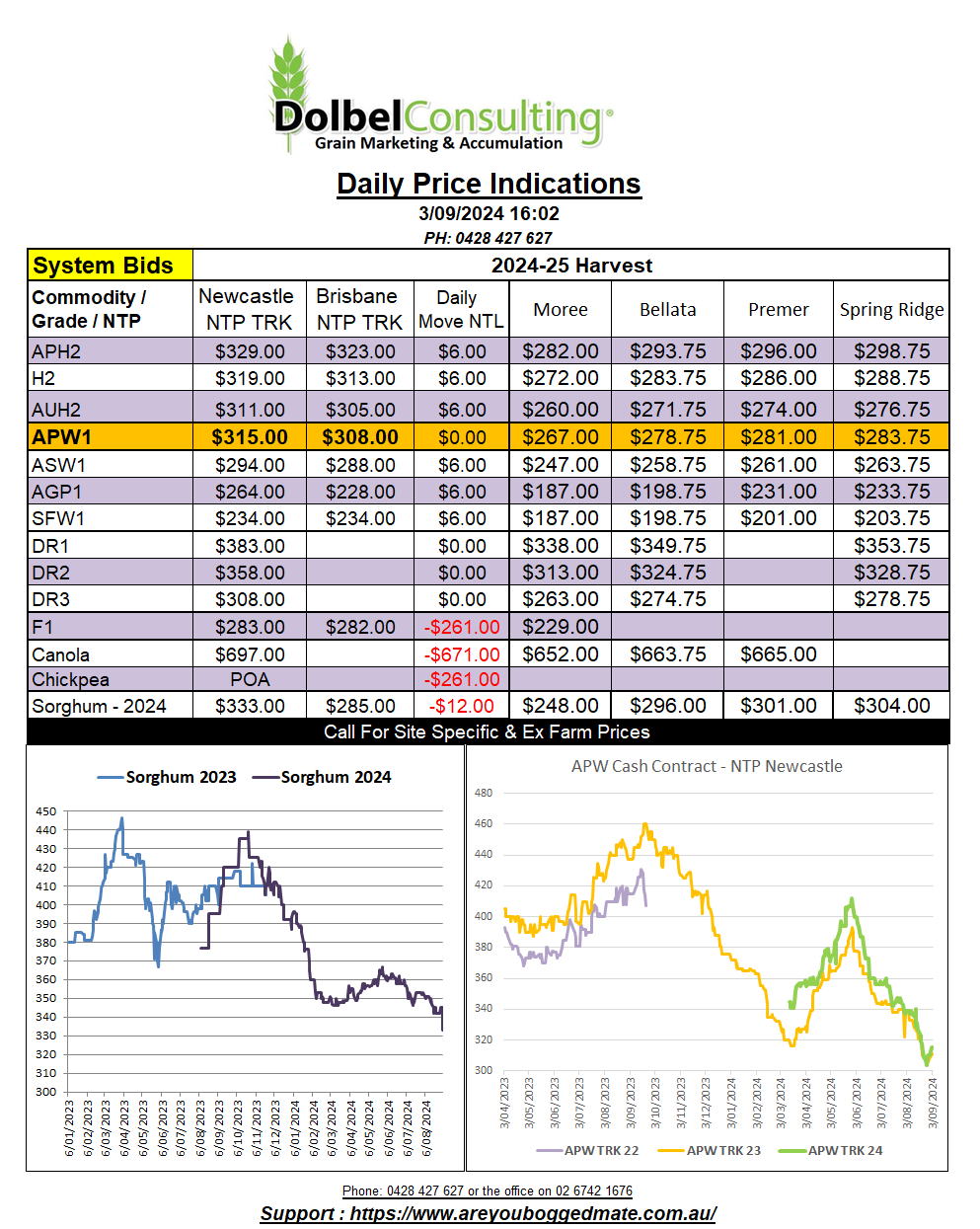

3/9/24 Prices

The Labour Day holiday in both the US and Canada has left the international markets a little thin on information this morning. The Paris and London markets were active but the movement in most grains was subdued. London feed wheat gained £0.50/t in the Jan 25 slot, Paris milling wheat gained €0.50 / tonne in the December slot and Paris rapeseed was also higher, putting on €1.00 / tonne in the Feb 25 slot. The move in rapeseed was largely negated by the stronger AUD, the day to day conversion improving just AUD$0.37 / tonne from last Friday’s conversion.

Black Sea wheat values were, in AUD per tonne, a couple of dollars lower when compared to Friday’s conversion.

Delhi market chickpeas were again on the up. Closing just 2Rs/Q below the season high at 8042Rs/Q. Execution costs from Australia have changed a little over the last month or so, container rates increasing as opposed to relatively flat bulk rates. This may continue to pressure inland bids as opposed to bulk bids to port. Growers looking to sell direct to port will need to consider quality and hygiene closely as opposed to more casual procedures when executing to upcountry packers with doctor bins and grading facilities.

ABARES increased their production estimate for the Aussie wheat crop by 9% over their June estimate. At 31.8mt the wheat crop is now pegged 2.7mt larger than their last estimate. Gains of 300kt in QLD, 1.2mt in NSW and 1.9mt in WA, were countered by small reductions in Victoria -377kt and SA -290kt. As a percentage, the WA crop is up almost 22.4% from the June estimate. With ABARES NSW crop estimated at 11mt, and as much as 11.725mt by some private analyst, there’s going to need to be a healthy export program to prevent carry over stocks becoming an issue. Unfortunately current world prices will probably struggle to flush out sellers in the volume needed to get the sales volume up where it may need to be.