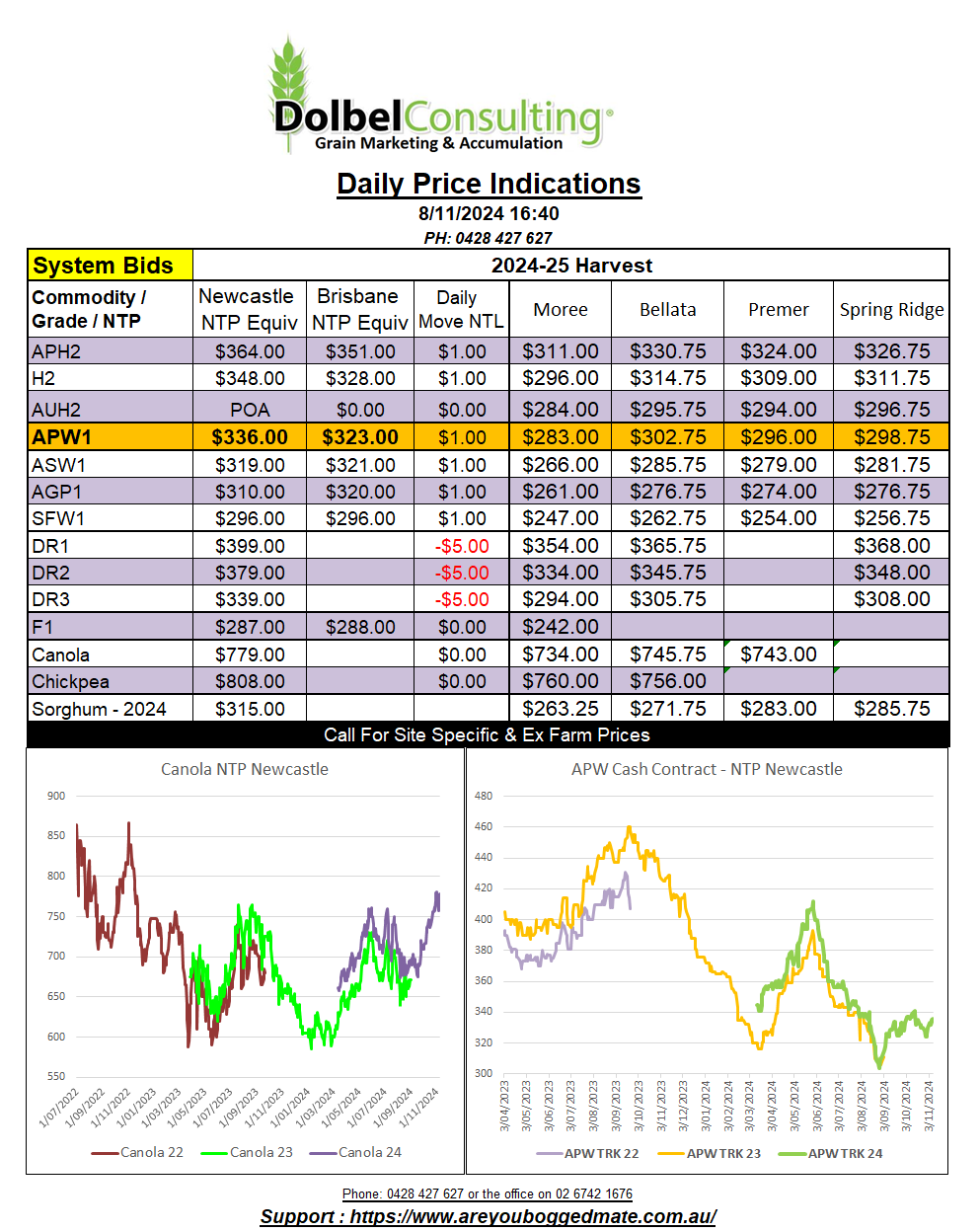

8/11/24 Prices

Rapeseed and canola futures bucked the trend lower in wheat last night. US soybeans had a good close, up 21c/bu (AUD$11.57/t) on the nearby contract at Chicago. This gave both Paris rapeseed futures and Winnipeg canola a nice injection, keeping up the momentum from the previous session.

Good weekly export sales by the US spurred the soybean pit into life. The number came in at 2.04mt, close to the top end of expectations prior to the release of the data. Good soymeal and soyoil sales also underpinned the complex. The punters are also talking about potentially lower US production in tonight’s WASDE report, possibly helping world stocks lower. Spillover strength from crude oil was also a feature.

It reads to be all about spillover strength from soybeans, with little new fundamental news for rapeseed or canola. Ukraine FOB offers were a smidge lower but cash bids across Canada followed the futures markets higher, continuing to ignore the prospect of Chinese tariffs as long as there’s good demand from Europe and their domestic crush market.

Wheat sales out of the US were back 9% from the previous week to 375kt. Although lower week on week the pace is enough to sustain a slight increase in year on year US export volume. US wheat out of the Pacific Northwest reflected the decline in futures. HRW now valued at 639c/bu. On the back of an envelope, using north Asia as a consumption point this converts to a H2 value of something close to $300 ex farm equivalent LPP. Yesterday APH2 port bids were indicated at $370 to $385 for APH2 & $360 – $370 for H2. This may not be the case today.

S.Korea picked up 63kt of feed wheat at US$266.92 along with 65kt of corn. Add this to the 100kt of milling wheat S.Korea booked from the US and Australia on Wednesday and they have had a busy week. The feed wheat number roughly converts to about AUD$300 XF LPP +/-. So very supportive of current values being bid for SFW1 / ASW1 on the LPP.