29/8/24 Prices

Argentina is still contending with less than ideal conditions for its wheat crop. Looking at rainfall data from WorldAgWeather.com shows that heavy falls over the last 2 weeks had generally missed much of the western wheat regions of Cordoba and Santa Fe. Falls were light across the state of Buenos Aires but were considered beneficial.

The seven day forecast from GFS which looked good earlier has since backed off the amount of rain expected to fall across Argentina, but it does show the potential for some good falls across the SE of Santa Fe, a major wheat growing area. Other forecast models tend to back up this prediction for next week, some even calling for heavier more widespread falls. If the rain does eventuate, it has the potential to turn the wheat crop around and help setup what many are now predicting to be a record sowing of soybeans for Argentina’s summer crop, corn acres should be much lower.

Keep an eye on this as it will not only have an impact on world wheat values during Q4 2024 and Q1 2025 but it could also have a big influence on world oilseed values if both Brazil and Argentina produce the volume of soybean that the punters are expecting.

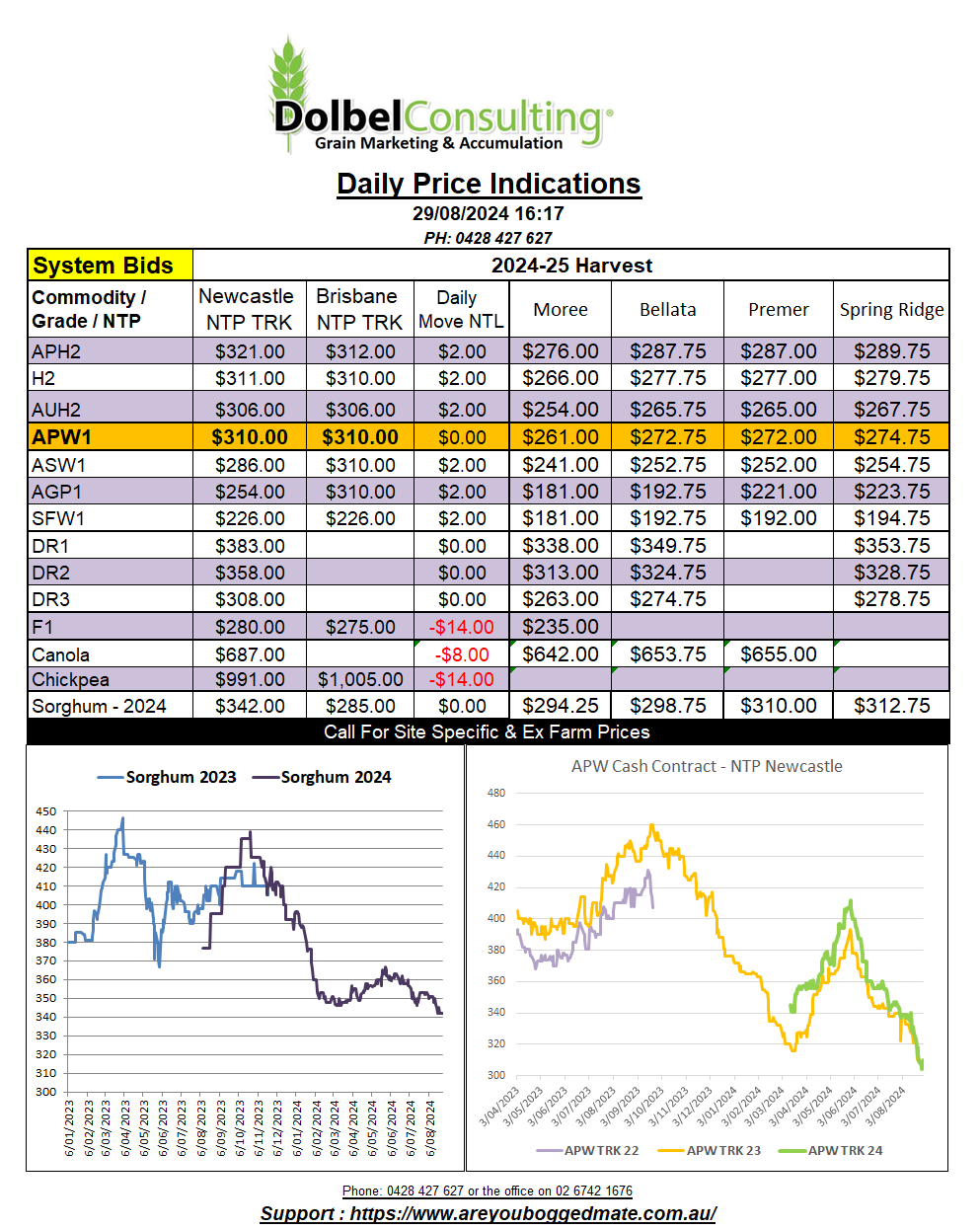

A higher close in all three US major wheat grades last night has the punters predicting that the wheat lows for 2024 may well be in. I mean it’s called the futures market for a reason, they are supposed to try and predict the future. Let’s hope this is right, current international values continue to be very cheap, below the cost of production for many producers in developed countries. Local basis appears to be happy to be bid between +30c/bu and +40c/bu. The gap between H2 and HRWW into the Asian markets has shrunk in recent weeks. HRWW no showing roughly a AUD$14 discount to H2. We would traditionally expect to see that spread closer to or at least +$20 to $35 for H2 (2023 chart attached).