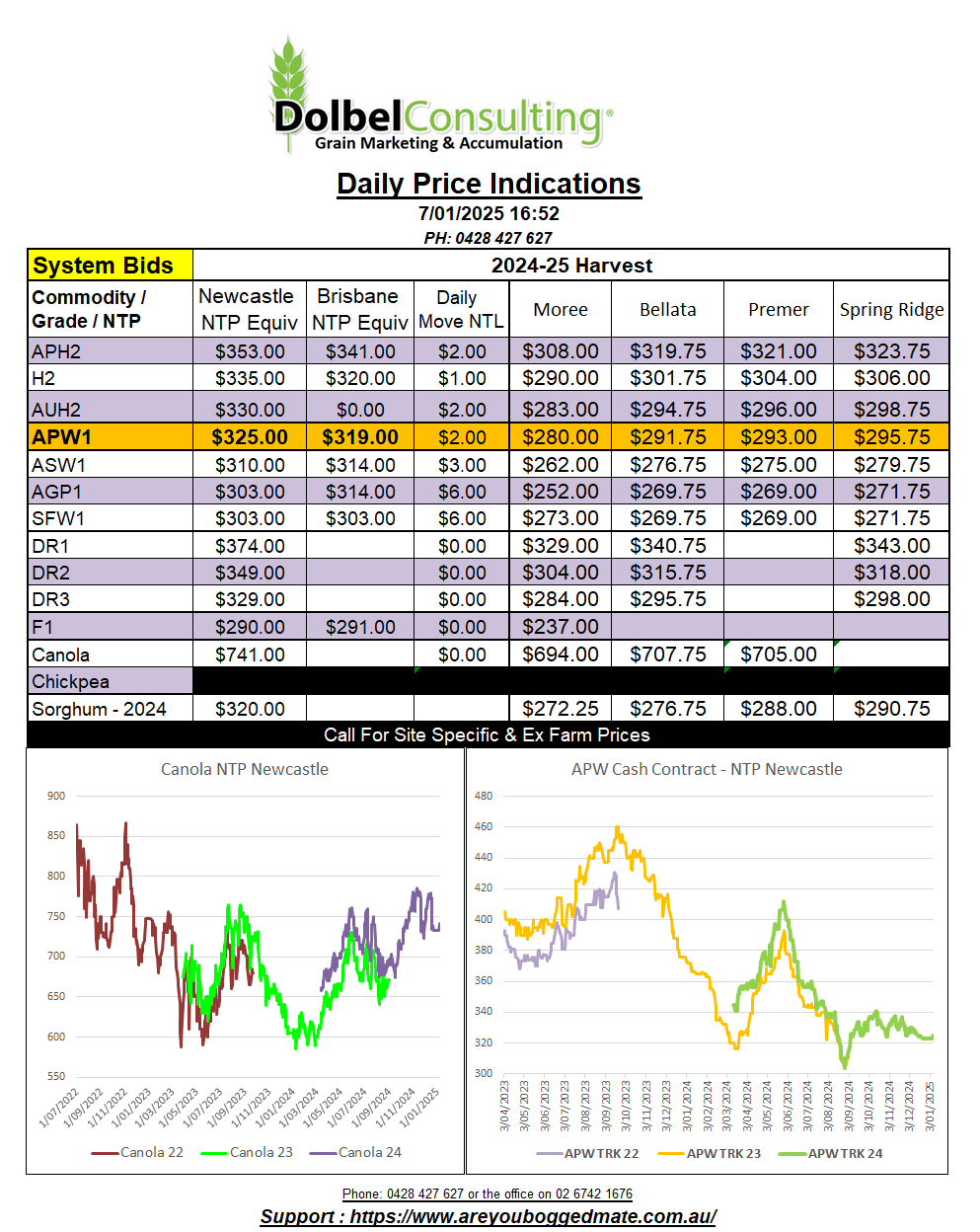

7/1/25 Prices

Over the break there were some good international purchases, mainly from Black Sea suppliers, but demand is demand and it all goes towards reducing world carry in stocks before the northern hemisphere gets into the new crop in July / August.

Egypt picked up 1.27mt of mostly Russian wheat late in December. According to Egypt’s state grain buyer this should meet the countries needs until June this year. The full details of the purchase have not been made public though, leading to some speculation on price, volume, and supply dates. In recent times Egypt has found it a little difficult to secure funding for wheat purchases. This saw Egyptian wheat stocks fall to just a 3 month buffer in the middle of last year. Since that time there has been further purchases but these contracts have also been plagued with execution issues and the full volume of purchases has not been delivered, leading to more speculation on Egyptian demand.

The weaker US dollar had a bit to do with last night’s increase in US grain futures. There were reports from the Washington Post that Trump was softening his stance on some tariffs, a report that was rejected by Trump later in the day. This saw the AUD rally to just above 63c mid session before falling sharply in the later half of the session and settling back around the 62.3 – 62.4 range.

In regards to retail sales, if our little shop at Gunnedah is any indication of December retail purchases across the country, I’m of the opinion that if the government comes out with data showing anything but the worst spending in more than 10 years I’ll call BS. There are just a few paper thin numbers holding this economy together at present, and retail isn’t one of them.

The AUD was mixed, stronger against most majors bar the Euro and Sterling. Dollar for dollar Aussie H2 wheat is still a great buy for the Asian market.