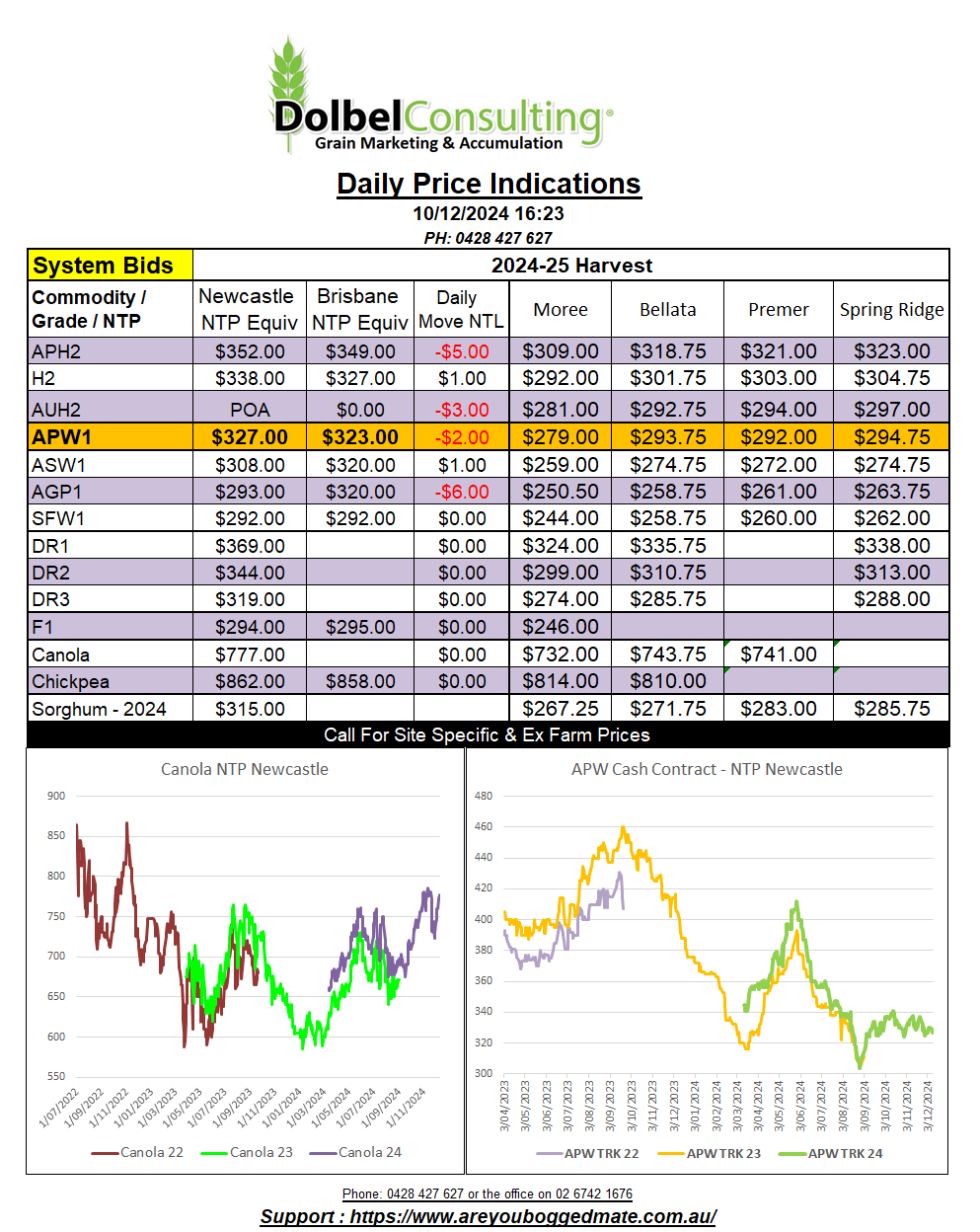

10/12/24 Prices

International Commentary

The AUD is back at 64.44 US cents this morning after testing a low of 63.85 early in the session before recovering and then slipping a little towards the close. The RBA have their Dec meeting finishing today, they will release the monetary policy decision statement at 2.30pm. The punters, who were initially forming a consensus that the RBA would reduce rates today, are now not so sure. A raft of measures could be used to talk rates flat and remain that way through to the February meeting. About 6.2m Aussie households would probably argue these measures, maybe not as effectively as someone managed argue with the US health insurance system last week, but tempers are high.

US wheat futures were a little higher, more gains in the higher grades. Looking at international values for 11.5% wheat, wheat similar in quality to our H2 grade, we see that Australian H2 wheat is now very well priced into the international market after a slight recovery in US values.

For example, US HRWW out of the Pacific Northwest is valued at roughly US$6.30/bu this morning. That’s comparable to a C&F north Asian consumer of about US$272. If we use that number and work it back to a Newcastle port price we can compare it to local H2 values and it tells us that H2 is probably now AUD$10+ cheaper than the US equivalent. Usually we would see H2 white wheat pull about a AUD$20 – $25 premium to red wheat, a A$10 discount must be making Aussie H2 wheat look very attractive to the Asian market.

International sorghum and barley values have done very little since mid last week, generally trending firmer but making minimal gains. US sorghum export sales were back sharply week on week, down 96% to just 4.3kt, China still the major buyer. US shipments were strong for sorghum, 153.7kt, keeping up with the previous better weekly sales volume. Black Sea barley was higher, mainly lead by higher export duties for Russian exports of both barley and wheat.

Domestic Commentary

Yesterday was a very frustrating day from a grain marketing perspective. The trade and consumer appear happy with their current positions and are not yet really focusing strongly on wheat exports out of the Newcastle zone. The stem report shows 105kt of wheat booked to move out of Carrington in December and just 50kt out of NAT. December is not the hardest month on the calendar to book 155kt of wheat, especially when NNSW has harvested close to 5mt of wheat. There is currently no further wheat bookings for Carrington showing on the Graincorp Stem report. The trade continue to play their cards close to their chest, as they did with sorghum this year. Not exactly what the stem report was designed to do.

The SFW1 market was flat yesterday, changing hands at $305 delivered Caroona / Killara Feed Lot for the March slot. The trade have the luxury of system ownership or ex farm ownership. Currently ASW wheat out of the Walgett area is bid at $257 site. A buyer could execute this by road and land it on the LPP for something close to $320 – $325, hence why we are seeing grower bids for ASW at about $310 to $320 delivered LPP, depending on the delivered date. The spread to SFW1 is still about $10.00. SFW1 changed hands at $290 ex farm last week for a January pickup. Slots are filling quickly.

There’s still minimal interest in feed barley, a little changed hands at $260 ex farm N-LPP late last week for a Feb / March lift, but there remains little interest in prompt pickup.

Chickpeas moved at $830 delivered Narrabri packer, bids generally weakened late in the day, many buyers actually refraining from bidding at all yesterday. Delhi chickpeas fell away overnight. Again narrowing the spread between local bids and the Delhi price, chart attached.