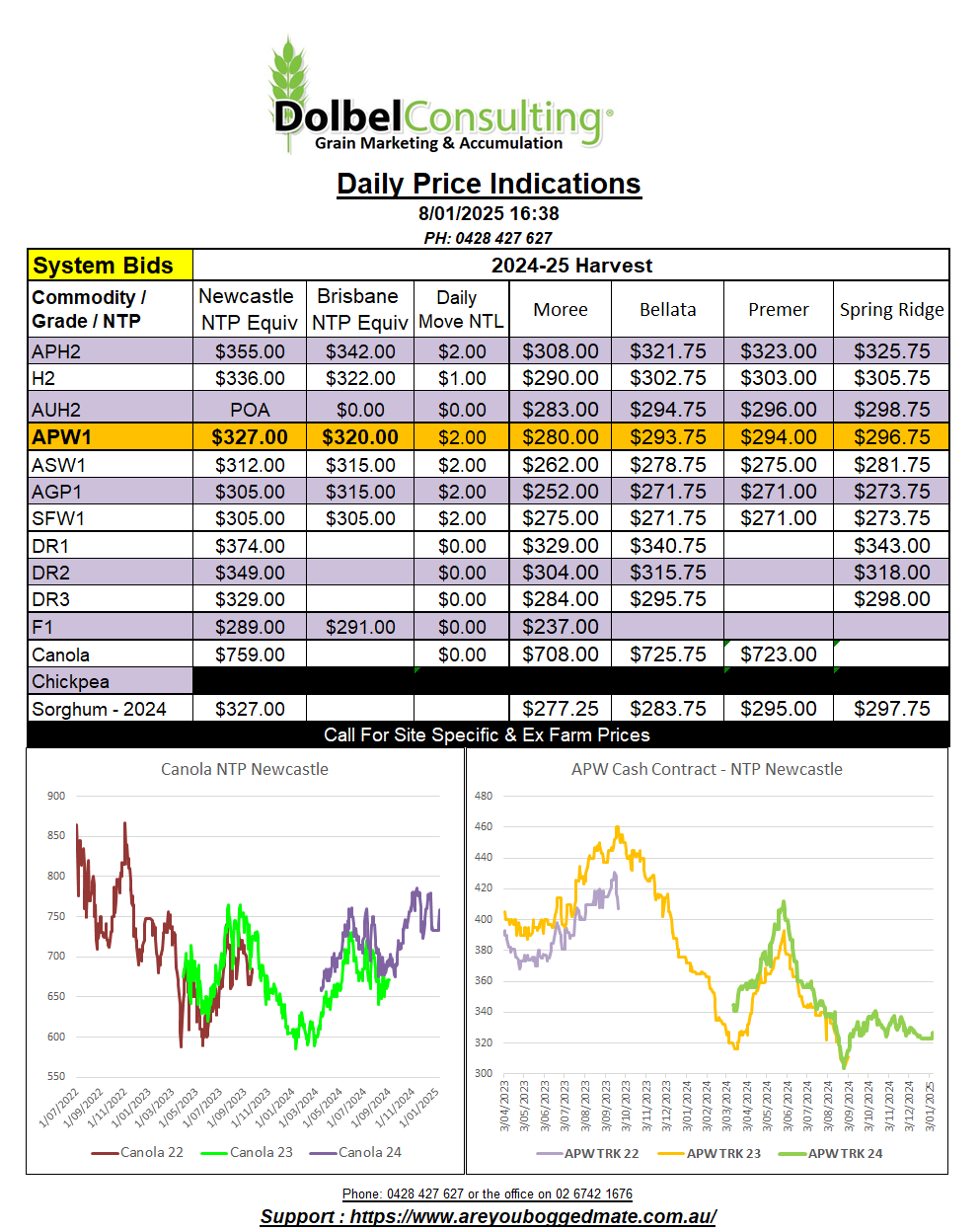

8/1/25 Prices

International grain futures were generally flat to higher in last nights session. Closing values for Paris milling wheat futures were mixed, the nearby shedding a little value while the Sept > May 26 contracts were a smidge firmer. London feed wheat futures were up just over a pound. US wheat futures were higher across all three of the major grades. Chicago corn made minimal gains while Chicago soybeans closed a smidge lower. The only product to really take a hit last night was Winnipeg canola, breaking away from the Paris rapeseed contract. Winnipeg closed C$4.10 / tonne lower across the Jan and March slots. Paris rapeseed made some good gains across all months, the nearby Feb slot closing €7.25 higher, May +€5.75 / tonne.

International cash values for wheat were mixed but generally a little firmer. US Pacific Northwest values followed the futures market with HRWW and spring wheat values generally about AUD$1.00 to AUD$2.00 higher FOB. White wheat values opposed the move in red wheat, actually shedding a dollar on the conversion comparison to yesterday. Stacking US club white wheat up against Aussie APW white wheat into the Asian consumer tends to indicate that the US may have a slight price advantage over Aussie wheat, not by much though.

When comparing Aussie H2 wheat with US HRWW out of the PNW into the Asian market the Aussie product continues to be very competitive, and a much better wheat when compared to the milling characteristics of HRWW to H2 white wheat. This indicates there is little potential downside in H2 values unless US values decide to push sharply lower. This is unlikely given the current export sales pace for US HRWW is good.

Support in US wheat futures was said to come from a worse than expected condition rating for the US winter wheat crop. It’s January, I wouldn’t be betting the house on a Jan report ringing true in April, there’s a long way to go. Although the 8pt drop in the Kansas G/E rating was large, it’s still rated 47% G/E.