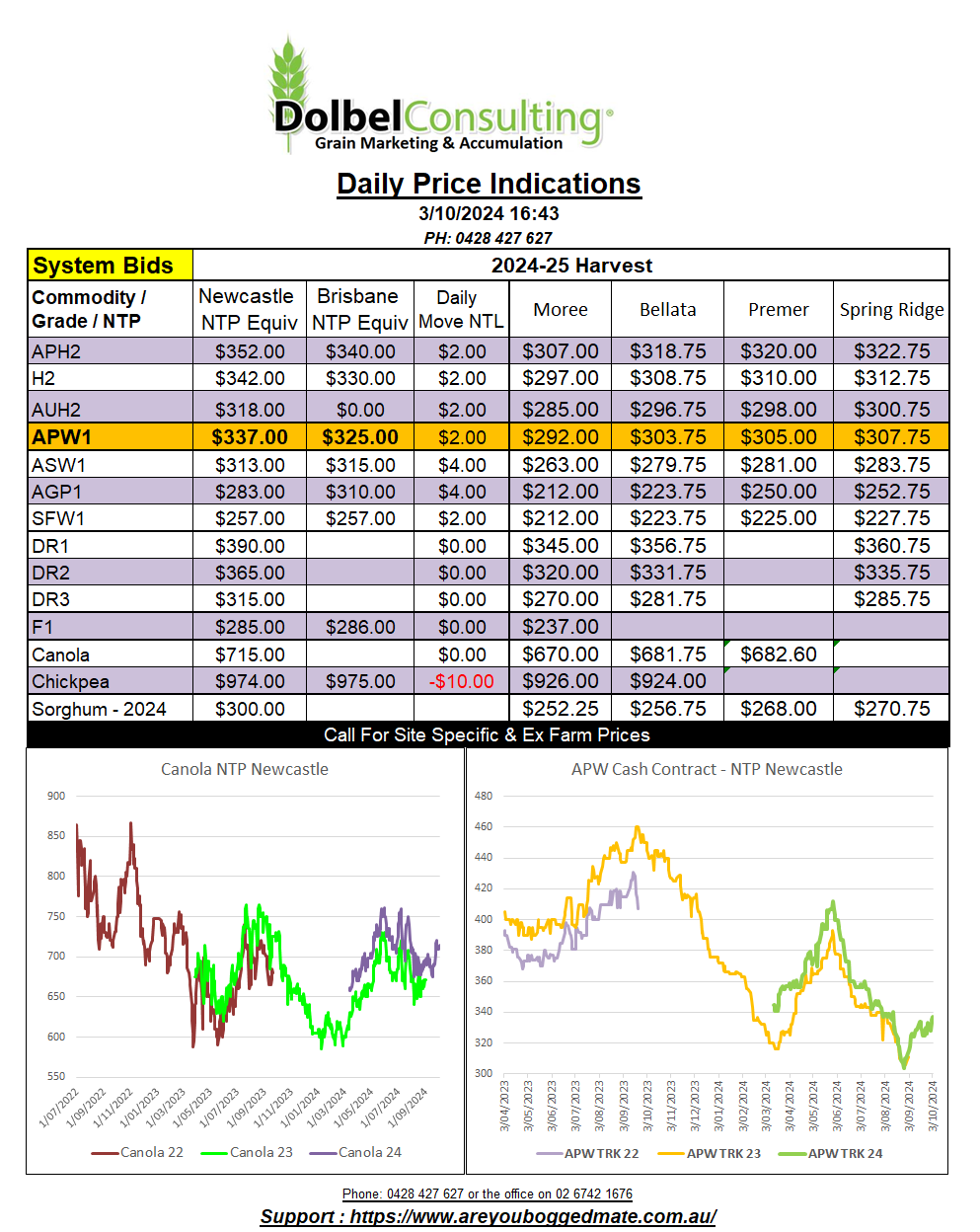

3/10/24 Prices

US and EU wheat futures continued to push higher overnight. HRWW futures closed more than 20c/bu higher, some cash bids even more so. Export values out of the US Pacific Northwest were also firmer. Taking the limited move in the AUD against the US dollar into account HRWW values out of the PNW were up roughly AUD$11.21 per tonne. White wheat values out of the PNW were more subdued, higher by roughly AUD$0.53/t over yesterday’s conversion.

Using China / Japan as a client the US HRWW value out of the PNW converts to roughly US$287 C&F importer. We can then do a rough conversion on this value, converting it back to an equivalent price XF LPP, or close to it. This number comes in at around AUD$320, this compares to yesterday’s local new crop H2 price of roughly AUD$308 delivered Gunnedah silo. This could be telling us that local values have some scope for upside while remaining competitive into the north Asian market. The H2 market into Brisbane remains comparable to export values, bid there at AUD$375 delivered yesterday.

Milling wheat futures at the Paris MATIF exchange were also stronger by the close. Up €6.25/t in the December slot and posting gains of €4.75 to €5.50 in the outer months. Managed money continues to reduce short exposure, actively buying Paris milling wheat.

The underlying drivers behind this week’s rally in both Paris and US wheat futures remain unchanged apart from some additional heat on the political side. Shrinking Black Sea stocks, frost damage in Australia, dry weather in Argentina, possibly changing there later this week, and persistent wet weather across the Brazilian harvest are all key fundamental influences. Dry weather is forecast for the Russian spring wheat region this week too, so we may start to see some quality data from that region next week. We are still a long way from seeing the necessary fall in world supply in order to trigger a big turnaround in price, but the changing fundamentals and political environment are keeping sentiment more positive than negative.