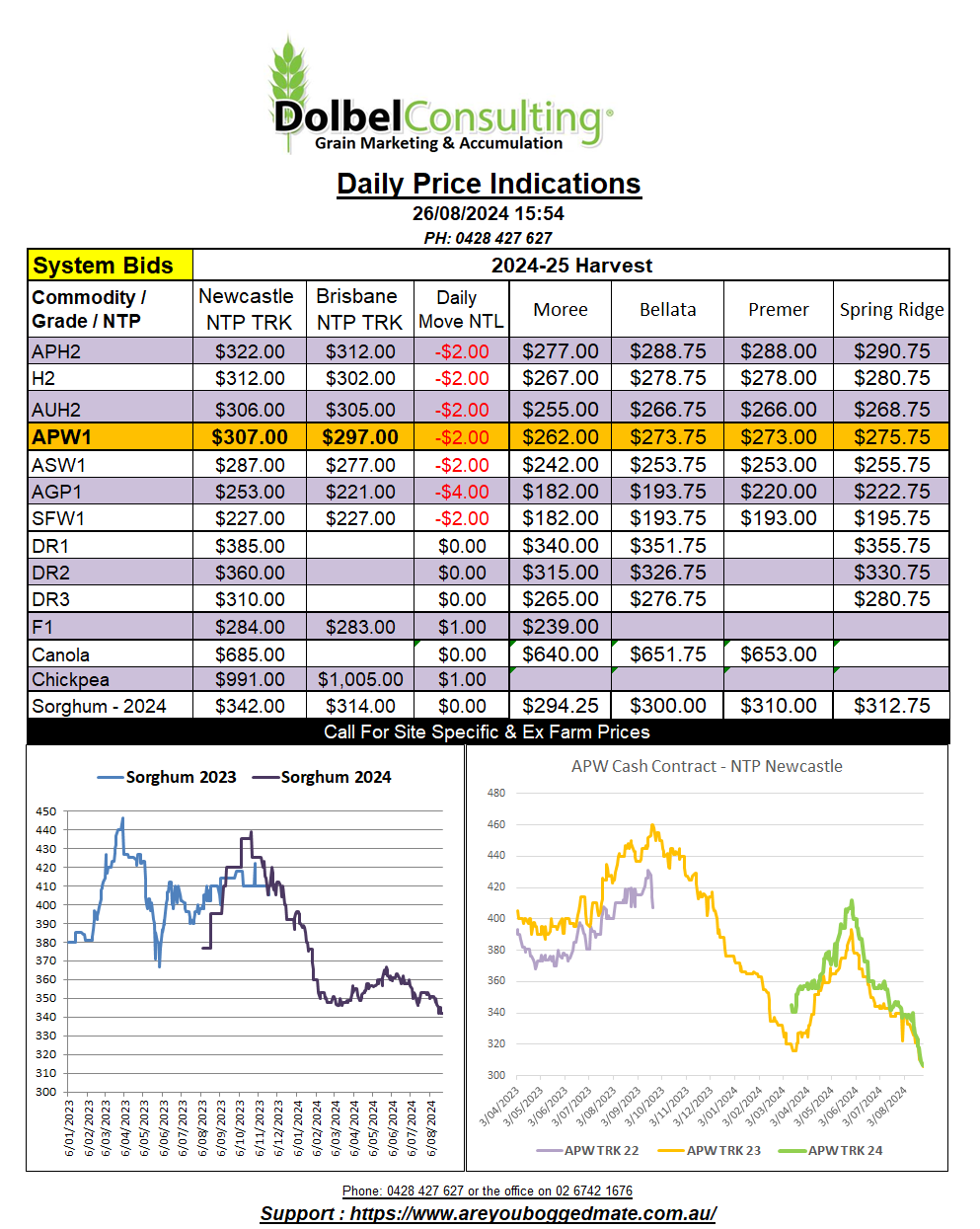

26/8/24 Prices

It was all about 2 things last night. The US dollar and soybeans, the rest, well they generally continued on the same path lower that’s been set by the funds for weeks now.

The FED confirmed their intention to start to lower US interest rates. It’s about 3 weeks until the official meeting where any rate cuts will be confirmed or rejected, so there’s bound to be plenty of speculation on the amount or if the first cut will be in September. In the meantime the weaker USD resulted in a sharp rally in the AUD, just what we didn’t need to see. Overnight the AUD closed up 1.36% at 67.97, just failing to breach 68c repeatedly.

The rally in the AUD was worth downside in wheat of roughly AUD$3.68/t when compared to yesterday. Combine that with a softer close in US SRWW futures of roughly AUD$4.73/t and it’s likely to weigh on new crop bids here on Monday.

In search of some good news we look towards the oil seed market. Volatility in this sector remains high. Chicago soybeans closed up 11.25c/bu in the Jan25 slot last night. The strength rolled across to both Paris rapeseed futures and Winnipeg canola futures. The three grains, the only grains to close in the green.

Nearby Minneapolis spring wheat futures were hit the hardest of the wheat’s, shedding 16.5c/bu nearby. Canadian spring wheat values ex farm SE Saskatchewan were also sharply lower. PDQ indicating average ex farm values there fell C$6.23 to C$231.74 for a December lift.

The stronger AUD was a problem across the board, exacerbating the fall in wheat prices in the US when converted to AUD per tonne, but also resulting in a day to day reduction in the conversion of wheat prices from international suppliers where values were flat in USD FOB basis.

US weekly soybean sales should be very good in next weeks report, every day this week US traders confirmed large sales. This has countered some of the negativity in the market due to the expectation of better than average soybean yields.