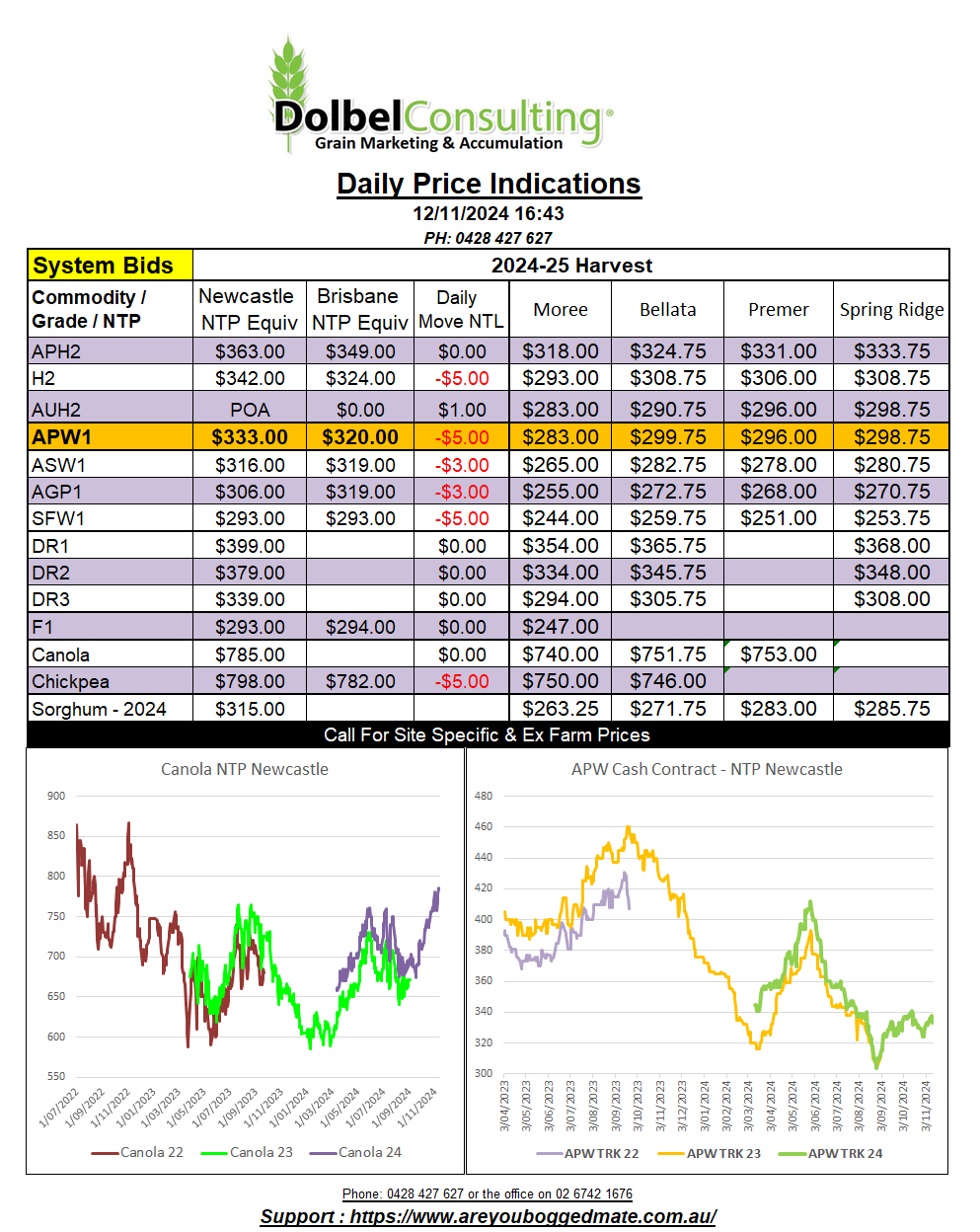

12/11/24 Prices

The Canadians had a day off for Remembrance Day. US markets, cash and futures, were generally lower. Cash wheat out of the Pacific Northwest declined up to AUD$8.60 per tonne for HRWW December. Club white wheat out of the PNW was lower by less than a dollar. The AUD was firmer against the Euro, countering the €2.50 move higher in Paris rapeseed futures. Paris milling wheat also shed value across all but the December contract which was up €0.50 / tonne, March down €0.50 and May down €1.00 / tonne.

Local basis to nearby Chicago SRWW was lower, falling from +38c/bu to +33c/bu, the weaker AUD playing a roll. International cash wheat values generally trended lower last night. Black Sea values were flat to softer while US and Argie offers were lower, as were French offers. This may weigh on local bids here today.

Fundamentals leading into the winter freeze period have improved across most major wheat producers. France continues to suffer from too wet / too dry but broadly speaking the EU block is likely to produce an average crop in 2025. The USA has seen good rain over the last 7 days. Most of the driest parts of the HRW belt receiving good falls and temperatures there remain favourable.

Showers across much of the Russian wheat regions have also been beneficial. This all points to a stagnated market, possibly rangebound, in the short to mid term without some unexpected demand arising.

We could also throw in the chance of some serious political influence for the next few years. If the US can broker a piece deal between Russia and Ukraine, that would most likely be bearish on values. As much as the trade has grown used to both Russian and Ukraine grain moving into the international market with just minor interruptions the conflict hasn’t starved the market of grains as first feared. The downside would be limited by world S&Ds but news of a deal would be bearish. The AUD is the real dark horse, the staunchness of the RBA against falling US rates is a problem.